[I wrote this last weekend, but Jason Furman beat me to it.]

It’s not just the US that has high inflation; consumer price inflation in Europe is running far above the ECB’s 2% target. Does this mean the Eurozone economy is also overheating? I doubt it, although Eurozone data is so confusing that it’s hard to be certain.

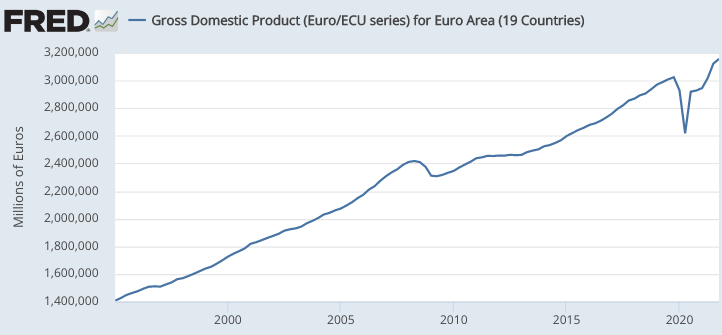

I like to begin with NGDP data. The FRED database has Eurozone NGDP data, but only up to the 4th quarter of 2021. I went to Eurostat to find out what’s causing the delay, and discovered that 2022:Q1 NGDP data is available for 18 of the 19 Eurozone members. What’s holding things up? You guessed it—Greece, a country that never should have been allowed into the Eurozone. For what it’s worth, the performance of Eurozone NGDP up until late 2021 looks almost perfect—right back on trend:

Between 2019:Q4 and 2021:Q4, Eurozone NGDP growth averaged about 2.2%, with 2.1% inflation and 0.1% RGDP growth. So what’s all this we hear about high Eurozone inflation? At first I thought that perhaps their GDP deflator was rising much more slowly than their CPI. Not really. CPI inflation ran at 2.25% from November 2019 to November 2021. The actual problem is the disgraceful delay in reporting the NGDP data. Eurozone CPI data is available monthly, and their CPI has risen by 5 percentage points in just the 5 months since November 2021. So the high Eurozone inflation that we read about is mostly due to very recent price increases, presumably associated with the Ukraine War and perhaps other factors such as Covid in China. (Ukraine affects Europe more than it affects the US.)

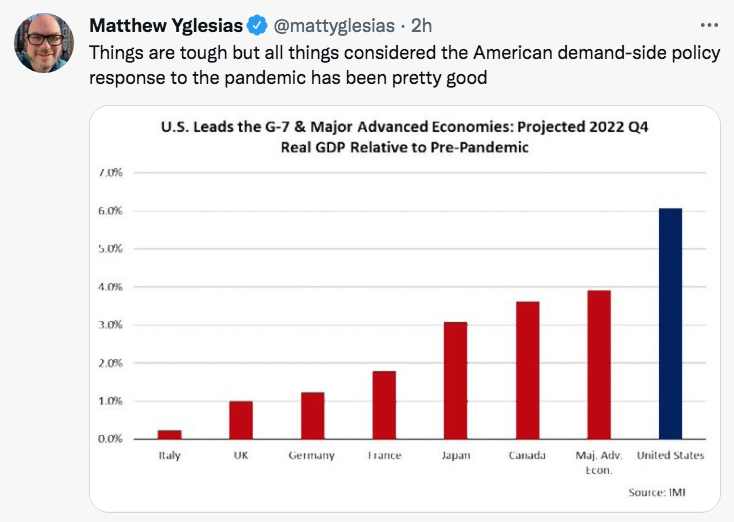

Matt Yglesias has a tweet suggesting that aggregate demand growth in the US is better than in Europe:

I’d say the growth in AD has been stronger in the US, but the growth in AD has been better in Europe—indeed near perfect. US spending growth has been too strong. This claim might seem counterintuitive given that our economy is doing better than the Eurozone economy. But our relative strength all comes from the supply side, where we significantly outperform Europe. Under Bernanke, the US did a much better job of controlling AD than did the Eurozone, but in recent years the ECB has greatly outclassed the Fed.

Europe has much higher unemployment than the US, but the Eurozone unemployment rate has actually fallen to well below its pre-Covid levels, indeed to record lows. In contrast, the US unemployment rate has merely fallen back to pre-Covid levels. There’s plenty of demand in Europe, but not excessive demand.

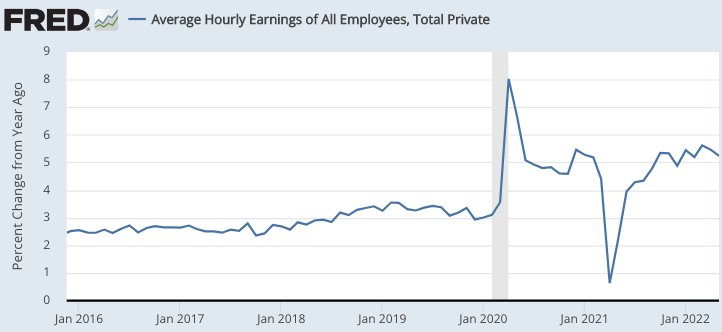

To further assure that the Eurozone is not suffering from any excessive demand-side inflation, I decided to confirm the NGDP data by looking at nominal wage growth (from Trading Economics). Once again, there is no evidence of overheating in the Eurozone:

The 2020:Q2 wage spike presumably represents a labor force composition issue, as low wage service workers disproportionately lost jobs. A year later that unwound and ever since then nominal wages have been well behaved. In contrast, US nominal wage growth has accelerated to levels incChristonsistent with 2% inflation:

To summarize, if you just look at headline inflation then the Eurozone looks almost as bad as the US. But on closer inspection, the US inflation problem has major contributions from both supply bottlenecks and excess demand, whereas in the Eurozone the inflation problem is almost entirely supply-side. The ECB seems to be doing a great job. Keep up the good work Christine Lagarde!

PS. Like me, she’s 66-years old and is much taller than average.

PPS. Steve Hanke and John Greenwood pointed out in the WSJ that not all countries suffer from high inflation:

We don’t have a global inflation problem. Inflations are always and everywhere a monetary phenomenon spawned by the creation of excess money by local central banks. China, Japan and Switzerland also face elevated oil prices, supply-chain problems and fallout from the war in Ukraine, but their annual inflation rates are 2.1%, 2.5% and 2.5%, respectively. They have avoided the ravages of inflation because their central banks haven’t produced excessive quantities of money.

READER COMMENTS

Thomas Lee Hutcheson

Jun 8 2022 at 7:18am

I am unclear on how to distinguish “demand side” inflation from “supply side” inflation. *I* might think that supply side inflation is the amount needed to maximize long run real income (“full employment”) given supply shocks (that require changes in relative prices) and some rigidly downward prices and the additional difficulty in predicting future relative prices when inflation is high. But how does SS do it?

Scott Sumner

Jun 8 2022 at 12:11pm

I use NGDP growth as my benchmark; I explained it all in my previous post.

Kailer

Jun 8 2022 at 2:46pm

“I explained it all in my previous post” and roughly 4,328 other posts going back to 2009!

This episode has helped to separate inflation doves/hawks from people who know what their talking about. Not many correctly assessed demand too weak in the GR and too strong post COVID. Those are the people to trust on monetary policy. Your posts taught me a lot over the years, thanks Scott.

Doesn’t mean you’re not still wrong about the lab leak 😉

Thomas Lee Hutcheson

Jun 9 2022 at 7:07am

Sorry, I still do not quite get it. So we take 1+ the real growth during the time is question and divide into 1+target NGDP as 1+ the “supply side” inflation and the additional inflation needed to get to actual NGDP as “excess?.” Or to simplify 1+ excess inflation = 1+actual GDP growth/1+ target NGDP growth. And the target NGDP is what the target ought to have been?

Scott Sumner

Jun 9 2022 at 2:12pm

Demand-side inflation is inflation caused by NGDP being above target.

derek

Jun 9 2022 at 2:33pm

Is there a wordy version of this answer somewhere? It seems weird to think that if real economic activity stays flat but some external shock pushes prices up 6% (so NGDP goes up 2% above a 4% target), to say that one-third of the inflation is from “excessive demand.” Maybe the Fed should indeed raise interest rates so that real activity goes down and NGDP stays on its target track, but the exogenous issue is still the external supply shock. “Excessive demand” seems like it is meant to convey a diagnosis of incorrect Fed policy, but it kind of reads as a diagnosis of political policy (e.g., how much of the inflation is due to stimulus checks, etc.).

Walter

Jun 8 2022 at 4:05pm

Any thoughts on the UK? Inflation here is even higher than the US, I believe.

Scott Sumner

Jun 9 2022 at 2:11pm

What’s the UK’s NGDP growth rate over the past 2 1/4 years?

William Peden

Jun 11 2022 at 6:43am

Scott,

Just under 5% since the beginning of 2020:https://fred.stlouisfed.org/graph/?g=QrBT

That’s above the ~4% average in the 2010s. Furthermore, part of the current inflation in the UK is that the increase in NGDP all took place in the past 12 months (11% growth from Q1 2021 to Q2 2022). Since the SRAS curve isn’t flat, especially under pandemic/post-pandemic conditions, you’d expect such a rapid increase in demand to result in a temporary inflation spike.

Personally, I expect UK inflation to be elevated for a while, but (like the US and Eurozone) I am no longer worried about runaway inflation. In fact, the danger now is that central banks will reverse course too quickly, leading to an unnecessarily deep recession, and potentially an inflationary reaction in the opposite direction. This has been the pattern of the Fed through most of its post-Gold Standard history, except the Great Moderation and the underrated Second Great Moderation of the 2010s.

Scott Sumner

Jun 13 2022 at 1:20am

Given those figures, I’d say the UK situation is similar to the US, both supply and demand side inflation.

William Peden

Jun 13 2022 at 5:53am

Yes, I agree. Not quite the 1970s redux, but some interesting parallels.

Arqiduka

Jun 9 2022 at 5:29am

If the ECB has been doing their job (well, not really, given that their job is inflation control, not spending control, but anyway), and inflation is what it is in the Eurozone, it must mean that the real standard of life in the eurozone must have cratered in the last five months or so. Just at the same time when a demand-driven inflationary episode grips the US and Australia. What a coincidence.

Scott Sumner

Jun 9 2022 at 2:13pm

That’s right. It’s actually pretty common throughout history for multiple problems to occur at once. We also saw that in the 1970s.

MarkLouis

Jun 9 2022 at 12:00pm

Doesn’t the ECB essentially have a single mandate around price stability? Should we really be cheering non-elected officials re-writing laws?

Scott Sumner

Jun 9 2022 at 2:16pm

It has a 2% inflation target. Like the US, it views that as a long run target, and allows short run deviations during supply shocks.

MarkLouis

Jun 10 2022 at 10:45am

What gives you the sense they have any intention of correcting this overshoot to get back on the 2% price level path. ECB simply ignoring its mandate in order to not have to do anything “extreme” seems more likely.

QW

Jun 22 2022 at 6:37am

MarkLouis, the ECB’s mandate is just “price stability” which should be vague enough that it can say it hasn’t ignored it. The more precise 2% inflation target is a self-defined target; it’s something the ECB itself has decided on. The EU treaties don’t define a precise target like that but only the vaguer “price stability”.

dlr

Jun 9 2022 at 3:22pm

scott, i have sympathy for your case, but…if europe is all supply side why are german and italian 5 yr breakevens the same as the US @ ~3.1%?

Comments are closed.