In 1936, John Maynard Keynes came up with a macro model that was a product of its time. That’s the wrong way to do macro. Models should be based on the empirical facts of all countries and all time periods.

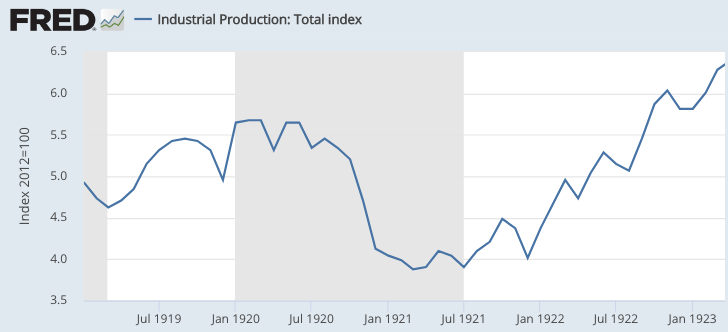

If your macro model cannot explain why the US experienced a major deflation (with NGDP falling nearly 30%) from mid-1920 to mid-1921, the model is useless. If it cannot explain why industrial production suddenly fell by 30% after mid-1920, the model is useless. If your model cannot explain why the 1921 depression was followed by a very quick recovery, whereas the 1929-33 depression was followed by a long 8-year recovery, the model is useless. You need a truly “General Theory”, applicable to all times and all places.

Unfortunately, most macro models cannot explain these important facts, and many others.

My previous post on the US and Hong Kong Phillips Curves got some positive feedback:

Brian Donohue

Jun 21 2019 at 4:45pm

Very clever.ChrisA

Jun 22 2019 at 3:49am

Agreed. With empirical data like this, who can deny the monetary framework is the right way to do macro-economics. The theory is sound but that doesn’t always transfer into empirics.

When I wrote the post I overlooked this point. It seems obvious to me that macro models must be monetary models. But lots of people disagree. So Chris is right, it does constitute a powerful argument for the monetary approach to macro, which many people still do not accept. What other explanation is there for the difference between the US and Hong Kong Phillips curves? Surely there is no alternative explanation as simple and elegant.

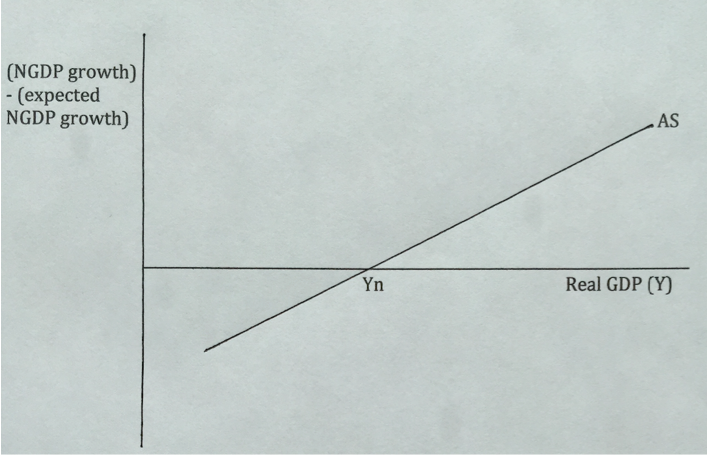

Think of the following two-part model:

NGDP = M*V(i, bank failures), where velocity is positively related to nominal interest rates and negatively related to risk of bank failures. (Since 2008, you need to add IOR.)

And unexpected NGDP shocks affect real output:

This is a simple but incredibly powerful framework for analyzing a wide range of macro issues. Of course it’s just a framework; we still need to model all of the factors that impact aggregate supply. But this framework can easily explain the stylized facts that I discussed above. Thus the big decline in NGDP during 1920-21 was mostly caused by a huge decline in the monetary base. Note that the monetary base does not even appear in most New Keynesian models. What is their explanation for 1920-21? The quick recovery was due to the fact that nominal hourly wages were more flexible in those days. The contraction of 1929-33 was caused by a fall in the monetary base during 1929-30, and a fall in velocity during 1930-33, caused by lower interest rates and bank failures. The slow recovery from the Great Depression was caused by the NIRA, the Wagner Act, and minimum wage laws, which sharply contracted the supply of labor, and also the contractionary monetary policy of 1937-38.

This is a simple but incredibly powerful framework for analyzing a wide range of macro issues. Of course it’s just a framework; we still need to model all of the factors that impact aggregate supply. But this framework can easily explain the stylized facts that I discussed above. Thus the big decline in NGDP during 1920-21 was mostly caused by a huge decline in the monetary base. Note that the monetary base does not even appear in most New Keynesian models. What is their explanation for 1920-21? The quick recovery was due to the fact that nominal hourly wages were more flexible in those days. The contraction of 1929-33 was caused by a fall in the monetary base during 1929-30, and a fall in velocity during 1930-33, caused by lower interest rates and bank failures. The slow recovery from the Great Depression was caused by the NIRA, the Wagner Act, and minimum wage laws, which sharply contracted the supply of labor, and also the contractionary monetary policy of 1937-38.

The framework also applies to modern times. The deep recessions of 1982 and 2009 were caused by NGDP growth falling far below expectations, due to tight money policies.

READER COMMENTS

Steve Fritzinger

Jun 22 2019 at 5:40pm

Keynes entered the UK Civil Service in 1906. He was at the very start of his career and that was the last time he saw a normal economy.

After that he lived through the run-up to WW I, the inter-war period and (most of) WW II.

He correctly predicted what punitive damages against Germany would do.

He was like a brilliant physician who never saw a healthy patient.

Scott Sumner

Jun 22 2019 at 6:21pm

Steve, Good point.

Benjamin Cole

Jun 22 2019 at 7:54pm

All true, but do not be too impressed with any single explanation of what brings about economic prosperity.

Hong Kong is a good example in point. People in Hong Kong face ferocious housing costs due to property zoning and other regulations on property development. The powerful financial community in combination with property developers works with the government of Hong Kong to very slowly redevelop parts of the enclave. The limited competition assures that all participants make money and that Hong Kong bureaucrats are influential.

The perspective that the monetary authority of Hong Kong has created an inflation in Hong Kong property, as they peg their policy to the Federal Reserve, is true in some respects but a very limited perspective in other respects.

Scott Sumner

Jun 23 2019 at 4:31pm

Not sure what point you are trying to make.

Thaomas

Jun 23 2019 at 10:05am

Notwithstanding the micro mistakes of NIRA, AAA, minimum wages/Wagner Act (important?), allowing bank failures, and the decline in the fiscal deficit in 1939, etc., why could the Fed not have adopted a “buy what it takes” policy of restoring the trend of the pre 1929 price level and full employment or trend level of NGDP have done the trick?

Scott Sumner

Jun 23 2019 at 4:32pm

Thaomas, Yes, more monetary stimulus would have helped. So would more flexible wages.

Thaomas

Jun 24 2019 at 6:05am

But the Fed moves last.

BTW I thought the recovery from the Great Depression starting about ’32 was quite fast and private investment led. Is that just semantics?

Matthias Görgens

Jun 29 2019 at 9:42am

There was some quick recovery and then another recession. Have a look at Scott’s Midas Paradox for more details on the Great Depression.

ChrisA

Jun 23 2019 at 12:41pm

Thanks for the feedback Scott.

Ben – do you really believe that Hong Kong is rich because of high house prices? Isn’t that just the wrong way round?

Hank Phillips

Jun 24 2019 at 11:03am

For a minute there I’d hoped an economist had seen reason, but no. In a mixed economy, coercion at gunpoint is the conveniently overlooked variable. On the Chart I see the effects of wartime prohibition enacted June 1919, five years after the first weaponizing of the communist income tax abruptly shut down the exchanges. This was followed by weaponized Volsteadism the night of January 16th, 1920, while These States were technically still at war with Germany, but innocent of participation in the Versailles Treaty. Farther to the right, dividends are left untaxed, providing a retirement fund for the investment of illegal income from recently banned things such as beer. Then within a single 24-hour period, Manly Sullivan’s 5th Amendment defense is annulled by the same Supreme Court that saw nothing unconstitutional in conscription and prohibition. Coinciding with that bootlegger’s tax liability the German bourse imploded, did not recover, and voters thenceforth stampeded to National Socialist Candidates. Finally Wesley Livsey Jones’ Five and Ten law made beer criminals liable to the chain gang, asset forfeiture and a fine worth about 30 pounds of gold just before Herbert Hoover took office. So, monetarist, how large a sum of money was involved in the liquor and drug market compared to, say, the Federal budget? Prohibition and The Crash were perhaps no more a coincidence in 1929 than in 1921.

Scott Sumner

Jun 24 2019 at 3:56pm

So Prohibition caused the 1921 depression and the Great Depression?

Did it also cause the roaring 20s? The Coolidge boom?

John Hall

Jun 24 2019 at 3:26pm

It seems like Real GDP should be on the y-axis of that chart instead of the x-axis. Economists always have drawn their charts funky…

Scott Sumner

Jun 24 2019 at 3:57pm

You could argue the same for ordinary S&D diagrams. I’m following convention. It would be too confusing if I tried to reform all of macro and all of micro in one diagram.

Robert Simmons

Jun 25 2019 at 2:01pm

If your macro model cannot explain why the US experienced a major deflation (with NGDP falling nearly 30%) from mid-1920 to mid-1921, the model is useless. If it cannot explain why industrial production suddenly fell by 30% after mid-1920, the model is useless. If your model cannot explain why the 1921 depression was followed by a very quick recovery, whereas the 1929-33 depression was followed by a long 8-year recovery, the model is useless. You need a truly “General Theory”, applicable to all times and all places.

Does this apply to other fields of study, like physics? So Newtonian gravity is useless because it’s only approximately correct under certain circumstances?

Scott Sumner

Jun 27 2019 at 1:27am

Robert, That’s not a good analogy, as my examples are some the the simplest, least difficult problems in macro.

Matthias Görgens

Jun 29 2019 at 9:44am

Modern versions of Newton’s classic theory come with an understanding of when it’s applicable.

Comments are closed.