George Selgin has a new post discussing three pieces of legislation being considered by the Senate. Here’s one:

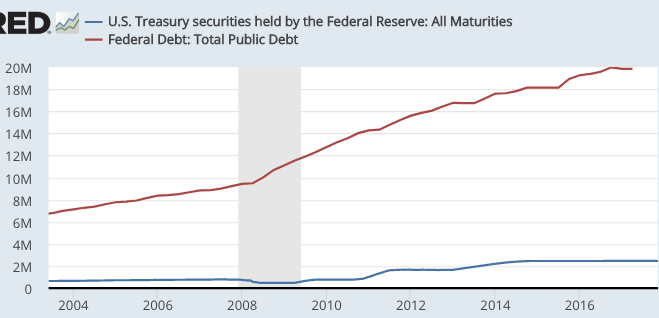

The Independence from Credit Policy Act (H.R. 4278), introduced by Rep. French Hill (R-AR), is intended to restrict the Fed’s asset holdings, apart from gold, foreign exchange, and IMF-issued SDRs, particularly by requiring it to swap its current MBS holdings for Treasury obligations. In future emergencies the Fed could temporarily acquire certain non-Treasury assets in connection with its 13(3) lending operations (concerning which see below); but it would be allowed to hold such assets for no more than a year, after which it would also have to trade them in for Treasury securities.

I have mixed feelings about this proposal. I would prefer the Fed hold Treasuries rather than mortgage backed securities, but I also worry about restrictions that might be perceived as limiting the ability of the Fed to hit its targets when at the zero bound. Here are a few provisions that could be added to this sort of bill:

1. The restriction on asset purchases could be limited to periods where the Fed holds less than 50% of Treasury securities outstanding. As far as I know, the Fed has never come close to that milestone, so the bill would still have exactly the effect its proponents hoped for, under all but the most unusual circumstances. But this provision would also make clear that the Fed never “runs out of ammunition” and hence make its policy commitments more credible.

2. I also think it would be helpful for legislation to spell out more clearly what Congress wants and expects from the Fed when at the zero bound. Thus Congress might want to instruct the Fed to do whatever it takes to achieve its Congressional mandate (currently stable prices and high employment, but I’d prefer stable NGDP growth.) Congress should tell the Fed that macroeconomic stability is far more important than any profits or losses on the Fed balance sheet. The Fed should be told that it is free to set the rate of interest on reserves at negative levels. (That’s assuming we keep IOR; I’d prefer the entire policy be abolished, as it has not worked well.)

Trying to keep the Fed focused on monetary policy rather than credit allocation is an entirely laudable goal. Indeed I might go even further, and recommend abolishing the discount window. But I also think we need to focus not just on limiting what the Fed can do, but also making it clearer that we want them to do whatever it takes to hit the more limited goals that we provide. We need less credit allocation and more macroeconomic stability.

READER COMMENTS

bill

Nov 12 2017 at 3:17pm

I’m in favor of allowing negative IOR.

I’d be OK with positive IOR but with restrictions. The most important one being that the rate of IOR be set at least 100bps to 200bps below market rates. I can appreciate that the banks disliked getting 0% on reserves when LIBOR was 5%. And I really dislike that the Fed is now paying the banks a higher rate on reserves than the Treasury will pay me for 90 day money.

Thaomas

Nov 12 2017 at 5:25pm

It’s mainly symbolism. The Fed could still purchase unlimited amounts of foreign currency securities

Jake

Nov 12 2017 at 8:56pm

I think this is good policy. The Fed doesn’t really need to purchase anything other than treasuries to stabilize NGDP growth, right? The problem is they weren’t willing to.

The idea of the Fed trading in private sector securities has always been unsettling to me. Or for that matter the central banking system in general.

I feel like if we had a Fed that was solely committed to achieving stable NGDP growth, most of the rest of macro would work itself out.

Scott Sumner

Nov 13 2017 at 10:19am

Bill, I agree.

Thaomas, I wonder if they feel inhibited regarding buying foreign securities, as we criticize other countries for doing this. (“Currency manipulation”)

Jake, It depends how many securities they need to buy, and how many are outstanding. So far they have not needed to go beyond Treasuries, but there are countries where the monetary base is now close to 100% of GDP (Japan, Switzerland)

LK Beland

Nov 13 2017 at 11:02am

The Fed balance sheet is $4T or so; a bit less than $2T in MBSs. Say that it bought assets in a way that highly distorted the market for MBSs–which is debatable. By how much did it distort this market? Suppose that it propped up prices in MBSs by 20%–$400G. That’s a one-time distortion of an asset price of the order of 2% of GDP. How much of a drag has these been on the economy? Maybe 0.2% of GDP?

That’s a small number compared to the effects of keeping the level of NGDP on track–or not–over the 2007-2017 period.

Matthew Waters

Nov 13 2017 at 5:55pm

My first thought reading this bill was the 40% required gold backing of Federal Reserve notes and deposits in 1931.

I know there is significant debate about how much blame the Fed should have for 1931-32. But I found the Milton Friedman narrative unconvincing for 1931-32. The Federal Reserve had to adjust their policy for the other 60%, discount window and OMO’s, in light of keeping the statutory 40% gold backing.

IMO, we could dramatically alter the idea of the Fed, ending discount window, daylight overdrafts and the current OMO structure. Much of the Fed’s actions are wrongly centered around it being like a normal bank, with technical “shareholders” and P/L statements.

The Fed could instead just make open offers to buy Treasuries and, if necessary, just make credits to the Treasury General Account with no debit. If inflation needs to be reduced, raise IOR instead of selling Treasuries. (I didn’t say it would be politically popular, just technically possible).

Comments are closed.