It’s very possible that I’m missing something important, but right now I’m having trouble following the media discussion of the US-China trade war. Let’s start with the obvious:

1. China’s exports to the US are a modest share of their GDP (about 3.5%).

2. The proposed tariffs apply to only a fraction of Chinese exports (roughly 50%).

3. Chinese industries tend to be highly competitive.

4. The US would have difficulty finding these goods from an alternative source, at least in the short run.

Put those facts together, and damage to China’s GDP will probably be less than 0.5% of GDP. That’s not pocket change, but it doesn’t seem to explain why Chinese stocks have fallen so sharply.

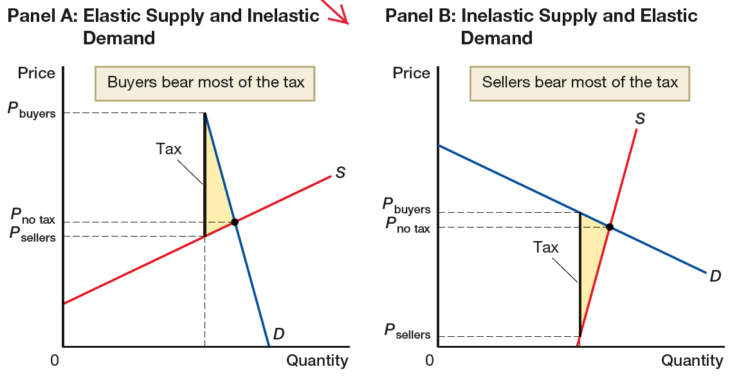

Here it might be useful to review the basics of tax incidence. One key idea is that the side of the market with the less elastic curve bears the largest burden of the tax:

When considering US imports from China, Panel A is clearly a better fit. Because China’s export industries are highly competitive, the supply of Chinese exports is highly elastic.

When considering US imports from China, Panel A is clearly a better fit. Because China’s export industries are highly competitive, the supply of Chinese exports is highly elastic.

In many cases, it’s a disadvantage to have competitive industries. Thus firms in countries like the US and Switzerland often have a great deal of market power, as they produce goods with a high level of intellectual content (think about pharmaceuticals and precision machines from Switzerland, or high tech goods and movies from the US). This allows for a relatively high rate of profit on our exports. Chinese firms making zippers or sneakers are in a ruthlessly competitive industry, where profit margins are slim.

But this negative (for China) turns into a positive as soon as another country tries to tax their output. China’s producers cannot profitably export the goods at a significantly lower price, and hence the tax gets passed on to consumers in the importing country. Thus it seems to me that tariffs would hurt the US more than China.

Of course, there are lots of other factors to consider:

1. Perhaps tariffs on Chinese goods would cause output to shift to other countries. Obviously, consumers will still be going to Walmart and buying products like sneakers and Christmas ornaments. But they’ll be made elsewhere. The problem here is that in the short run there’s no one else to fill the gap. While the tariffs on Chinese goods may divert production to some extent, the overall effect will be modest in the short run. In addition, the Chinese yuan will depreciate, which will further mitigate the impact of tariffs. Thus China will keep exporting the same stuff to America in the short run, and US consumers will pick up the tax.

2. In the long run, the effects of tariffs could be much greater. Output will shift to other regions as the US begins buying more from places like Vietnam (a process already underway due to rising Chinese wages.) This certainly harms China to some extent, as their alternative sectors may not be as profitable as the foregone exports to America. But it seems unlikely that the trade war will continue in the long run. The Chinese surely know that President Trump is highly unpopular, and also that he likes symbolic “wins”. In addition, tariffs on Chinese inputs would put US producers who rely on those inputs at a competitive disadvantage to producers in Germany, Japan and Korea, which also rely on Chinese inputs. I don’t see why the Chinese would feel any need to negotiate with Trump, except perhaps to offer a few meaningless face-saving gestures.

The counterargument is that Chinese stocks have recently done poorly, which might be due to the threat of a trade war. It’s not clear that this is solely due to tariff fears (there’s also concern about the recent government crackdown on the Chinese property sector), but it’s probably at least partly due to the tariffs. So there’s a decent chance I’m wrong in my assumption that Chinese exports will hold up well. Perhaps in higher end manufacturing it will be less difficult to source the goods from alternative countries (including the US), and hence Chinese exports might fall by more than I assumed. But I’m skeptical that the US can wait long enough for these alternative supply lines to develop.

When Siamese twins get into a knife fight, it’s hard to envision either side winning.

PS. The initial tariffs will be 10%, rising to 25% in January. My hunch is that the trade war will be over by February—as the 25% tariff would be too disruptive to the US economy. I predict an outcome much like the Nafta renegotiation—not much change in current trading patterns.

READER COMMENTS

Benjamin Cole

Sep 18 2018 at 9:29pm

I largely agree with this post.

The tariffs considered are a relatively minor structural impediment, perhaps 1% or so as large as domestic property zoning.

The Shanghai composite is in bear territory. Perhaps the answers lie in the monetary policy of the People’s Bank of China. It has not moved aggressively enough to promote growth.

Still, the tariff tiff has had entertainment value.

Money makes for strange bedfellows.

Whoever thought that the US Chamber of Commerce would become a mouthpiece for the Chinese Communist Party?

Scott Sumner

Sep 19 2018 at 12:11am

Ben, You said:

“Whoever thought that the US Chamber of Commerce would become a mouthpiece for the Chinese Communist Party?”

These sorts of comments are kind of pointless. You obviously don’t have shred of evidence that this is true, so why say it?

Benjamin Cole

Sep 19 2018 at 9:59am

Scott

I am surprised at your comment.

As Milton Friedman said, and I concur, corporations (including public companies and multi-nationals) have no social or national obligations. Their only obligation is to comply with law, and then meet all-encompassing fiduciary obligations to shareholders.

Multi-nationals are not “for or against” human rights, or “for or against” free trade.

Multi-nations should be, and are properly for trade agreements (free, or not, or even totally corrupt) that maximize their profits, and they should care nothing about human rights.

As we see.

Also, the multi-nationals can pour unlimited funds into US elections, media, think tanks, academia.

Thus:

“The U.S. Chamber of Commerce, another trade industry body has argued in a new campaign that 2.6 million American jobs could be lost as a result of “recent and proposed trade actions by the Trump administration.”

Scare-mongering is okay too.

Since multi-nationals have established a gigantic base of operations in mainland China, which is run by the China Communist Party (and ever more tightly) they are now necessarily mouthpieces for the CCP.

Indeed, in honoring their fiduciary obligations to shareholders, multi-nationals are usually mouthpieces for whoever is in charge in any particular nation.

You don’t see the oil guys bad-mouthing Saudi Arabia.

Is this even debatable?

Benjamin Cole

Sep 20 2018 at 12:02am

Oh, I missed a chance to use one of my favorite words: “amoral.”

This word, often misused, is valuable in economics.

Economic actors in free markets are amoral, not immoral.

Multi-nationals are not immoral when they do business with the Communist Party of China, they are amoral. And they should be amoral, as Milton Friedman prescribes.

Consider Rex Tillerson, former Chair/CEO of Exxon, and Secy of State.

Tillerson, when at Exxon, won the Russian Medal of Friendship, awarded personally by Putin in a ceremony, after signing deals with the state-owned Russian oil company Rosneft, whose chief, Igor Sechin, is seen as Putin’s loyal lieutenant.

I cannot imagine that an intelligent, worldly fellow like Tillerson was unaware of the nature of Putin or the thug-state he runs.

But Tillerson, as chair/CEO of Exxon, had an obligation to be amoral, and honor fiduciary obligations to shareholders. If you owned shares of Exxon, it warned the cockles of your (financial) heart to see Tillerson cut deals with Putin.

See multi-nationals in China.

Mark

Sep 19 2018 at 7:59am

The direct impacts of the tariffs may be limited as you say, but I (and apparently very global investors) am very worried that they will prompt increased nationalist sentinment in China and cause the Chinese government to increase its control over the economy and investment.

Scott Sumner

Sep 19 2018 at 11:48am

That’s certainly a concern.

Jon Murphy

Sep 19 2018 at 8:00am

I also suspect that assuming China is relatively more protectionist than the US, they have less to lose in a trade war than the relatively open US.

The US has realized the gains from trade liberalization. Further liberalization will beneficial, yes, but not hugely so. China, on the other hand, if they are relatively protectionist, has a lot more gains to realize. They would stand to benefit from increased trade significantly so.

Thus, in a trade war, China would have less to lose. They are not realizing the gains from open trade, and thus reducing trade wouldn’t make them significantly worse off. It would, however, be that way for the US.

By way of metaphor, consider the following: let’s say a doctor says exercise and a good diet are key for healthy living. He gives this advice to two people: one who exercises an hour a day and eats well, the other who is a couch potato and eats fried and fatty foods. Who would benefit most from the doctor’s advice? Obviously the latter; the former is already doing the doctor’s orders. However, if one were to measure the effectiveness just by looking at the former, it would look like the extra exercise was ineffective! It would be erroneous to conclude that exercise and a good diet are not very beneficial by looking at the minimal change in the health of someone who is already eating well and exercising. Likewise, whose health would deteriorate more from eating fatty foods? The unhealthy person or the healthy person? The unhealthy person’s already done the damage. Any additional food wouldn’t have the same effect as eating by the healthy man.

Warren Platts

Sep 19 2018 at 12:06pm

Actually, assuming your premise, and applying optimal tariff theory, one gets the opposite conclusion: China has much more to lose. According to Torrens’s theory, when a unilateral free trade country goes up against a mercantilist country, the mercantilist country comes out on top. In the present case, USA is paying fat terms of trade gains to the Chinese; meanwhile USA lets in Chinese goods in tariff-free. So the USA is already suffering terms of trade losses. Thus when we impose 25% tariffs on Chinese goods, the resulting terms of trade gains offset the terms of trade losses we were already paying, thus improving our relative position.

As for Chinese retaliation, the former regime was likely already at or even somewhat above their optimal tariff is. For example, the landed cost of Vermont maple syrup is 48%, not counting shipping. Much above that, and their tariffs and other fees become prohibitive, and the resultant terms of trade gains become less. Thus, China loses on both fronts: they suffer terms of trade losses on their exports because of U.S. tariffs; meanwhile their retaliatory tariffs have the effect of lowering the terms of trade gains they were extracting from U.S. producers.

Jon Murphy

Sep 19 2018 at 3:58pm

The optimal tariff model is completely irrelevant here

Warren Platts

Sep 19 2018 at 4:54pm

That is called begging the question.

Jon Murphy

Sep 19 2018 at 7:38pm

No, it’s called “knowing the model.”

Warren Platts

Sep 20 2018 at 11:02am

You are ignoring optimal tariff theory because it does not give the answer you want, not because it is irrelevant. Conclusion of Balisteri & Hilberry (2017):

Jon Murphy

Sep 20 2018 at 12:08pm

This is your chance to prove to everyone your claim that you know this material better than the experts.

Merely asserting that the model fits here and resorting to ad hominum will win you no favors.

Not too long ago, you quoted Paul Krugman (among others) explaining exactly why the optimal tariff model is inappropriate for this situation.

I wonder: can you tell me why Krugman, Samuelson, Humphries, and all the others you love to cite say the optimal tariff model is inappropriate for this situation? Further, can you then explain why they are wrong?

Hint: merely asserting you are right while repeating the model ad nauseam in the vain hopes it will suddenly become true will not do.

Warren Platts

Sep 20 2018 at 1:05pm

That is a mere assertion for which you have not a shred of evidence. It doesn’t even make sense. For one thing Samuelson isn’t even alive, so how can he say optimal tariffs are inappropriate for Trump’s trade war? If you cannot make a substantive comment, why do you even bother to comment?

The model I quoted from above is a general equilibrium model that specifically analyzes then-candidate Trump’s threatened tariffs and any potential retaliations. It is certainly more applicable than your extemporaneous, couch-potato speculations.

Jon Murphy

Sep 20 2018 at 1:39pm

We can clearly see you have nothing to offer other than mere assertions and ad hominem and non-sequiturs. You had an opportunity to showcase your brilliance, and you let it go. (Also note that the comment you made about the paper is directly contradicted by the part you quote and bolded in your comment).

By that same logic, Torrens is dead, so how could he have anything to say on Trump’s trade war?

Warren Platts

Sep 20 2018 at 3:13pm

This is a useless comment, apparently psychological projection.

And this does not even make sense. I said Balistreri’s model was a general equilibrium (GTAP) model, and it is; and I said it was an attempt to specifically model Trump’s tariffs, and it is. Therefore, the most charitable interpretation of your comment is that you have not even glanced at the paper.

This is finally something resembling a decent question. And the answer to your question is that Torrens was the father of optimal tariff theory, and that optimal tariff theory is necessary to properly analyze a trade war.

Indeed, that is exactly what Scott attempted to do in this here article.

Look at the panels again. They depict the terms of trade gains predicted by optimal tariff theory. In Scott’s nomenclature:

Terms of Trade Gain = [P(no tax) – P(sellers)] x Quantity Supplied

In Panel A, the terms of trade gain is tiny; in Panel B, there are are great terms of trade gains.

Thus Scott provided some pretty good reasons to think that if USA imposes tariffs on China, USA is in Panel A territory–buyers (i.e., U.S. consumers) pay most of the tariff tax incidence, and thus the resultant terms of trade gains will be negligible. That is optimal tariff theory, whether you, sir, realize it or not.

All I did was point to published estimates of elasticities that seem to point to the opposite conclusion (that USA is in Panel B, and China in Panel A), and point to a published GTAP study that reached a similar conclusion, that the USA will be relatively better off than China in a trade war.

But either way, optimal tariff theory is being used to analyze the trade war. Therefore, if you have a problem with that, then why are you screaming at me? Take it up with Scott, and call him a bunch of names, given that is apparently the best you can do.

As for Samuelson, I call BS. Nowhere in any one of the 1,000 papers that he wrote did he ever write that “the optimal tariff model is inappropriate for this situation [Trump’s trade war],” as you say, or any other trade war for that matter. If you can provide a quote from Samuelson that optimal tariff theory is “inappropriate” for analyzing trade wars, I will eat my hat…

Jon Murphy

Sep 21 2018 at 9:03am

Come now, Mr Platts. This was your great big opportunity to prove how smart you are. You had a chance to outshine two Nobel Prize winners (Samuelson and Krugman) and prove that their claims, that an optimal tariff is not appropriate to model a trade war, are incorrect. You had a chance to show the claim in the very paper you quoted, that optimal tariffs are not appropriate to model the current trade war, is incorrect (I highly recommend you re-read the paper much more carefully then you have done, especially the conclusion and the part you bolded).

And your response? Mere assertions that you’re right, despite all evidence to the contrary that you present, and name-calling. What are people to think?

Warren Platts

Sep 21 2018 at 10:32am

Jon, it is either the case you do not bother to read the stuff you comment on, or else you have no clue what optimal tariff theory even is. I hope for the sake of the reputation of your department that it is the former.

Since you apparently did not read my previous comment, for the 2nd time, Scott Sumner himself uses optimal tariff theory in this very blog post. Read it!

As for Krugman, you of course could not be more wrong, as 5 seconds of googling would have told you. Top hit: nytimes article dated June 17, 2018. Read it!

As for Samuelson, you are obviously making stuff up, just like you did about Krugman. Sad. I don’t know about Nobel Prize winners, but it sure is easy to outshine George Mason University graduate students!

Amy Willis

Sep 21 2018 at 1:51pm

Warren Platts

Sep 19 2018 at 11:42am

Tokarick (2010, IMF working paper WP/10/180) estimated import demand and export supply elasticities for practically all economies, including the United States and China.

Using his estimates, we can calculate the expected average tariff tax incidence. For U.S. tariffs on China, the short run and long run supply elasticities are 0.79 and 1.1, respectively (these figures include general equilibrium effects). For the U.S. import demand elasticities, they are -1.09 and -1.52 for short and long run.

The formula for the supplier tax incidence is Ed/(Es + Ed). For both the short and long run, China would bear about 58% of the tax incidence, implying that U.S. producers would eat 42% of the cost. Thus if we accept Tokarick’s numbers, then your Panel B above would be the one that would apply.

As for U.S. exports to China, the U.S. export short and long run supply elasticities are 1.29 and 1.77 respectively. For China import demand elasticity, the numbers are -0.44 and -0.61, implying that Chinese consumers would bear 75% percent of the tariff tax incidence (Panel A).

Thus, either way, using Tokarick’s numbers, the USA comes out on top.

Scott Sumner

Sep 19 2018 at 11:51am

I don’t understand those supply elasticity estimates; they make no sense to me at all. I would expect them to be far higher. But then I have not studied the question.

Warren Platts

Sep 19 2018 at 12:19pm

Tokarick’s estimates were based on GTAP models that included value-added, import & export data in 57 sectors, and included general equilibrium effects. I don’t claim to understand it, but it looks like he did his homework. As for passing the smell test, I have seen published elasticities for crude oil on the order of 0.1, to his estimates are perhaps not too far out of line. They could be a bit dated.

If one looks at soybeans, China’s 25% tariff apparently caused a 20% drop in U.S. prices. So if the starting price is indexed to 100, it then dropped to 80, and 25% of 80 is 20, implying that U.S. producers are eating 100% of the cost of the soybean tariff, at least. But I would say that is an extreme case of inelastic supply: the crops are already in the ground, so U.S. farmers are committed this year. Next year no doubt many would substitute other crops that have less exposure to Chinese tariffs.

Hazel Meade

Sep 19 2018 at 12:34pm

My thought is that it could harm US products in international markets, because it will force US companies to source inputs more expensively. That could indirectly benefit China. it could even harm US products in domestic markets in some cases, compared to non-Chinese competitors that are able to source the same Chinese parts without tariffs.

Benjamin Cole

Sep 23 2018 at 4:46am

Well, I do not know if anyone is reading anymore, but regardless of your biases or intrepied and true beliefs on China, here is an observation:

BUSINESS NEWS

SEPTEMBER 7, 2018 / 4:17 PM / 16 DAYS AGO

China to increase export tax rebates on 397 products

2 MIN READ

BEIJING (Reuters) – China said on Friday it will increase export tax rebates for 397 items ranging from some steel products to electronic ones, in a bid to boost prospects for shipments amid its trade war with the United States.”

—-30—-

Okay, so it goes like this: The US raises tariffs on Sino products.

Beijing increases VAT tax rebates to exporters.

The price to US consumers remains the same. China loses some tax revenue, and the US gains tax revenue.

It is too much to hope, but one could argue that now the US can cut domestic taxes by a like amount.

Comments are closed.