The Fed says no.

Many Fed critics say yes.

I say that it’s too soon to say.

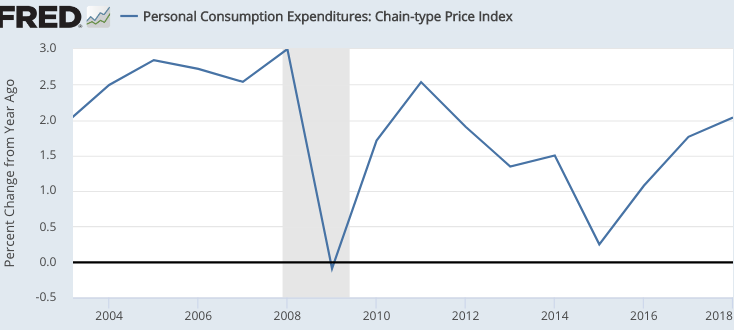

Let’s look at PCE inflation (the index targeted by the Fed) over the past 15 years:

Inflation has exceeded 2% in seven years and fallen short in eight years. That’s consistent with a symmetrical target. So why do critics like David Beckworth argue that the Fed treats 2% as a ceiling?

The real problem is quite recent. The Fed has fallen short of 2% in 6 of the past 7 years, and 8 of the past 10 years. My view is that the shortfall around 2009-10 was intentional, as the critics maintain. But I also believe that the more recent errors have been mistakes, and that the Fed does sincerely favor a symmetrical 2% target.

Fed critics seem to have “Occam’s razor” in their favor. Isn’t the simplest explanation that the Fed is aiming for 2% or less, rather than that they make repeated mistakes?

In fact, I believe Occam’s razor works in the opposite direction, in favor of my hypothesis. In this earlier post I pointed out that over the past decade the private consensus forecast has also consistently overestimated future inflation. My theory is that both private forecasters and Fed economists made the same mistake, relying too heavily on “Phillips Curve” models of inflation.

In contrast, Fed critics need an excessively complicated explanation:

1. The Fed has not had a low inflation bias over the past 15 years, but did adopt such a bias roughly 10 years ago.

2. Private sector forecasters consistently underestimated overestimated inflation over the past decade for reasons unrelated to the bias in Fed policy, perhaps excessive reliance on the Phillips Curve.

3. The Fed made similar mistakes to private sector forecasters, but for completely unrelated reasons. Unlike private sector forecasters, the Fed knew they were likely to undershoot 2% inflation, but lied and claimed they were on track in order to please . . . . someone.

Many people have a lot of trouble with my claim that the Fed innocently made repeated errors in the same direction. But any theory must be consistent with the private sector forecasters making the same sorts of systematic errors. So for me, Occam’s razor points to an honest mistake being the most likely explanation for the repeated undershoot of inflation. I don’t need the three assumptions (above) that the Fed critics need for their theory.

I’ve made similar arguments over the past year or two, and also suggested that I was looking for the Fed to do a better job in the future. Despite the slightly above 2% inflation last year, I don’t believe the problem has been solved, indeed I expect inflation to again fall below 2% in 2019.

BTW, the TIPS markets have been more skeptical of the claim that 2% inflation was on the way, and the TIPS markets have thus been more accurate than either the Fed or private sector economists.

READER COMMENTS

Grant Gould

Apr 24 2019 at 3:32pm

When I had an economics course in high school in 1993, the teacher told us all that the Philips curve was an old idea that people used to believe in decades ago but nobody took seriously any more, like the heliocentric universe or phlogiston.

I know now that wasn’t actually a correct description of the field, but it’s nonetheless given me some default skepticism (and confusion) the more Fed commentary and criticism I hear.

Matthew Waters

Apr 24 2019 at 3:46pm

IMO, there is a complex relationship between the natural interest rate and the Fed’s inflation performance. When the natural rate is higher, the Fed receives less lobbying and pressure to raise rates.

2013-2016 corresponded to the Fed raising short-term rates up to “normal” levels. Now that rates are at “normal” levels, the Fed looks more like an actual symmetric target. The pre-2008 Fed also looked more like a symmetrical target.

The lobbying pressure to raise rates from low levels happens across economies. 1990s BOJ, ECB and Sweden all raised rates too soon. In general, banks will always have tremendous lobbying power and banks will also not pass along rate increases at lower rates. Central banks should recognize an inherent bias towards tight policy at lower rates and counteract it *now*, before natural rates go low again. Explicit level targeting, at least at low inflation, is the best solution.

Thaomas

Apr 24 2019 at 7:22pm

If the Fed had a symmetric target then after n quarters of undershooting the target they would start overshooting it and explaining to people why they were overshooting.

My theory is that the Fed really really hates to raise ST interest rates rapidly (because banks really really hate to see ST rates rise rapidly) and knows that PL targeting, and a symmetric inflation target implies PL targeting, probably means more volatile ST rates. (I believe that the failure to drop ST rates to zero in Sept 2008 WAS just a mistake.)

Benjamin Cole

Apr 24 2019 at 7:43pm

In an odd way, Scott Sumner may be correct on this one.

After all, the largest graven-image boogeyman in the Temple of Macroeconomics is the Inflation Totem.

Practitioners of the macroeconomic arts and faiths often ominously predict the Boogeyman is returning and bigger than ever.

So the Fed and the private-sector have often overestimated, but earnestly, the future rate of inflation.

The 2% inflation target has been enshrined and worshipped now for a long time, so bumping the inflatiom target up to, say, 2.5% might be considered sacrilege. But it might be worth a try.

bill

Apr 24 2019 at 8:15pm

You make a great case. You persuaded me.

Check out this article on Bernanke.

https://www.cnbc.com/id/100496086

One sentence: Bernanke noted that inflation, one of the risks most often cited by critics of the central bank’s so-called quantitative easing, remains projected to stay at or below the Fed’s 2 percent target for the foreseeable future.

Rajat

Apr 25 2019 at 1:31am

In point 2, I believe you meant to say, “Private sector forecasters consistently overestimated inflation.”

Brian Donohue

Apr 25 2019 at 10:51am

Honest or not, it’s an error, and it’s been persistent.

If we pick up the story at the beginning of 2010, just AFTER the PCE contraction associated with The Great Recession, we see a 9-year period with cumulative annual PCE growth of just 1.5%, resulting in a cumulative undershoot of the price level of 4.7%.

So, if you took out a mortgage in 2010 that currently has a $200,000 balance, you have suffered a net loss of almost $10,000 in net worth due to the Fed’s failure to hit its target since the beginning of 2010.

Scott Sumner

Apr 25 2019 at 11:58am

Thaomas, You said:

“If the Fed had a symmetric target then after n quarters of undershooting the target they would start overshooting it and explaining to people why they were overshooting.”

That would be true if the Fed had a price level target, but it does not.

Thanks Rajat, I fixed it.

Thaomas

Apr 26 2019 at 6:24am

If the Fed never exceeds it’s “symmetric” inflation target, how can it persuade markets that it has a symmetric target? Wouldn’t NGDP be subject to the same problem if the Fed constantly undershot its NGDP rate target. Is the difference then only in the ambiguity of a “symmetric” rate vs a level target?

Scott Sumner

Apr 26 2019 at 4:41pm

Thaomas, If it never exceeded its target it could not convince the public. Of course it does occasionally exceed its target.

PJ

Apr 25 2019 at 2:18pm

Well if it was a series of mistakes, the FOMC really ought to take the data produced by the Cleveland Fed more seriously. Take the four year out inflation expectation based on treasury yields and inflation swaps. This value was below 2% in 81 of the 88 months beginning January 2012. It’s average has been 1.64%, the minimum value was 1.16%, the maximum was 2.11%.

Scott Sumner

Apr 26 2019 at 4:42pm

PJ, And private sector forecasters should also pay more attention.

Comments are closed.