In a recent piece, Financial Times columnist Rana Foroohar eulogizes the American “regulators” who are becoming a model for European ones. I put regulators in scare quotes because what we are speaking of has little if anything to do with homeostatic or cybernetic autoregulation or with general rules of law. In reality, the bureaucrats and politicians in question are coercive controllers as Ms. Foroohar admits by invoking “criminal as well as civil penalties for violators.”

Reporting of a recent American-European conference among such regulators, she writes (“America Is Toppling the EU From Its Regulatory Throne,” Financial Times, March 6, 2023):

It was the energetic crop of young American regulators who were the rock stars of the event. …

Team USA seemed to be thinking bigger and broader than its EU peers. FTC commissioner Rebecca Slaughter stressed that her agency was making policy based on how “people participate in the economy as whole people”, not just as consumers. The Justice Department officials in attendance made it clear they were going after entirely new areas. …

American regulators … view their work not in technocratic but existential terms; a battle against the risk of corporate oligopoly which threatens liberal democracy. …

Until quite recently, it was assumed that Europe would lead the way in regulating the world’s largest and most powerful corporations. That’s now shifted.

Since Ms. Foroohar column was published more than one week ago, before the demise of three American banks, the implications for banking and finance are interesting. To quote Foroohar again:

In bank regulation, too, Americans are taking a more aggressive tack than their European peers. The Fed vice-chair for bank supervision, Michael Barr … pointed out that the lack of bank failures since the pandemic began has less to do with financial institution strength than government backstopping of the economy.

We see that when the government starts “backstopping” the economy, it cannot stop front-ruling it, as it were, since it always needs further interventions to correct the consequences of its past interventions, its own mess, notably in creating moral hazard. Europeans know something about that. It is also nearly certain that the current problems of banks partly comes from the federal government’s attempts to correct in a swoop the inflation it had generated through money creation and which it denied during all of 2021. Another factor is the historical fragility of the heavily regulated American banking system, a product of two centuries of state and federal regulation. (See also a recent post of my co-blogger Scott Sumner.) So much for the government backstopping the economy.

Finally, after quoting a 1936 speech of Franklin Delano Roosevelt, Foroohar concludes:

The new and more robust American regulatory response harks back to an era when power mattered more than price and politicians weren’t afraid to take on big business.

That takes the cake! (C’est le bouquet, we would say in French.) Forward to the past!

With due respect for the respected columnist, one wonders if, despite being a mature person, she learned economics in a woke classroom. Ignoring three centuries of economics, a field of analysis that helps think about such matters, her approach is distressingly similar to current political intuitions, for mere intuitions and superstitions is what they are. Looking a bit farther in the past than the 1960s or FDR’s progressivism, one realizes that the “era where power mattered more than price” covers millennia—a few hundred thousands of them—was when ordinary people were dirt poor and at the mercy of brutal rulers or stifling customs.

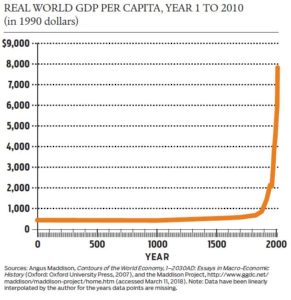

The end of this ordeal came slowly. To make a long story short, we may start with the commercial city-states of the late Middle Ages, go to banking and finance at the beginning of the modern era, and finally to the Great Enrichment that followed the Industrial Revolution (see chart below for a peek). Prices finally started start replacing power. Markets replacing the tribe or Leviathan. On this, see, among other works, the delicious short book of Nobel laureate John Hicks, A Theory of Economic History (Oxford University Press, 1969—the link is to my review of the book, a poor substitute).

READER COMMENTS

Richard W Fulmer

Mar 15 2023 at 12:52pm

Prices are information. They convey the relative values that billions of people place on tens of billions of goods and services and allow the rational and spontaneous coordination of human action across space and time. Replacing prices – replacing information – with power is a recipe for poverty. We are knowledge-based lifeforms who perform poorly in a world of disinformation.

Pierre Lemieux

Mar 15 2023 at 2:18pm

Richard: You would expect a Financial Times columnist to know that, wouldn’t you? Strange times.

Craig

Mar 15 2023 at 1:12pm

“We see that when the government starts “backstopping” the economy, it cannot stop front-ruling it”

Indeed dirigsme begets dirigsme as you might say, Professor, and as I now might add, “….and even more dirigsme”; as we now see the government backstopping (banks) the consequences of its prior backstopping (QE)

David Seltzer

Mar 15 2023 at 6:25pm

Craig, backstopping often called the Fed Put, gives self-interested bank executives the incentive to assume greater risk, as losses will be socialized. TBTF and the Peltzman Effect.

Craig

Mar 16 2023 at 11:30am

Very true, what we are seeing today might be partly the result of a moral hazard from the bailouts. This time though it does look like they are backstopping the depositors and letting the management/shareholdes take the hit.

Jose Pablo

Mar 15 2023 at 11:11pm

We see that when the government starts “backstopping” the economy, it cannot stop front-ruling it, as it were, since it always needs further interventions to correct the consequences of its past interventions,

This is so good!

And banks and the pandemic are a wonderful example:

1.- The “government backstopping of the economy” that Foroohar mentions, causes inflation

2.- To fight inflation the FED (so, the government/the “regulators”) has to raise interest rates, fast and furiously

3.- The increase in interest rates punches a hole in banks balance sheet thru the repricing of government bonds. An asset that regulation encourages them to hold after the Great Recession because they were safe, or, at least, apparently safe due to “hide losses until they naturally disspear” accounting rules enhaced by … “regulators”.

4.- The “regulators” have to act to shore up the bank crisis they have sparked with the “government backstopping of the economy” and help to hide with their accounting rules

[And it is not only, obviously, the US. The Bank of Englad was forced also to intervene to shore up the highly regulated and extrictly supervised (by “regulators”) English pension funds]

I want to be a “regulator” when I grow up: it has to be very nice being rigth even when you are so wrong

Craig

Mar 16 2023 at 11:32am

I have also noted how quickly the left is to pounce to lay blame at deregulation.

Comments are closed.