James Alexander has a new post discussing recent trends in NGDP growth in the UK:

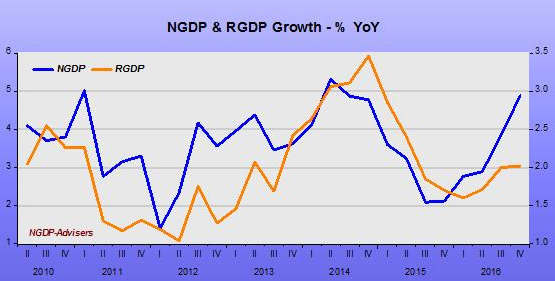

Unfortunately, the headline is a bit misleading. NGDP (left scale) grew at a 5.0% rate in the first half of 20172016, and a 4.6% annual rate in the 2nd half of the year.

James makes a mistake that I see quite often, using data before an “event” in an event study. He uses year over year data, which includes a 6 month period before the Brexit vote. It doesn’t seem likely that the Brexit vote in late June caused rapid NGDP growth in the first half of 2016!

Nonetheless, even a 4.6% NGDP growth rate is reasonably impressive—above the average NGDP growth rate of the last 5 years. Thus James is right that the BoE policy of monetary offset was effective. We’ll need another 6 months before the YoY data will consist of only data collected after the Brexit vote.

He’s also right that many critics of Brexit predicted a collapse in aggregate demand after the vote:

Anti-Brexiteers were all forecasting a collapse in AD following the vote. It was never clear if this was going to come from shocked consumers spending less, from dramatic falls in business investment, or maybe both. Nothing of the sort happened, as we now know. All those top economists and other experts were completely wrong.

But not all anti-Brexiteers expected a collapse in AD. The steady growth in AD (so far) is consistent with the market monetarist model.

READER COMMENTS

Matthew Moore

Feb 25 2017 at 10:26am

Inflation is the real danger now…

James Alexander also makes the rare but crucial point that whether the economic disruption is worthwhile depends on what political institutions you prefer, and how much.

I was in conversation last week with a man who observed that most previous generations of Britons had paid the blood price for parliamentary democracy, and we should consider ourselves fortunate to be paying only a modest gold price.

AntiSchiff

Feb 25 2017 at 11:13am

Dr. Sumner,

Very good points, but the mystery remains as to why there was no fall in real GDP after the Brexit vote. My guess is that expected benefits of Brexit exceeded expected costs. I might think there could be hits to real GDP to come later, but if so, why did the forex market respond so quickly?

Ilverin Curunethir

Feb 25 2017 at 3:33pm

This might be a typo with regard to the 2nd half of 2017?

Andrew_FL

Feb 25 2017 at 6:58pm

You have to be against British home rule to be a market monetarist, now.

Scott Sumner

Feb 25 2017 at 9:12pm

Antischiff, Brexit is still several years away. I expect Brexit to eventually lead to slower growth. Expectation of a weaker future pound will cause the pound to fall in value today.

Thanks Ilverin, I’ll fix it.

Andrew, Obviously not, where did you get that idea? Indeed I believe James is both a MM and a supporter of Brexit.

Andrew_FL

Feb 25 2017 at 11:42pm

I found this to be ambiguous phrasing, sorry.

Gabriel Cormier

Feb 26 2017 at 12:11am

I know you’ve been sckeptical of the “uncertainty theories” of the business cycle; but is it possible though that uncertainty towards Brexit and the future of the UK actually slowed RealGDP, wich was then in part offset by growing NGDP?

AntiSchiff

Feb 26 2017 at 10:26am

Dr. Sumner,

I hope you don’t mind if I ask a question about nominal exchange rates. If Americans, for example, suddenly decide to increase their domestic savings, nominal exchange rates for the dollar would fall, ceteris paribus. This would merely change the composition of real GDP in the short-run, not affecting short-run growth, correct? That is, more I and less C? Or, will real GDP growth fall in the short-run, but rise in the long run? Either way, I believe, real GDP growth rises in the long run.

I guess I have a related question if an increase in domestic savings would cause RGDP growth to fall in the short-run. In that case, would the fall in the nominal exchange rate be proportional to the short-run fall in RGDP growth?

James Alexander

Feb 26 2017 at 4:56pm

Thanks! Two points.

Annualizing any period of less than one year is pretty misleading. Far better to just state the actuals than multiply the noise in any GDP change.

You can be pro-Brexit and a liberal, in a good sense. Surveys show that at least 20% of the Brexit voters were so inclined. Many Remainers were liberal Brexiteers, but successfully frightened by all the warnings and now wonder what the fuss was about.

James Alexander

Feb 27 2017 at 5:01am

Thanks! Two points.

Annualizing any period of less than one year is pretty misleading. Far better to just state the actuals than multiply the noise in any GDP change.

You can be pro-Brexit and a liberal, in a good sense. Surveys show that at least 20% of the Brexit voters were so inclined. Many Remainers were liberal Brexiteers, but successfully frightened by all the warnings and now wonder what the fuss was about.

Scott Sumner

Feb 27 2017 at 8:45pm

Andrew, Yes, I guess that was ambiguous. I meant that I had this view, not all MMs.

Gabriel, Possible, but we’d need more data to establish that point. Uncertainly certainly seems less important than many pundits assumed.

Antischiff, I doubt that more saving would reduce RGDP, but it does depend on the response of the monetary authorities.

James, Best is to have a full year of good data.

Second best is to have 6 months of good data.

Worst is having 12 months of meaningless data. 12 months of 2016 data is meaningless.

You said:

“now wonder what the fuss was about.”

I’d suggest that they wait until Brexit occurs before reaching any conclusions as to its effects.

Comments are closed.