When I studied history, I was perplexed as to how the US could have done things like the internment of Japanese-Americans in WWII or the Joe McCarthy witch hunts of the early 1950s. Today, as I observe the growing anti-Chinese hysteria, these events are becoming easier to understand.

When I studied economic history, I was perplexed as to why economists of that period were blind to the costs of an extremely tight monetary policy that drove NGDP sharply lower during the early 1930s. Today, having seen a similar blindness in regard to the Great Recession, I’m no longer so perplexed.

The Economist has a very good (but also very depressing) article discussing how the field of macroeconomics has changed during the past decade. I take no pleasure in being right 10 years ago when I warned that misdiagnosis of the Great Recession could lead to the same sort of “dark ages” of economics as developed during the 1930s (and we escaped from in the latter 20th century).

Kevin Erdmann recently wrote a book pushing back against many of the myths regarding the housing bubble and bust, and I have a book coming out next April (University of Chicago Press) on market monetarism and the Great Recession. Until then, you might be interested in our joint Mercatus working paper, which presents some of the key ideas in both books.

PS. The Economist article is excellent, but does have one mistake:

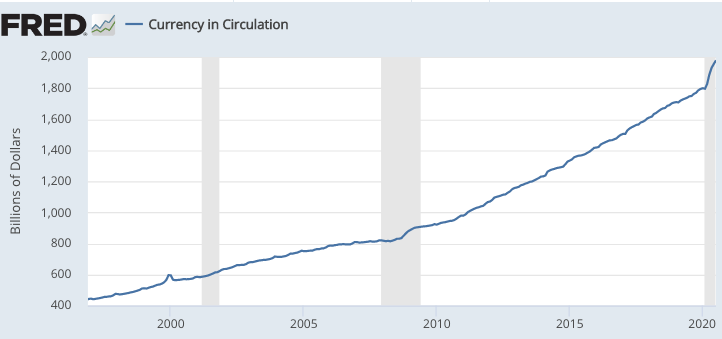

Several factors might yet make the economy more hospitable to negative rates, however. Cash is in decline—another trend the pandemic has accelerated.

Actually, use of cash (mostly as a store of value) has increased sharply under Covid-19. That makes the economy slightly less hospitable to negative rates. Cash is a substitute for negative rate bank deposits.

READER COMMENTS

Michael Byrnes

Aug 4 2020 at 5:31pm

I have $5 in cash in my wallet that has been there since March 13,the day I started sheltering in place. I’ve been to stores plenty of times since then and I walk by an ATM at least once every day. But still have just $5 that is leftover from the before times.

So I’m not surprised that someone would assume cash is going out of use – I would have wrongly assumed the same.

Philo

Aug 4 2020 at 7:25pm

Out of use for transactions, but not out of use as a store of value.

Scott Sumner

Aug 4 2020 at 7:39pm

Yes, I’ve also cut back on the use of cash.

Dylan

Aug 4 2020 at 10:37pm

One of the interesting things I’ve noticed around here is the number of places that have gone from being cash only to not accepting cash at all. Lots of Venmo only bars and restaurants popping up.

Mark Brady

Aug 4 2020 at 11:25pm

“When I studied history, I was perplexed as to how the US could have done things like the internment of Japanese-Americans in WWII or the Joe McCarthy witch hunts of the early 1950s. Today, as I observe the growing anti-Chinese hysteria, these events are becoming easier to understand.”

Were you also perplexed, at least somewhat, as to how the U.S. could have dropped two atom bombs, the first on Hiroshima, the second on Nagasaki?

Matthias Görgens

Aug 5 2020 at 4:19am

I don’t think he would have to be. Doing questionable things to people in far away places was never out of fashion during Scott’s lifetime.

Scott Sumner

Aug 5 2020 at 8:10pm

It’s not so much Hiroshima that appears incomprehensible; it’s all of WWII. On my first visit to German in 1990 I couldn’t even imagine what had happened there 50 years earlier. It all seemed so “normal”.

Iskander

Aug 5 2020 at 6:18am

Monetary policy was not the only part of economics to go crazy during/after the 1930s.

Governments moved away from free trade, funneled massive amounts of money into state owned businesses, took a hostile attitude to foreign investment and jacked up the regulation of private sector activity. Yet what happened?

The post war boom led to higher living standards than ever before, despite the worse government framework. I think it shows how for GDP per capita, the growth effects of technological progress predominate the level effects of government policies.

Mark Brophy

Aug 5 2020 at 6:31pm

Governments freed more trade after the war and that has been the major reason the world has become more prosperous.

Scott Sumner

Aug 5 2020 at 8:08pm

You said:

“I think it shows how for GDP per capita, the growth effects of technological progress predominate the level effects of government policies.”

Within the policy range of the US that’s true. Not so true when you consider extremes like Venezuela.

It’s also a reason why I put more weight on cross sectional comparisons—that’s where neoliberalism really comes out ahead.

Kailer

Aug 5 2020 at 6:28pm

Fun fact. The Bank of Canada surveyed Canadians on payments used over the previous week. Perhaps not suprisingly fewer people reported using cash than debit or credit cards. What was surprising was that more people reported using e-mail transfers than using cash (barely more. Basically a tie)!

Note: In Canada you can send someone money by email, not sure if you have these in the USA.

Comments are closed.