Supply

Definitions and Basics

Supply, from the Concise Encyclopedia of Economics

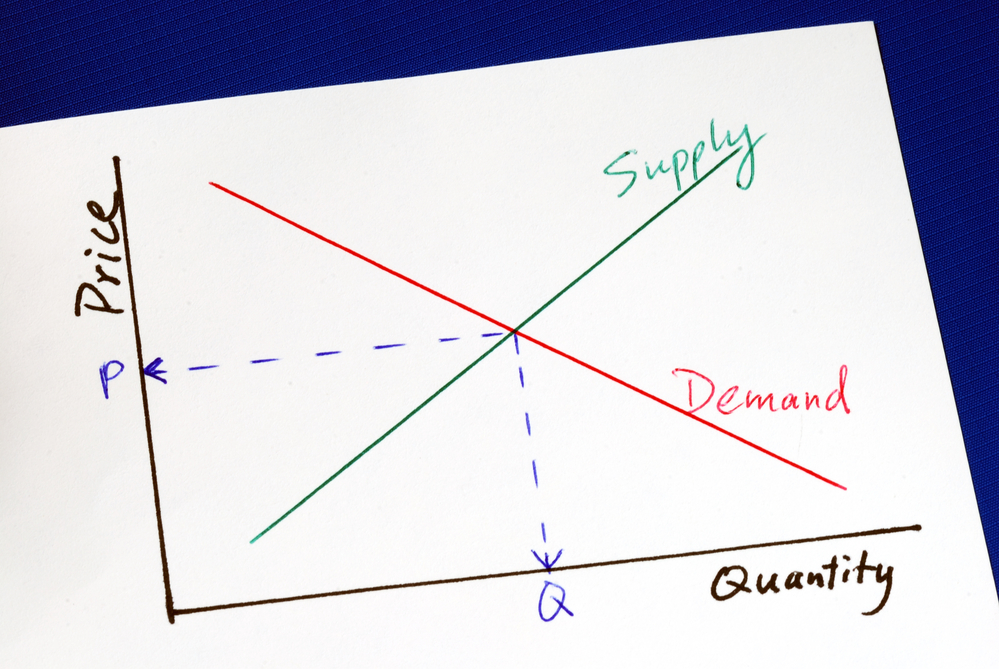

The most basic laws in economics are those of supply and demand. Indeed, almost every economic event or phenomenon is the product of the interaction of these two laws. The law of supply states that the quantity of a good supplied (that is, the amount that owners or producers offer for sale) rises as the market price rises, and falls as the price falls. Conversely, the law of demand says that the quantity of a good demanded falls as the price rises, and vice versa. (For reasons unknown, economists do not really have a “law” of supply, though they talk and write as though they did.)…

Economists often talk of supply “curves” and demand “curves.” A demand curve traces the quantity of a good that consumers will buy at various prices. As the price rises, the number of units demanded declines. That is because everyone’s resources are finite; as the price of one good rises, consumers buy less of that and more of other goods that now are relatively cheaper. Similarly, a supply curve traces the quantity of a good that sellers will produce at various prices. As the price falls, so does the number of units supplied….

The Supply Curve, at Marginal Revolution University

Law of Supply, at Khan Academy.

In the News and Examples

Trey Malone and Jayson L. Lusk, No Yolk: Shortages and Spikes in the Time of COVID, Econlib May 2021.

From February to April 2020, the price of a dozen Grade A eggs at the grocery store jumped 60%. A year later, pandemic disruptions have not subsided. As of mid-March 2021, Americans were still spending 15% more on food through grocery outlets and 14% less on restaurants and hotels than they were in January 2020. A common conclusion is that America’s food supply chain is “broken” and in need of radical restructuring to become resilient. This view is almost completely at odds with the facts and misunderstands the nature of the disruptions and the speed at which the food system responded.

Russ Roberts, Where Do Prices Come From? Econlib, June 2007.

Why are convertibles more expensive than non-convertibles? Why is scotch that’s been aged for 21 years more expensive than scotch that’s been aged 10? Why are red peppers more expensive than green peppers? Why do Wal-Mart employees earn less than the average worker in the United States? Why is gasoline more expensive in the summer than the winter? Why is gasoline more expensive in Europe than in the United States? Why are roses more expensive on February 14? Why isn’t beer more expensive on Super Bowl Sunday?

A Little History: Primary Sources and References

Alfred Marshall, from the Concise Encyclopedia of Economics

In his most important book, Principles of Economics, Marshall emphasized that the price and output of a good are determined by both supply and demand: the two curves are like scissor blades that intersect at equilibrium. Modern economists trying to understand why the price of a good changes still start by looking for factors that may have shifted demand or supply, an approach they owe to Marshall.

George Stigler, from the Concise Encyclopedia of Economics

Take, for example, Stigler’s “A Note on Block Booking.” Block booking of movies was the offer of a fixed package of movies to an exhibitor; the exhibitor could not pick and choose among the movies in the package. The Supreme Court banned the practice on the grounds that the movie companies were compounding a monopoly by using the popularity of the winning movies to compel exhibitors to purchase the losers….

But why did block booking exist? Stigler’s explanation was that if exhibitors valued films differently from one another, the distributor could collect more by “bundling” the movies. Stigler gave an example in which exhibitor A is willing to pay $8,000 for movie X and $2,500 for Y, and B is willing to pay $7,000 for X and $3,000 for Y. If the distributor charges a single price for each movie, his profit-maximizing price is $7,000 for X and $2,500 for Y. The distributor will then collect $9,500 each from A and B, for a total of $19,000. But with block booking the seller can charge $10,000 (A and B each value the two movies combined at $10,000 or more) for the bundle and make $20,000. Stigler then went on to suggest some empirical tests of his argument and actually did one, showing that customers’ relative tastes for movies, as measured by box office receipts, did differ from city to city….

For his earlier work on industrial organization and his work on the effects and causes of regulation, Stigler was awarded the 1982 Nobel Prize for economics….

Advanced Resources

Demand, Supply and the Market, lesson plan from the Foundation for Teaching Economics.

This lesson focuses on suppliers and demanders, the participants in markets; how their behavior changes in response to incentives; and how their interaction generates the prices that allocate resources in the economy. Learning about the reaction of demanders and suppliers to price, and the impact of non-price conditions (the determinants of demand and supply) creates a foundation for understanding the dynamism of markets.

The Supply and Demand of Toy Fads, lesson plan from EconEdLink.

In this economics lesson, students will examine the market responses to two different toys.

Charles L. Hooper and David R. Henderson, A Cure for Our Health Care Ills: The Supply Side, Econlib October 2018.

In a free market, if one person desires another’s services and the two parties reach mutually agreeable terms, they make an exchange. That’s not the system we have in medicine, as willing providers are often not allowed to sell to willing buyers. The outward rationale for governmental and quasi-governmental control of physicians’ services is consumers’ supposed incompetence: how can we know what good care is? The result is reduced competition, which leads to higher prices for doctors’ services.