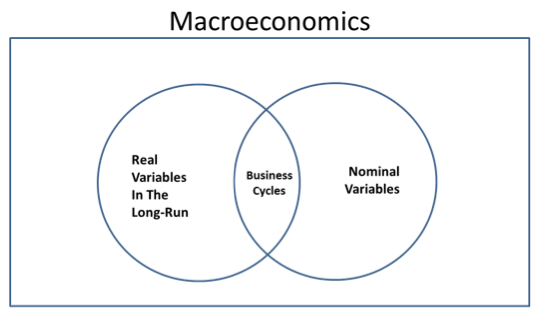

Several other bloggers have recently described how they visualize macro, so I’ll play copycat. I see three types of macro, each radically different from the other two:

Long run nominal is the easiest to explain, then business cycles, and long run real growth is the most complex.

1. Long run nominal trends. Central banks determine the long run trend NGDP growth rate, or long run inflation rate, by adjusting long run growth in the monetary base, relative to money demand/velocity, which is mostly determined by non-monetary factors in the long run. The only exception is that when the long run trend rate of nominal growth is slow enough to push interest rates to zero, then money demand shocks become relatively more important. Changes in the long run trend rate of inflation/NGDP growth have fairly small second order effects on real variables unless the changes are extreme. Money is roughly, but not precisely, neutral and super-neutral in the long run.

2. Business cycles. There are two types of business cycles—with or without big swings in the unemployment rate. Throughout most of history, real output volatility was primarily due to real shocks such as wars, droughts and plagues. These did not necessarily impact the unemployment rate.

In large modern economies, real shocks such as the 2011 Japanese earthquake have at most a very modest short-term impact on output, and almost no impact on unemployment. Some public polices can impact the unemployment rate, such as FDR’s NIRA rule that mandated a 20% across the board wage rate increase in July 1933. European style labor market policies can lead to a higher natural rate of unemployment. But even in Europe, fluctuations in the unemployment rate are primarily due to nominal shocks.

Like Keynes, I believe that modern business cycles reflect the interaction of sticky wages and nominal GDP shocks leading to employment fluctuations. Unlike Keynes, I believe wage flexibility would help, although I don’t think there’s much the government can do to make wages more flexible. And unlike Keynes, I believe monetary policy drives NGDP shocks. Recessions are caused by the failure of central banks to stabilize one or two year forward NGDP expectations. Wage flexibility at the individual level doesn’t solve the problem for that individual; it’s aggregate wage stickiness that matters.

When the central bank has a bad target, such as an inflation target, then fiscal policy can help. But fiscal policy should always involve tax changes, never spending changes. (See this, for example.) Spending should be determined according to classical cost/benefit considerations. And the low interest rates typically seen during a recession do not imply a need for more government spending—that’s reasoning from a price change.

3. Long run economic growth. This reflects many factors. It’s useful to contrast per capita growth near the frontier (US/Switzerland/Singapore) and catch up growth (China/India/Ethiopia.) Trend real GDP growth at the frontier reflects technological progress at the global level, and good governance at the country level.

Catch-up growth occurs when there is some sort of public policy change that makes a country’s position in the pecking order change. Thus under Mao’s policies, China’s natural position might have been 5% of the frontier, and the switch to a 1950s European-style mixed economy might move China’s natural position to 55% of the frontier. They are currently transitioning to that 55% position. Further gains beyond the 55% point would require further market reforms.

Both human resources and good governance determine the natural position of a country. In some cases, such as the two Koreas, governance explains most of the divergence, although human resources may change as a result. Most low-income countries suffer from both low human resources and bad governance, and indeed the low human resources may partly cause the bad governance.

Human resources relate to cultural factors such as utilitarianism (i.e. sympathy for strangers), trust, patience, and also average IQ. In the modern world, human resources matter much more than natural resources, except in small oil-rich countries. Human resources can be increased more easily than natural resources, although we are not certain which methods are most effective.

Good governance consists of deregulation, privatization and fairly low marginal tax rates. But government can play a constructive role in areas such as the environment and (consumption) redistribution. If all countries had the same governance, there would still be lots of inequality in the world, but far less than we currently see.

READER COMMENTS

Patrick R. Sullivan

Nov 16 2015 at 10:06am

It might be able to, at least for large employers. It could mandate that at least part of wages paid not be ‘fixed’ (so much per hour/month), but fluctuate according to, say, a firm’s revenue.

Matt Moore

Nov 16 2015 at 10:33am

… I don’t think there’s much the government can do to make wages more flexible

Do you think that government can make wages less flexible? I’m assuming yes. In which case, surely they can increase flexibility by just not doing those things?

Also, and I think I’m getting confused here, don’t you think that at least part of real wage inflexibility is based on nominal inflexibility? In which case wouldn’t a higher NGDP growth target increase flexibility?

Steve Fritzinger

Nov 16 2015 at 11:08am

Why do we talk about the business cycle when it isn’t a cycle? At least not in the sense of night following day or winter, spring, summer, fall.

It’s more like my health. I experience alternating periods of wellness and sickness, but no one would call that a health cycle.

Does talking about the economy as if it’s a real cycle affect how we try to manage it? Treating every down turn with a generic “stimulus” ike a doctor who believes in the health cycle treating every disease with a generic “medicine”.

Jim Dow

Nov 16 2015 at 1:56pm

@Steve Fritzinger

At one point people did think about it as a cyclical phenomenon, if with irregular periodicity. Wesley Mitchell and the NBER, who did a lot of the early work on business cycles, treated each cycle (trough to peak to trough) as a unit of measurement so that you could measure various economic behaviors as the average across cycles.

A more neutral term would be “aggregate fluctuations” but then you have to explain what you mean every time.

Scott Sumner

Nov 16 2015 at 6:12pm

Patrick, Possibly, but I would not favor that sort of policy.

Matt, The primary way they could boost wage flexibility is by abolising minimum wage laws. But that would not do “much”, as I said.

Steve, I don’t favor having policymakers treat the business cycle like a disease, but rather believe they should try to refrain from causing cycles in the first place. Don’t cause more diseases than necessary, have a stable monetary policy.

Matt Moore

Nov 16 2015 at 6:41pm

What are the key institutional factors underlying wage stickiness?

Michael Byrnes

Nov 16 2015 at 7:24pm

@ Matt Moore

Personally, I think wage stickiness is more of a transaction costs/game theory problem.

Scott gave one example. As a worker, I might prefer a 10% wage cut over a 10% change of getting laid off. Then again, if I see myself as one of the better employees (or just willing to bet my job on 90% odds), I might not. But as Scott says, whether I would take that deal or not is irrelevant – because few companies, if any, would ever offer it. The closest most companies would ever get to that is a wage freeze, which sounds like sticky wages to me.

Then you have lots of other issues. Companies have every incentive not to be up front about stuff that concerns the health of the company. “Our revenue is in free fall, so we’re going to have an across the board 10% wage cut” will, in all likelihood, send the best employees running for the exit as far as they can get there.

Also, employees may not want to accept a salary cut because a pay cut may not just reduce a worker’s current salary but also his future earnings potential. (As an offered salary is often based on a worker’s current salary, and sometimes this is verified through background checks).

James

Nov 16 2015 at 9:25pm

If wage rigidity is a factor contributing to unemployment, then we should observe more rigidity among the unemployed than among the employed. In fact we see the opposite. The *only* evidence for wage rigidity comes from observations of the employed, a population in which there is no unemployment to explain. Among the unemployed, a population in which there is a lot of unemployment to explain, there is very little evidence for wage rigidity.

A question worth asking is what would happen if unemployment were caused by real factors, such as forecasting errors, and the central bank misdiagnosed the situation as being the result of nominal shocks and tried to fix things by smoothing out NGDP. If a business was making things that could not be sold at a real profit, an easy monetary policy might well obscure this by leading to a nominal profit, potentially even leading to an expansion of the industry. NGDP would keep rising but welfare would fall because of the mismatch between the type of output and the preferences of consumers.

ThomasH

Nov 16 2015 at 11:00pm

Scott,

These two statement seem incompatible:

1.

2.

In the classical cost benefit analysis I know about, one discounts the future benefits by the an interest rate. If the rate at which the government can borrow falls, more activities will pass a classical cost benefit test. Moreover marginal costs of most items of government expenditure will be less than market prices — that’s what unemployment of factors of production means. The Hoover Dam, TVA, and all those trails in National parks built by the WPA were darn good investments. (And we know a lot more today about how to do cost benefit analysis than they did in the ’30s.)

Now if there are predictable ways to use tax changes to get private individuals to change their expenditure plans (which are mistaken because, as for governments, the marginal cost of those expenditures is less than market prices) then tax policy has a role as well. Reducing the wage tax and transferring funds to state and local governments so they don’t lay off public servants and having the government borrow the difference would be a good example.

And since it is such a popular fallacy, I’d think you’d have a few words against the idea of “austerity” — reducing expenditures when deficits rise.

Michael Byrnes

Nov 17 2015 at 9:11am

James wrote:

“If wage rigidity is a factor contributing to unemployment, then we should observe more rigidity among the unemployed than among the employed. In fact we see the opposite. The *only* evidence for wage rigidity comes from observations of the employed, a population in which there is no unemployment to explain.”

Can you explain your reasoning more clearly?

Wage rigidity contributes to unemployment if a company chooses to reduce payroll by cutting staff rather than by cutting wages. For salaried positions, layoffs are the norm and salary reductions are the exception.

Scott’s argument is that an individual employee who would prefer to accept a reduction in pay rather than take his chances with a possible layoff cannot solve this problem. (I think employees would need to make this decision collectively and get buy in from their firm in order to make this happen.)

Scott Sumner

Nov 17 2015 at 12:00pm

Matt, I don’t know.

James, You said:

“If wage rigidity is a factor contributing to unemployment, then we should observe more rigidity among the unemployed than among the employed.”

I’d expect just the opposite. I’d expect less wage flexibility among professions unlikely to be laid off during a recession (say nurses) and more flexibility among professions more likely to be laid off during a recession (say blue collar workers.)

Your argument might be correct if individual wage stickiness were the problem, but in fact the problem is aggregate wage stickiness, and making an individual’s wage more flexible doesn’t solve that problem.

You said:

“The *only* evidence for wage rigidity comes from observations of the employed, a population in which there is no unemployment to explain. Among the unemployed, a population in which there is a lot of unemployment to explain, there is very little evidence for wage rigidity.”

No, the problem for the unemployed is not their own wage rigidity, it’s the wage rigidity of the employed. If wages for the employed are rigid, firms have no money available to hire the unemployed (when NGDP falls), regardless of wage flexibility.

Thomas, You are reasoning from a price change. Draw a saving and investment diagram. Shift the investment schedule to the left. Note that as interest rates fall, the optimal amount of investment falls, even using the cost/benefit criterion.

James

Nov 20 2015 at 11:50pm

Michael,

I believe heavy drinking causes liver damage. If you asked for evidence, I would cite the presence of liver damage among heavy drinkers. I wouldn’t point out that there seems to be a lot of drinkng by people with healthy livers.

Some people believe wage rigidity causes unemployment. They should be pointing to high levels of unemployment among those with wage rigidity. Instead they point to wage rigidity among the employed.

Scott,

If you want to claim that wage rigidity is a precipitating cause of unemployment, you need to point to wage rigidity among the unemployed exceeding the wage rigidity of the employed. I really don’t see the point in using cross sector comparisons between nurses and construction workers because it breaks ceteris paribus and fails to isolate variables.

If an employer has a finite budget and they don’t employ every potential worker, you don’t need behavioral stuff like wage rigidity to explain that. Budget constraints from regular economics are enough. I wonder what evidence it would take to get you to change your mind and say a particular bout of unemployment wasn’t wage rigidity, just budget constraints and reservation wages.

If some employer’s budget cannot cover the reservation wages of all of the applicants that want to work there, that’s not a wage rigidity problem, or any other kind of problem. There is nothing to fix. But say some central planner is convinced of the wage rigidity story tried to fix it by monetary easing. What is supposed to happen next? The employer’s budget constraint expands in nominal terms so they hire more workers, but the workers are now making less than their reservation wage in real terms. That’s a pretty bad result to solve the wrong problem. So you need to be really sure about this nominal rigidity story. Unfortunately, you give no actual evidence.

J.V. Dubois

Nov 23 2015 at 7:04am

James: Scott repeatedly said that it is aggregate wage rigidity that matters. You are committing the composition fallacy.

For instance if you have asthma because of heavy smog in the city where you live, your own ability to decrease the amount of smog you yourself produce does not matter. It is the the aggregate smog level that triggers your asthma attack.

The best way to think about this is as if wages are subject to some sort of private price control system. Think about tickets for a concert of a popular band. Sales start year ahead for a fixed price, servers crash and the next minute when you load the page you see all tickets sold out. It does not matter that you were willing to pay 10% more than the list price (but not 100% more as on black market). Why does this happen on private and unregulated market? There probably are studies about this but the short answer is: who knos? Ticket sellers lose money and potential customers who really want to go to the concert end up frustrated.

Comments are closed.