Bloomberg has an article discussing recent research on price stickiness:

U.S. inflation has been lower than standard economic models would predict throughout the current expansion. Some blame the rise of Amazon.com Inc. for keeping prices low, but there’s another so-called “Amazon effect” that might be more relevant for central bankers.

That’s according to a paper presented Saturday by Harvard Business School economist Alberto Cavallo at the Federal Reserve Bank of Kansas City’s annual symposium in Jackson Hole, Wyoming.

The hypothesis that Amazon might somehow explain the relatively slow pace of inflation is false. If it were true, then high productivity growth would cause inflation to be lower than what one would expect based on growth in nominal wages, but it isn’t. Nominal wage growth is running at only 2.7% over the past 12 months.

The second “Amazon effect’ is more interesting:

Cavallo’s main finding was that competition from Amazon has led to a greater frequency of price changes at more traditional retailers like Walmart Inc., and also to more uniformity in pricing of the same items across different locations. He found that the shift has led to a greater influence of movements in the U.S. dollar exchange rate and gas prices on retail prices. . . .

The implications have subtle significance for monetary policy because so-called “sticky prices” — the notion that sellers aren’t able to change prices right away in response to changes in supply and demand — is precisely what gives interest rates power in mainstream models to have any effect on the economy at all. In those models, if prices adjust instantaneously in response to shocks, then there is no role for central bankers to guide supply and demand back into equilibrium.

It is true that there are models where monetary policy is only effective when prices are sticky. But these are just models and do not describe reality. In the real world, monetary policy has real effects because of the interaction of nominal GDP shocks and sticky wages. Even if all prices were 100% flexible, NGDP shocks would still impact real GDP. Macroeconomics went off course when models were built around price stickiness—that’s not the fundamental issue.

I’d add that it’s a bit odd to talk about there being “no role for central bankers to guide supply and demand back into equilibrium” in a world with no price stickiness. That’s true, but if monetary policy actually were ineffective in influencing real variables due to price flexibility, it would be precisely because supply and demand are always at equilibrium.

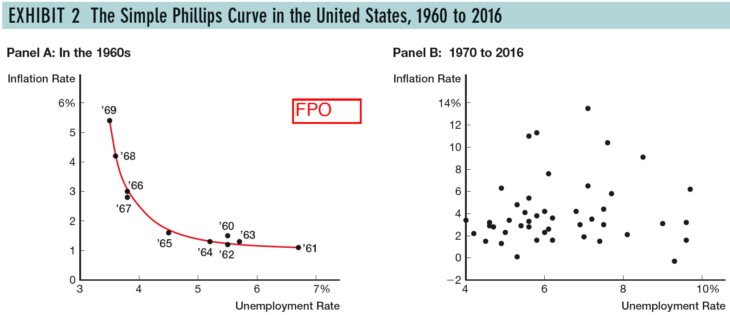

The article also discussed the Phillips Curve:

A paper published Thursday by top staff economists at the Fed’s Board of Governors in Washington cautioned against focusing too much on inflation and not enough on unemployment.

Part of the rationale is that in an environment like the present, where the relationship between unemployment and inflation seems to be weaker than it has been historically, external shocks to prices unrelated to domestic demand conditions could lead policy makers astray.

Actually, the relationship has been weak for quite some time:

Again, there is no low inflation mystery. Inflation has been running at levels that are consistent with the Fed’s monetary policy, which has been producing slightly above 4% NGDP growth. The Phillips Curve is not now and never has been a useful way to predict inflation.

Again, there is no low inflation mystery. Inflation has been running at levels that are consistent with the Fed’s monetary policy, which has been producing slightly above 4% NGDP growth. The Phillips Curve is not now and never has been a useful way to predict inflation.

READER COMMENTS

Market Fiscalist

Aug 26 2018 at 10:13am

I’m not quite following ‘Even if all prices were 100% flexible, NGDP shocks would still impact real GDP. ‘.

The only way I can see that prices could be 100% flexible would be if wages were also 100% flexible. And if I understand your model – if wages are 100% flexible then NGDP shocks would not affect RDGP. If amazon keeps the prices of all goods at their market clearing level and their is a demand shock then (if wages are sticky) firms will react to the shock largely by reducing supply rather than reducing prices, which does not really seem to qualify as 100% flexible pricing.

Jeff

Aug 26 2018 at 12:50pm

If all prices, including wages, are flexible, then every market is in equilibrium all the time, because prices adjust instantaneously to make it so. What Scott is saying is that if wages are sticky while prices are not, labor markets can get knocked out of equilibrium by NGDP shocks that are not effectively countered by monetary policy. This is standard Macro 101.

Scott Sumner

Aug 26 2018 at 4:01pm

Market, Then term ‘prices’ generally does not refer to wages. There is little to no evidence that wages are becoming more flexible, even as prices do become more flexible. I was reacting to the way the reporter described the implications of the research paper.

Ilya Novak

Aug 27 2018 at 3:22pm

Scott,

But then how would *your* preferred model predict inflation? What would you replace the Phillips Curve with? For example, would you use a Sumner Curve where instead of comparing inflation with unemployment you compare NGDP with total hours worked?

Comments are closed.