People tend to be overconfident in their views. They are overconfident about their political views, their religious views, their views on global warming, even their views on sports. That’s just human nature.

And people are especially overconfident about their understanding of markets. Here’s a Slate.com article from two days ago:

China’s Stock Market Is Falling Again. This Was Entirely Predictable.

For a little while, China’s stock market seemed to be rallying from the nausea-inducing crash that wiped out a third of its value in a month. Now, it’s back to falling, albeit a little more slowly. Over the past two days, the Shanghai Composite Index is down 4 percent. Tally the ups and downs, and it’s off about 26 percent from its June heights.

There are a few reasons why shares are dipping again. But one of the biggest, as the Wall Street Journal notes, is simply that investors are finally free to buy and sell stocks like normal again. Most of them, anyway. At one point last week, trading had been suspended for more than half of all listed corporations on China’s markets.

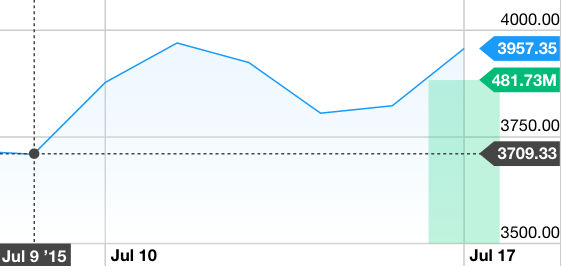

Was the market decline entirely predictable”? I doubt it. And if it was, why didn’t Slate.com tell us it was going to happen two days earlier?

And I don’t understand the phrase “is falling again”. Why not say “has recently fallen”? Doesn’t “is falling again” subtly suggest some sort of downward momentum, likely to continue for at least a short while? But then why did Chinese stocks rise about 4% in the two days after the Slate article, to the level before the “entirely predictable” decline? And where is the entirely predictable Chinese market going next?

Although Slate.com did not predict the decline two days earlier, they did say this back on the 9th of July:

China’s stock market stopped crashing on Thursday. After a stunning four-week drop that obliterated a third of its value, the Shanghai Composite Index rose 5.8 percent, its largest one-day gain in six years. This may be a sign that that the Chinese government’s extraordinary efforts to calm investors have finally worked.

Or, it might just be a breather before the carnage starts anew.

Here’s the problem. Sooner or later, trading will have to go back to normal. And when it does, there’s a good reason to think the sell-off will start up again, since Beijing hasn’t done anything to address the likeliest culprit behind the plunge: Too many mom-and-pop investors borrowed money to buy stock, which they are now being forced to unload in order to cover their losses.

It could be the “efforts . . . worked” or it could “just be a breather”. Okay. And how did the market move after July 9th?

It went up for two straight days. Then down for two straight days. Then the Slate.com “entirely predictable” comment. Then up for two straight days. What about that was entirely predictable?

In my view markets stock prices changes are roughly a random walk, and market movements are nowhere near “entirely predictable”, even with government distortions. Those investors still free to buy and sell would be inclined to do so at prices expected after the government meddling ceased (which is one reason I doubt that government intervention has much effect, except to the extent it increased perceived liquidity risk, or if the government is seen as planning to hold the stocks permanently.) If the government is simply trying to delay an inevitable decline for a few months, it’s unlikely to succeed, even in the short run.

I would add that the government did not intervene in the highly liquid Hong Kong market, which tends to be strongly correlated with the Chinese market. And yet that market also had a sharp price run-up, a steep decline, and then a partial recovery–just like China.

People love to say things like “The US housing bust was entirely predictable”, even when they have no explanation for why house prices in Australia, New Zealand, Canada and Britain are still at so-called “bubble” levels. Why didn’t entirely predictable crashes occur in those 4 countries?

I recommend that people ignore all predictions of the future movement of asset prices, whether it is from the media, professional economists, or Wall Street stock pickers. There is no evidence that these forecasts are useful.

READER COMMENTS

David R. Henderson

Jul 17 2015 at 11:20am

Excellent post! Much needed.

One quibble: Markets are not a random walk. Stock price changes are a random walk.

Scott Sumner

Jul 17 2015 at 12:34pm

Thanks David, I clarified that.

The Original CC

Jul 17 2015 at 12:37pm

DH, I think that’s backwards. Price changes are actually mean-reverting. Price levels follow (roughly) a random walk. (This leads to endless confusion when people start saying that some price should “mean-revert”…)

Floccina

Jul 17 2015 at 12:41pm

I believe that per capita GDP in China (currently about $7k) will approach that of Japan (currently about $38k) over the next 20 years getting within 25% or 20% by 2035 and so I have been buying some of what I consider the stronger china based companies. A fall in stock prices is great. Many things could stop my prediction from happening but all investments have risks.

meets

Jul 17 2015 at 1:47pm

Would love to invest in a Slate hedge fund.

Scott Sumner

Jul 17 2015 at 1:50pm

Thanks CC, I’ll get it right eventually. Maybe my editorial changes are a random walk. 🙂

David R. Henderson

Jul 17 2015 at 2:18pm

@The Original CC,

Price levels follow (roughly) a random walk.

I’m pretty sure you’re wrong. When I made that statement at the University of Rochester in the late 1970s, which, with people like Mike Jensen there, was a finance powerhouse back then, a financial economist named David Mayers corrected me. He pointed out if prices were a random walk, all you would need do to make a lot of money is wait until they are very low, then buy, and then sell when they are high. That’s why the correct formulation is that price changes are a random walk.

emerson

Jul 17 2015 at 3:29pm

I do not claim to truly understand the stock market. If I could predict the stock market I would be a zillionaire – which I am not.

But the correction in the Chinese stock market may be fundamental.

As I understand, all corporations in China are at least partly owned by the government. This is the “State run capitalism” concept that emerged out of the ashes of the 2008 financial crisis and was – – at least for awhile–considered to be the new paradigm of success.

In Nov. 2014, The Economist published a report: “State Capitalism in the dock”, that showed how the profitability and valuations of state owned enterprises was rapidly falling.

Apparently, when a company is required to primarily serve the political mandates of the government, profitability suffers.

Who could have predicted that?

Jesse

Jul 17 2015 at 3:43pm

Perhaps people are using slightly different definitions for “price changes”? A random walk can’t be gamed by “buy low, sell high” unless it’s mean reverting.

DH, your points about Slate are great.

Maybe Slate could start a virtual hedge fund, where they are given the benefit of hindsight, they can make all sorts of claims of what was obvious in the past, but they don’t trade real money. Yet they could charge fees for shares in the hedge fund, and it could yield haughtiness credits. Wait – I guess they do that for free for their readers now.

Jesse

Jul 17 2015 at 3:45pm

My apologies – I meant “Scott, your points about Slate are great.”

Gordon

Jul 17 2015 at 5:55pm

“That’s why the correct formulation is that price changes are a random walk.”

If true, doesn’t this mean that the attempts by investment firms to engage in high speed trading only serve to increase the “stride length” on that random walk?

khodge

Jul 17 2015 at 6:02pm

Admittedly it gets confusing when mixing markets and economies, but back on July 5 in “Greece: What are the Markets telling us” you seemed more willing to accept what the markets were telling us about Greece than what they currently are telling us about China.

I think there is validity to what Slate is saying as long as they did not put a time frame on it. Also, even with perfect foresight, I would be extremely hesitant to bet on the Chinese market because you are also betting on whether the markets have reached the transparency and technological expertise that we have with the US markets.

hanmeng

Jul 17 2015 at 7:56pm

I believed this was a good blog. I see now I may very well have been wrong. (I suppose I should acquire the conscience of a “liberal”, now.)

Scott Sumner

Jul 17 2015 at 8:59pm

David, Whatever the correct terminology, the concept is clear.

Emerson, I’ve never liked the term ‘correction’. In a sense all asset price movements are corrections.

Thanks Jesse.

Khodge, You said:

“Admittedly it gets confusing when mixing markets and economies, but back on July 5 in “Greece: What are the Markets telling us” you seemed more willing to accept what the markets were telling us about Greece than what they currently are telling us about China.”

No, there is no contradiction at all. I think you misunderstood this post, which was about prediction. I never claimed to be able to predict future movements in either Greek or Chinese stocks, and I don’t believe anyone else can either. In the Greek case I simply pointed out that the Greek market clearly responded to major policy announcements. That’s also true of the Chinese market. When the PBoC does unexpected monetary stimulus, Chinese stocks tend to rise. One post was about prediction, the other was about correlation.

hanmeng, Yes, it’s quite possible that this is not a good blog.

The Original CC

Jul 17 2015 at 11:45pm

DH- I’m not sure what you’re talking about. If prices were *mean reverting* then you could just buy when they fall below average. But if prices follow a random walk then that strategy won’t work.

Price changes clearly don’t follow a random walk (except maybe a trivial one that only a mathematician would call a random walk). If they did then after stocks had a big up day, you’d be able to predict that the next day’s move would also be large and positive.

If a process follows a random walk then each value is the previous value plus some randomly determined change. That’s exactly how efficient market guys model stock prices. On the other hand they certainly don’t model price changes that way. Instead a simple model might have price changes picked from a normal distribution each time. So they’d be iid, not a random walk.

Comments are closed.