I’ve occasionally done blog posts explaining how it’s possible to prevent recessions from occurring, even after they have begun. That’s because a recession is dated from the point where output starts falling, but it’s not considered a recession unless the decline persists for a considerable period of time. This is one reason why economists are so poor at predicting recessions. During the past three recessions, a consensus of economists failed to predict the recession until it was well underway.

It occurred to me that I failed to provide an example of a recession that was prevented after it had already began. Today I will do so.

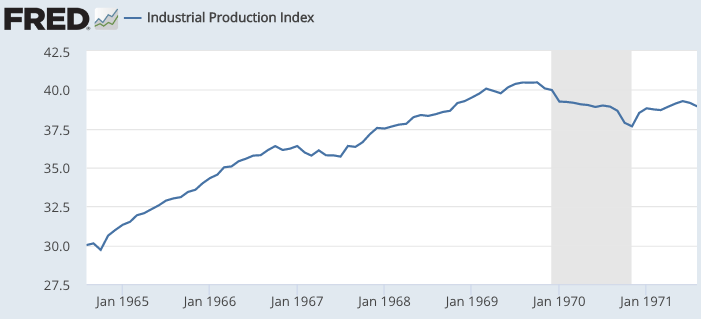

In 1966 the Fed tightened monetary policy to slow inflation, which had recently been increasing. As a result, industrial production fell by 1.9% between October 1966 and July 1967.

But that’s much less than the nearly 8% decline observed during the 1970 recession, which was itself fairly mild. We had no recession in 1967 because the Fed sensed a slowdown, and eased policy in the spring of 1967. Because of this action, unemployment merely nudged up from 3.6% in November 1966 to 4% in October 1967, before renewing its long decline.

Now let’s look at industrial production during late 2007 and early 2008:

After peaking in November 2007, industrial production fell by only 2.2% over the next 7 months. Then after June 2008, output fell sharply, and by June 2009 was more than 17.3% below pre-recession levels. June 2008 is considered a recession period whereas July 1967 is not, primarily on the basis of what happened later.

Unlike in 1967, the Fed decided not to ease monetary policy in the middle of 2008, despite growing signs of recession. Indeed policy was actually tightened sharply, as the fed funds target was held at 2% from April to October, despite a rapidly falling natural rate of interest. If the Fed had eased aggressively in June 2008, then they might have entirely prevented a recession that technically began in December 2007. It wasn’t too late!

The decline in output from late 2007 to June 2008 was too small to constitute a recession. Yes, the NBER eventually declared that the recession began in December 2007, but there would have been no recession to date in the first place if industrial production had risen in the second half of 2008, as it did in the second half of 1967. (I would add that the post-Lehman crisis might also have been milder, indeed Lehman might not have even failed.)

Ironically, the Fed made the wrong call in both 1967 and 2008. In 1967 the Fed should have allowed a (very mild) recession to occur, in order to prevent the “Great Inflation” of 1966-81 from occurring. That inflation did far more damage than a rise in unemployment to, say, 5% in late 1967. Indeed, a mild recession in 1967 might have made the 1970 recession unnecessary. In contrast, the Fed should have prevented the 2008 recession.

In 1967, the Fed was too worried about unemployment and not worried enough about inflation, whereas the reverse was true in 2008. The solution is to ignore both inflation and unemployment, and focus on keeping NGDP growing at a stable rate.

Even at the low point of the second quarter of 1967, 12-month NGDP growth was running at over 5.4%. There was no reason at all for the Fed to ease monetary policy. By the 3rd quarter of 1968, 12-month NGDP growth had soared to 9.9%—the Great Inflation of 1966-81 was underway. Now look at NGDP growth in early 2008:

In the second quarter of 2008, the 12-month NGDP growth rate was only 2.7%. Admittedly this data was not yet available to Fed officials in June 2008, but even the first quarter data showed only a 3.05% NGDP growth rate—far below trend.

So why did the Fed (passively) tighten policy in mid-2008, by keeping rates at 2% as the natural rate of interest plunged sharply lower? In a word, inflation. An economic boom in developing countries such as China pushed global oil prices to a peak of $146/barrel in mid-2008. In the US, 12-month (PCE) inflation rose to a peak of 4.2% in July 2008, far above the Fed’s 2% target. (CPI inflation reached 5.5%). Even though the Fed was aware that oil prices were distorting the data, they were so frightened of losing credibility on inflation that they allowed monetary policy to tighten sharply.

The Fed should have focused on NGDP growth, which was falling to dangerously low levels. As long as NGDP growth is kept at a modest level, any rise in inflation due to soaring oil prices will be transitory. Indeed by the end of 2008, the 12-month PCE inflation rate had plunged to below 0.4%, far below the Fed’s target. So one of the many causes of the Great Recession was the focus on inflation, when the Fed should have actually been focusing on NGDP growth. Indeed this mistake is now so obvious that it goes a long way toward explaining the rapid increase in support for NGDP targeting.

PS. I am indebted to Robert Hetzel for educating me on the situation in 1967. However he is not to blame for any mistakes in this post.

PPS. I recently read a very interesting Time magazine article from December 1965, entitled. “We are all Keynesians now“. It’s amazing how confident people were back then that we had it all figured out.

READER COMMENTS

Todd Kreider

Oct 14 2017 at 11:51am

I don’t think the data support this narrative.

First, China was already growing at over 10% from 2003 and this increased to 13% in 2006 and 2007 before falling sharply at the beginning of 2008 so China’s economy had been “booming” for years.

China’s oil imports doubled in 2001 from 1.2M bbl/day to 2.4M bbl/day and the price of oil in today’s dollars was flat at $31 a bbl. The rise in imports slowed signficantly in 2002 and 2003 and was flat in 2004 as the price of oil increased to $63.

China’s oil imports increased 15% a year in 2006 and 2007 as the price increased to $75 a bbl. In 2007, China’s oil imports increased only 4%, and this level of increase held in the great recession years of 2008, 2009 as well as to 2013.

From 2003 to latet 2007, the economies of the rich countries (where most of the cars and trucks are) were growing at full speed at 2% per capita. Of course, OPEC was a major factor as well.

China’s oil imports from 2001 to 2013:

https://www.indexmundi.com/g/g.aspx?c=ch&v=93

Cyril Morong

Oct 14 2017 at 1:37pm

“I recently read a very interesting Time magazine article from December 1965, entitled. “We are all Keynesians now”. It’s amazing how confident people were back then that we had it all figured out.”

Maybe that is why Hayek said Nobel Prize winner in economics should have to take an oath of humility

Andrew_FL

Oct 14 2017 at 3:22pm

I believe this is the first time I’ve ever heard a monetarist say that using loose money to avoid a mild recession lead to a worse recession later.

Thaomas

Oct 14 2017 at 6:19pm

But what if they had been focusing on their preferred core price level and everyone knew that they would return the PL to trend if it departed?I agree that NGDP level targeting might have gotten a quicker response, but even PL targeting would have prevented the “greatness” of the Great Recession.

But I do not think this was an intellectual error. the politics of the Feb board and Republicans in Congress was that they did not want the Fed to do what it would have taken to restore the PL. To paraphrase WJC, “it’s the (political) economy, stupid.”

Marcus Nunes

Oct 14 2017 at 9:05pm

From the Time article:

“In Washington the men who formulate the nation’s economic policies have used Keynesian principles not only to avoid the violent cycles of prewar days but to produce a phenomenal economic growth and to achieve remarkably stable prices.”

At exactly the same moment, Gardner Ackley, CEA Chairman wrote:

“The Contribution of Economists to Policy Formation” delivered in December 1965:

“…The plain fact is that economists simply don´t know as much as we would like to know about the terms of trade between price increases and employment gains (i.e, the shape and stability of the Phillips Curve). We would all like the economy to tread the narrow path of balanced, parallel growth of demand and capacity utilization as is consistent with reasonable price stability, and without creating imbalances that could make continuing advance unsustainable. But the macroeconomics of a high employment economy is insufficiently known to allow us to map that path with a high degree of reliability…It is easy to prescribe expansionary policies in a period of slack. Managing high-level prosperity is a vastly more difficult business and requires vastly superior knowledge. The prestige that our profession has built up in the Government and around the country in recent years could suffer if economists give incorrect policy advice based on inadequate knowledge. We need to improve that knowledge”.

Just like when the press touts the stockmarket at the peak!

Marcus Nunes

Oct 14 2017 at 9:10pm

This provides a history of the time:

https://thefaintofheart.wordpress.com/2012/08/25/the-origins-of-the-great-inflation/

Scott Sumner

Oct 15 2017 at 1:51pm

Todd, That graph shows Chinese oil imports rising from 1.2 to 4.2 million between 2001 and 2007, which is a huge increase. It doesn’t support your comment at all.

Todd Kreider

Oct 15 2017 at 3:03pm

Scott, my comment detailed both import increases and prices over that period and beyond when oil prices collapsed.

If you say China’s oil imports increase from 1.2 million bbl/day to 4.2 in 2007 is ‘huge’, then you acknowledge that the increase from 1.2 million bbl/day in 2001 to a doubling of 2.4 million in 2002, a full 40% of that increase in just one year, is ‘very large,’ right? Yet the price of oil in today’s dollars went from $32 per barrel in 2001 to $31 per barrel in 2002. How does your oriinal statement support China importing significantly more oil cause the price to drop?

(China’s oil imports went from a little more than 1% of the world’s total oil production in 2001 to a little more than 2% of the total oil production in 2002.)

But then oil imports slowed dramatically to just a 15% increase average in 2003 and 2004 and a small decrease in 2005. As a result, the price of oil went from $49 to $63 bbl/day, a 30% increase. Did China decreasing its oil imports really contribute to that 30% price hike that year?

By the summer of 2008, the price of oil had increased almost 100% from 2007, yet Chinese oil imports the previous year and that year were once again only about 15+% larger on average.

It wasn’t China’s growth but speculation in the oil markets with the help of a cartel that forced prices to double in 2008.

Fun fact: China imported around 8 million barrels a day last year, twice as much as when oil hit $145 in 2008. The price of oil the last two years has been around $40.

Scott Sumner

Oct 16 2017 at 12:09am

Todd, You can’t just look at year to year changes because there are lots of other factors impacting the price. In 2002 the developed world was depressed, and this held down prices. After 2002, Chinese demand rose along with a recovering demand in developed countries.

Of course since 2008 we’ve had the fracking revolution, so I don’t see your point about comparing prices in 2008 and today. That comparison seems meaningless.

Again, your data in no way refutes my claim that growth in developing country demand for oil was pushing up prices in the period around 2007 and 2008. Chinese imports were 3 million barrels a day above 2001 levels—that’s a lot.

Todd Kreider

Oct 16 2017 at 9:52am

Scott, you originaly pointed to just one cause: China and India’s economies booming even though there wasn’t much of a boom beyond the baseline high growth for China and no boom in India with its lower strong sustained growth then. I pointed out that wealhier countries experienced heathy 2% growth from 2003 to the end of 2007. Unlike many other periods, including post recession, world oil production was almost flat from 2005 to 2008 thanks to our friends at OPEC. Supply is just as important as demand.

World supply of oil:

2005 81.9 million

2006 82.5 million

2007 82.3 million

2008 82.9 million

One cannot point to China’s modest increases in oil imports in 2006 and even less so in 2007 for a 100% spike in the price of oil a year later in 2008.

I brought up 2001/2002 to show that other factors come into play beyond China’s doubling of oil imports in 2002, which lead to a slight decline in the price of oil. 2.4 million bbl/day in 2002 was “a lot” more than 1.2 million barrels a day in 2001.

China’s oil imports kept increasing after the 2008/2009 recession yet the price of oil plummeted. The world supply of oil kept increasing only after 2005 to 2008 as once again after the recession OPEC lost its cartel power to keep prices high.

Scott Sumner

Oct 16 2017 at 3:15pm

Todd, You said:

“Scott, you originaly pointed to just one cause: China and India’s economies booming even though there wasn’t much of a boom beyond the baseline high growth for China and no boom in India with its lower strong sustained growth then.”

That’s not accurate. I said “developing countries”.

China’s oil consumption (imports plus domestic) rose by nearly 4 million barrels per day between 2001 and 2007. If it had just risen at the pace of the rest of the world, oil prices in 2008 would have been dramatically lower, probably peaking far below $100 barrel. Nothing you say in any way undercuts this claim.

Yes, the recovery in developed countries played a role too, as did sluggish output growth, but it was China’s extraordinary growth in demand that pushed oil prices into the stratosphere.

Todd Kreider

Oct 16 2017 at 4:44pm

Here is China’s oil consumption, domestic plus imports:

2001 4.8 million bbl/day

2002 5.2 million

2003 5.8 million

2004 6.8 million [$49 bbl]

2005 6.9 million [$64 bbl] (no increase in oil consumption but price rose 30%]

2006 7.4 million [$71 bbl]

2007 7.8 million [$76 bbl]

2008 7.9 million [$101 bbl] (no increase in oil consumption but price rose 33%)

2009 8.3 million [$61 bbl]

You wrote that “it was China’s extraordinary growth in demand that pushed oil prices into the stratosphere.” But oil prices only went into the stratosphere to double at $140 in the summer of 2008 when China’s oil consumption didn’t increase.

You also say “sluggish output” played a role, yet it was the OPEC countries colluding to ensure supply did no rise, thereby forcing the price hike. Maybe picky but “sluggish” doesn’t convey deliberate intention to cap supply from 2006 to 2008.

China, India and other developing countries oil incraeses may have had a role but not a leading one relative to strong increases in demand in wealhthier countries running full steam the years leading up to the great recession and OPEC manipulaion.

OK, I’m done.

Comments are closed.