In a recent post I raised two objections to the MMT description of “net saving”, which is the following for a closed economy:

(GNP – C – T) – I ≡ (G – T)

This equation basically says that the government budget deficit equals the government budget deficit. But on the left side of the equation the budget deficit is redefined as “net saving”.

Let me try to present a case in favor of this approach, before criticizing it. Suppose I said total wealth minus non-monetary wealth equals the money supply:

Wt – Wnm ≡ M

Obviously, the left side of the equation is also the money stock, but does describing it this way help? You could argue that this identity shows that a rush for liquidity at a given income level (i.e. a desire to hold more of one’s wealth in the form of money), is potentially destabilizing. If there is an increased demand for money, then the government should boost the money supply (right side of the equation) to prevent the identity from being maintained by a fall in national income. When there’s a rush for liquidity, printing more money would meet the extra demand for money at full employment.

As far as I can tell from the commenters, MMTers are making a sort of analogous claim for the budget deficit. Thus, if at current interest rates and the full employment level of GDP there is more desire to (privately) save than to invest, then the government should accommodate that increased desire to save by running a budget deficit, which represents negative saving for the government sector.

Lurking in the background is the simple Keynesian cross model, with no role for monetary policy. (The “paradox of thrift” is another way of describing this concept.) This model is sometimes called “vulgar Keynesianism”, because it is considered less sophisticated than New Keynesian (IS-LM) models where monetary policy determines national income at positive interest rates, and fiscal policy is only needed at the zero lower bound for interest rates.

If I’m correct in my interpretation, then I still have the same two complaints about the model:

1. It’s confusing to students to call the left side of the equation “net saving”. Some other term should be used.

2. I don’t believe the identity is useful, because the underlying model that it’s being used to illustrate is wrong. I’ll illustrate this objection by discussing recent trends in the US budget deficit.

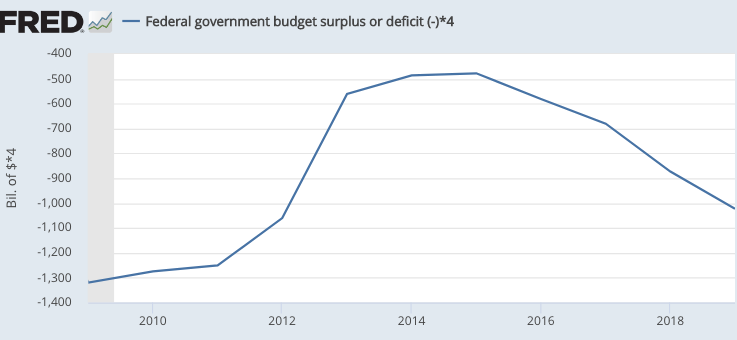

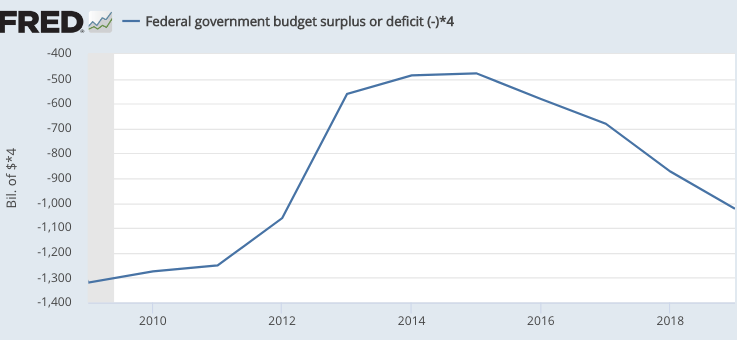

Everyone agrees that the 2020 spike in the budget deficit is a response to Covid, but there are other recent changes in the deficit that seem more “exogenous” in some sense. For instance, in calendar 2013 the deficit plunged from $1,060 billion to $560 billion, reflecting the desire for austerity among Republican members of Congress. After staying low for a few years, the deficit soared to more than a trillion dollars between 2016 and 2019, despite a booming economy. This reflected both increased spending and the Trump tax cuts.

Neither change was in response to a public “wanting” more or less “net saving”. Neither change was aimed at stabilizing aggregate demand. Instead, both changes reflected the political situation. In the Keynesian model, the 2013 austerity should have had a contractionary effect, but it did not due to offsetting monetary stimulus. The more recent increase in the deficit might have had a mild expansionary effect, but the Fed tried to offset that effect by raising interest rates multiple times. At the very least, this offsetting action by the Fed prevented inflation from rising to even their 2% target in 2019.

I can’t imagine how it could be useful to consider these fiscal policy changes from the perspective of how much net saving the public “wants” to do. Congress acts, interest rates move, and the public willingly buys up the newly issued Treasury debt at the new interest rate. The same thing occurs when IBM issues bonds. If the fiscal policy is seen (correctly or not) as threatening to destabilize the economy, as in 2013 and 2017-18, then the Fed acts to offset the effect. Keynesian economists predicted a slowdown when austerity was announced in late 2012, but by the fourth quarter of 2013 the year-over-year growth rate was considerably higher than 12 months earlier.

The budget deficit is one among many factors that the Fed needs to offset when targeting inflation at 2%, much like housing, exports, business investment, and other volatile sectors that might impact aggregate demand. If the budget deficit did determine aggregate demand, then we would have given Congress the duty to target inflation at 2%. Thank God we did not! As the 2013 and 2019 examples demonstrate, our fiscal policy is recklessly procyclical, and if Congress were determining inflation then we’d be back in the 1970s (or 1917-51) with inflation rates gyrating wildly up and down.

And it’s not just the US; other developed countries also give their central banks the responsibility for targeting inflation. There is no plausible alternative. A model that suggests that the budget deficit determines aggregate demand, even at positive interest rates, is simply wrong.

READER COMMENTS

Thomas Hutcheson

Nov 25 2020 at 1:06pm

“Thus, if at current interest rates and the full employment level of GDP there is more desire to (privately) save than to invest, then the government should accommodate that increased desire to save by running a budget deficit, which represents negative saving for the government sector.”

Presumably if this condition comes to exist from a previous condition of equality between the desired savings and investment, then it would manifest itself in unemployed resources (the marginal cost or re-employing the resource is less than its market price) and real interest rate will fall. In this circumstance, the number and aggregate value of public sector activities with positive NPV (when marginal costs not market prices of the resources employed are used in the calculation) will rise until the additional public investment eliminates the excess private saving.

This looks to me like neo-classical economics with a wealth maximizing public sector, not “Vulgar Keynesianism.” [“Vulgar” Keynesianism presumably means additional expenditures not guided by NPV maximization.] It does not even imply “no role” for monetary policy (whatever that could mean), as changes in Central Bank purchases of assets could be the vehicle by which the real interest rate falls.

Scott Sumner

Nov 26 2020 at 12:12pm

Actually, the correct response to that situation is monetary stimulus.

KevinDC

Nov 25 2020 at 2:44pm

Scott (or anyone else in the comments), do you know what MMT proponents were predicting would happen in late 2012? To be clear, I’m not asking how, looking back, they would explain what happened in a way consistent with their current model. I’m wondering what they were predicting would happen, in advance, on the basis of their model at that time the austerity was first announced. I’m curious if their model allowed them to predict the results as accurately as you did, or if they were as wrong in their prediction as the standard Keynesian model was.

Mark Brady

Nov 25 2020 at 4:00pm

If it’s a closed economy, it isn’t GNP, it’s GDP. Should I read further?

Scott Sumner

Nov 26 2020 at 12:13pm

What is “it”?

Mark Brady

Nov 26 2020 at 4:27pm

If an economy is a closed economy, we are surely discussing GDP, not GNP. Would you agree?

Scott Sumner

Nov 27 2020 at 1:26pm

No, I don’t agree. Why do you say that?

Ahmed Fares

Nov 25 2020 at 4:40pm

Dr. Sumner,

Quoting “heteconomist” (Dr. Peter Cooper):

“Macroeconomists often start their analysis from an accounting identity or set of identities. Since identities are true by definition, they can provide a good framework for analysis, including a way to detect any errors in logic or inconsistent conclusions. A theory that conforms to an identity is not necessarily correct but is at least potentially correct. To constitute a theory, though, it is necessary to do more than just invoke identities. This is because identities in themselves tell us nothing about causation.

Once we begin to make behavioral assumptions, the ground becomes contestable. Identities are incontestable, at least if we accept the principles of double-entry book keeping, whereas behavioral assumptions are not.”

From the same article:

“Broadly speaking, in MMT it is usually argued that once the government has formulated its fiscal policy settings, the behavior of non-government (which includes both the domestic private sector and the external sector) will determine the ultimate size of the government deficit (or surplus) through its behavior. In particular, tax revenues will rise and fall endogenously with oscillations in non-government activity. It is further held that if the government’s fiscal settings are not consistent with non-government achieving its intended net saving position at full employment, there will be either unemployment or inflation. Fundamental to this position is that there is no mechanism in a market economy capable of automatically generating full employment, and so in such cases it is up to government to adjust its fiscal settings to provide a better fit with non-government behavior.”

source: http://heteconomist.com/sectoral-balances-and-keynesian-causation/

My comment here, using sectoral balances:

(G – T) = (S – I) + (X – M)

My understanding is that it is typically the right-side of the equation that drives the left-side of the equation, i.e., the direction of the causation as regards net saving. The example you give of government spending in response to Covid is causation coming from the left-side of the equation.

In other words, net saving desires by the non-government sector increases net saving, but government spending can increase net saving, even if it is not desired. We see the latter with the current high saving rate. Every dollar of government spending must end up as a dollar of non-government net saving, until it drains away in taxation with each cycle of spending.

Scott Sumner

Nov 26 2020 at 12:17pm

I think you missed the point. The 2010s show that the government can adjust the budget balance in a way that is not in response to changing preferences of the public to save and invest, without destabilizing the economy. All you need is monetary offset. The MMT model rejects monetary offset, which is why it is wrong.

Ahmed Fares

Nov 25 2020 at 4:42pm

Correction:

That sectoral balances equation should be:

(G – T) = (S – I) + (M – X)

Jerry Brown

Nov 25 2020 at 10:47pm

What model says “the budget deficit determines aggregate demand” ?

MMT does not say that the budget deficit ‘determines’ aggregate demand as far as I know. MMT says that government spending could compensate for reductions in private sector demand that leaves real resources idle. But it is first the private sector that determines what it wants to do as far as spending- and then government policy needs to react to that.

Scott Sumner

Nov 26 2020 at 12:20pm

I meant determine in the sense of both policy successes and errors of omission. Yes, I understand that in the MMT model there are often shocks that originate in the private sector, but in that case MMTers argue the budget deficit should change to offset those shocks. MMTers believe the deficit should determine AD.

I don’t think we disagree; it’s just that my word choice was perhaps a bit vague.

Scott Sumner

Nov 26 2020 at 12:22pm

Here’s an analogy. I often argue that monetary policy determines NGDP. I don’t mean that velocity never changes; I mean that the Fed can and should offset those changes. If it doesn’t, then it is to blame.

Jerry Brown

Nov 26 2020 at 2:05pm

Yes, you sure do argue that consistently 🙂 I see the analogy when you put it that way. Thanks

Comments are closed.