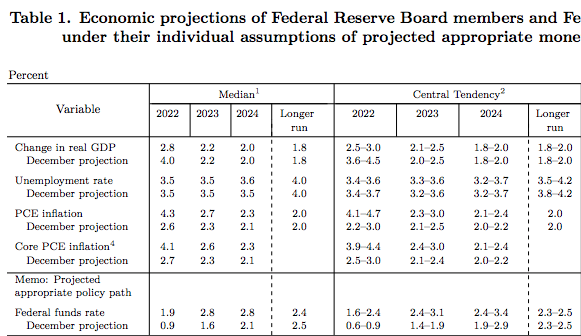

Of course they won’t admit to this fact, but these projections make a mockery of the Fed’s commitment that inflation will average 2% over the longer run:

The Fed is not supposed to raise its projection for the average inflation rate during the 2020s; it should adjust monetary policy so that its inflation forecast for the 2020s does not increase.

Some might point to the “flexible” part of “flexible average inflation targeting”, which presumably refers to the fact that the Fed doesn’t just care about inflation, they also care about real GDP growth. But the Fed just raised its implicit estimate of NGDP growth in 2022 from roughly 6.6% to over 7%, which is wildly inconsistent with the Fed’s dual mandate. NGDP is already well above the pre-Covid trend line. The economy is overheating and the Fed is about to pour more gasoline on the fire.

St Louis Fed President James Bullard is right; the Fed should have raised rates by 0.5%. But the bigger mistakes were made late last year, when the Fed allowed excessive NGDP growth and refused to commit to pushing inflation below 2% after a period of above 2% inflation.

Just as in late 2008, this is a mistake happening in broad daylight. There is no excuse.

READER COMMENTS

Michael Sandifer

Mar 16 2022 at 5:54pm

These aren’t exactly long-run projections for core PCE. In fact, the longer run forecast is blank. The NGDP projection going out to 2024 maxes out at 4.4%.

The 10 year breakeven makes your point, and this much nominal instability can make a big difference in real terms, but unless the Fed slams on the brakes, I just don’t see the danger. It’s what the markets think about the Fed’s reaction function that matters.

Scott Sumner

Mar 16 2022 at 8:02pm

The long run PCE inflation forecast is 2%, which is not consistent with AIT.

Michael Sandifer

Mar 17 2022 at 11:16pm

Scott,

Yes, it means there is no AIT, but why would an NGDPLT guy want AIT? While better than plain inflation targeting, it is nonetheless dumb. You seem to put more importance on having a specific, explicit rule, even when suboptimal, than promoting your preferred optimal policy.

Thomas Lee Hutcheson

Mar 16 2022 at 6:15pm

I agree qualitatively that the Fed should be (and should have been) “doing” more. Still the 5 year TIPS today is consistent with 9% inflation average for one year and 2.3% (equivalent of the PCE 2%) average for years 2-5. The Treasury really ought to create those intermediate TIPS so the Fed can see what the market is really thinking.

bb

Mar 16 2022 at 6:47pm

Scott,

It’s pretty clear now that they never believed in AIT. They wanted to run hot last year and decided AIT was a convenient excuse to hang their hat on. It’s all discretion all the time. And all the inflation hawks will feel vindicated for being right for all the wrong reasons. This doesn’t just harm the economy. This harms the discourse. This will make us dumber as a nation about monetary policy. So disappointing.

Scott Sumner

Mar 16 2022 at 8:04pm

I suspect Bullard believed in it, but Powell obviously did not.

I wonder what Clarida’s views were?

MarkLouis

Mar 17 2022 at 9:04am

Agree, and we should spend more time analyzing why the Fed is so comfortable abandoning a mandate. I suspect they are fearful of ever being seen as “pushing back” against government spending or asset prices.

Not sure how much of that is some version of “economics” or simply the desire to not have their names show up in mean headlines.

TravisV

Mar 16 2022 at 6:52pm

Prof. Sumner, I worship you more than almost anyone. I’m not nearly as alarmed as you are about the looming acceleration in NGDP growth, though. David Beckworth and Ryan Avent don’t seem to be nearly as alarmed either.

Here’s a brilliant post from David Glasner yesterday addressing a fellow inflation alarmist: Olivier Blanchard:

https://uneasymoney.com/2022/03/15/wherein-i-try-to-calm-professor-blanchards-nerves/

🙂

D.O.

Mar 16 2022 at 7:00pm

So it does seem that “average” in FED speak means “asymptotic”. In a sense, that’sounds right. Averaged over infinite time, asymptotic is average, but really? You know, in the long run we are all dead.

BC

Mar 16 2022 at 10:17pm

Yes, “asymptotic” (on inflation, instead of price level) seems to describe the Fed’s actual behavior. Note that asymptotic is less aggressive than even their old pre-FAIT was supposed to aim for. Under plain old (non-average) inflation targeting, the Fed was supposed to target 2% inflation each year, regardless of past inflation. But, their projections were always to approach 2% from whichever side they were already on, just like now.

The Fed seems to want to avoid “overshooting” on (instantaneous) inflation. Of course, average inflation targeting requires “overshooting” on inflation. Above-target inflation must be followed by below-target inflation. AIT doesn’t overshoot on *price level* target but, by stating projections in terms of inflation rather than price level, the Fed seems to psych itself into “asymptotic” behavior. “Overshooting” looks destabilizing. (The prefix “over-” literally means “too much”.) AIT is like a driver asymptotically approaching the center of the road (price level). But, if one looks instead at the heading of the car (inflation), then it looks like the heading is “overshooting”, zig-zagging from heading left to heading right. When the Fed projects core PCE inflation falling from 4.1% to 2.6%, it thinks it is projecting 1.5 percentage points of improvement towards its target rather than drifting another 0.6 points further away from its (price level) target, adding to the prior year’s 2.1 point error.

MarkLouis

Mar 17 2022 at 9:09am

In other words, there is no mandate.

Worse, when deflation is met with urgent and extreme moves (eg. bailouts) but inflation is met with patient and cautious moves, the system will be prone to overshoots. This is what the “hard money” crowd has always been fearful of.

Mark Brophy

Mar 16 2022 at 8:10pm

Raising the rate by 0.5% is too little, too late. They should’ve raised the rate to 5% and increased it by 1% until it reached 10% or 20% or until inflation is eliminated, as Paul Volcker did in the 1970’s. We’ll have to suffer permanently high inflation so that the federal government can repay the debt in devalued dollars.

We should accept the fact that paper money is a failed experiment, we need to return to the gold standard. The purpose of paper money is to enable the government to grow faster and bigger than it could in an honest gold money system. The bigger the government, the more money is available to politicians to buy votes and campaign contributions.

Jeff

Mar 17 2022 at 12:37am

How about a cryptocurrency that implements Friedman’s k-percent rule?

Rodrigo Escalante

Mar 16 2022 at 10:08pm

Will this be a catastrophic error like the post Lehman fed meeting? Or will this be a drag but allows the economy to truck along? You have been pretty critical of the fed which would lead me to think you believe this policy error will have deep repercussions on the economy although the market reaction was positive. Granted tomorrow could be much different but still the initial reaction was pretty good.

Market Fiscalist

Mar 16 2022 at 10:13pm

I agree that the fed seems not to be serious about AIT and that based on current NGDP trends they are allowing the economy to overheat. But given that the long run PCE inflation forecast is still only 2% (inconsistent with AIT but in-line with previous IT) I’m curious on how big a mistake you think the fed is currently making and what the consequences might be ?

MarkLouis

Mar 17 2022 at 9:12am

Why would they have any confidence at all in their ability to forecast inflation at this point? They should target TIPS spreads or inflation swaps (or set up a new, better inflation market) after having failed so badly with their own forecasting.

Further, if they want to continue to target a forecast they should explain in great detail how their approach to forecasting inflation has changed after getting the last few years so wrong.

Scott Sumner

Mar 16 2022 at 10:20pm

Rodrigo and Market, The size of the mistake is difficult to determine in real time, as monetary policy is an ongoing process. It may end up being small or large, depending on what they do next.

Market Fiscalist

Mar 16 2022 at 10:57pm

My fear (and sense) is that the fed is (for political reasons) currently making big mis-steps that will likely leads to an avoidable recession.

My question is: Why is that fear not reflected in inflation forecasts ? Do people just trust the fed more than I tend to ?

Scott Sumner

Mar 17 2022 at 1:57pm

Historically, recessions have been hard to predict. This inflation has not been going on long enough to make a big recession inevitable. The Great Inflation lasted 15 years.

They’ll have to slow the economy to bring inflation under control but how much is unclear. If they somehow get NGDP growth down to 3.5% and keep it there, we could still avoid a deep recession.

Jeff

Mar 17 2022 at 12:58am

They have been worried for years about “deflationary mindset” and they were looking for an opportunity to push a strong enough money impulse to change that. As brutal as it sounds, I think they wanted a new generation of people to experience what it feels like to see prices rapidly shoot upward. If they didn’t want this to happen they would have tapped the brakes last summer. And if they didn’t want regular people to be negatively affected, there are lots of policies they could have changed, like having Treasury raise the I-bonds limit. The reasonable conclusion is that they wanted the message to percolate through society that people should be in the habit of buying things ASAP.

bill

Mar 17 2022 at 10:58am

I would love to buy more I-bonds. Best investment I ever made was buying I-bonds in September 2001 after 9/11. The real yield on TIPS fell dramatically, but I-bond yields didn’t get reset until a few weeks later.

Phil H

Mar 17 2022 at 7:03am

I apologise for being ignorant on this point, but I can’t understand this post. The table seems to show inflation running a bit higher than 2% for the next couple of years, with one of the inflation measures still at exactly 2.0% in the “long run”. I don’t see how that’s inconsistent with targeting 2% on average. In the recent past have there not been years in which inflation was below 2%?

I understand that Sumner believes the Fed has the power to exercise very precise control over NGDP; but also that many other economists don’t believe that the Fed has that much fine control. Under *their* assumptions, wouldn’t it be reasonable to aim for inflation to trend down towards 2% over the next couple of years?

Scott Sumner

Mar 17 2022 at 2:04pm

Phil, A reasonable assumption is that FAIT began at the beginning of the 2020s. In that case, you’d want inflation to average 2% over the decade. Instead, the Fed keeps raising its estimate of inflation during the 2020s, higher and higher. That’s not how AIT is supposed to work. Even if its true that inflation should be brought down gradually, it should be brought down to below 2%, so that 2% is the average rate.

Phil H

Mar 18 2022 at 9:49pm

Thanks, that makes sense. But it does sound like it’s a bit dependent on the reference time window that you use, and also on your view of risk.

So, if I were a Fed board member, and I believed that I only have limited control over inflation and NGDP, in order to target 2%, I might very well make my long-range target always 2%. The intuition would be: there are going to be shocks along the way. But shocks can hit in both directions. There’s no need for me to try to artificially correct (overcorrect) for shocks; all I have to do is keep aiming for that long-term 2%.

This would seem especially likely given that the Fed, as I understand it, has not applied a specific time window to the average inflation policy – there is no commitment to hitting the 2% mark exactly at the end of 5 years, 10 years, or whatever. Without any kind of term within which a shock needs to be corrected for, there isn’t any necessity to build in corrective undershoot/overshoot into the planning?

(Though I recognise that this seems inconsistent with what was being said a couple of years ago, when there *was* talk of corrective overshoot following years of low inflation.)

Tacticus

Mar 17 2022 at 7:10am

It both amazes and terrifies me how many people I’ve spoken to in the last few days who are still claiming that all this inflation is just a supply shock from Covid + Ukraine and that raising rates will only hurt the economy.

Michael Rulle

Mar 17 2022 at 9:33am

True that 2.0% inflation rate is inconsistent with AIT——so he has obviously changed his view.

I just do not see why a 2% target inflation is troublesome——-would we think that had he never brought up AIT?

You are clear in your view that Fed should target NGDP. I can only assume that since they do not target NGDP, by eliminating AIT, the likelihood of achieving the desired NGDP (even as it is not targeted?) is lower without AIT.

I miss Milton Friedman.

Michael Rulle

Mar 17 2022 at 9:37am

P.S

not an insult re: Milton Friedman. I really do miss him.

Lizard Man

Mar 17 2022 at 10:26am

It seems to me that monetary policy that is too contractionary is a lot worse than monetary policy that is too expansionary, at least at the margins in which the US Fed operates. Policy that is too contractionary leads to many, many years of mass unemployment, as was seen during the Great Recession. Long periods of mass unemployment seems to hurt not only in the short run, but in the long run too, as young people, instead of learning useful skills and gaining valuable experience, sit around playing video games and work part time jobs that do not develop productive skills. Then when the economy finally recovers, all the employers want “senior” engineers, or accountants, or software developers, who simply don’t exist because so few people were hired as entry level engineers, developers, etc.

Expansionary policy doesn’t lead to a collapse in entry level hiring and future shortages of experienced, skilled workers. It just lowers wages, and it only does that if productivity growth is weak.

Scott Sumner

Mar 17 2022 at 1:59pm

I agree, for example the Great Recession was much worse. But one of the leading causes of monetary policy that is too contractionary is previous monetary policy being too expansionary. That’s why you want to avoid both.

James A

Mar 18 2022 at 3:22am

So now we will have the “soft landing” vs “hard landing” debates all over again.

At least the market is betting on a “soft landing”. Scott, trust the market!

Scott Sumner

Mar 19 2022 at 6:52pm

The market almost never predicts recessions.

James A

Mar 21 2022 at 4:51pm

A decently inverted yield curve is a good predictor, I believe. That is, current Fed rates are inappropriately high and likely to lead to much lower rates than current ones. Not the case today.

MarkLouis

Mar 17 2022 at 3:44pm

It is beyond perplexing that the Fed would adjust policy in such a way at their latest meeting that 10y inflation expectations actually rise. Yet this is exactly what happened (up 10bp since the meeting to 2.95%). I think we have to entertain the possibility that despite an army of PhD’s the Fed has essentially no idea what it’s doing.

Michael Rulle

Mar 18 2022 at 7:30am

To—Mark Louis.

I read 56 page essay yesterday—-written by Marius Gustafson in 2010 (reason.org) titled “The Hayek Rule: a New Monetary Policy for the 21st century”. It was derived from Hayek’s thoughts from the 1930s—-I am virtually positive he changed his views later in life as he lost faith in a Central Bank’s ability to to achieve targets.

What I found interesting was Gustafson said the Hayek Rule should target gross nominal income——which is the same as NGDP——-Or close enough. That is, pretty close to Scott Sumner’s view. He compared that to Friedman who targeted money supply and and John Taylor who targeted constant price levels.

I have come to believe it is not possible for even the best economists in history—-let alone readers such as ourselves —-to be persuasive enough about “best” monetary policy. For example, Taylor was a strong supporter of Greenspan until he wasn’t. Scott was a moderate supporter of Powell——-until Powell seemed to change his mind while pretending he did not.

Plus——the ability to implement any policy is extraordinarily difficult as the important variables are in constant flux.

I also wonder just how important the difference is between these various theories. Some might be better than others——-but how does “better” play itself out—-what is evidence of better?

It is easy to point out the extremes——large -deflation and large inflation——but not what would have happened had other policies been tried.

I am going to read Hayek’s later in life views on Central Banks——and see if I am intelligent enough to be persuaded.

There must also be a suboptimal policy that all can agree is suboptimal relative to their own best version ——but that might be good enough. I would like to see that policy.

MarkLouis

Mar 18 2022 at 8:38am

The Fed should follow its chosen framework most importantly. What’s ideal is irrelevant if the central bank will just scrap it when it becomes inconvenient for any reason (as we’ve just witnessed). If the Fed were to regain its credibility I’d favor NGDPLT but with of an inflation cap of 3%. I believe anything higher will result in volatile political outcomes.

Matt D

Mar 18 2022 at 6:04am

The Fed is the US Treasury’s banker. If they were to raise rates to the level needed to deal with inflation, then the US Treasury’s ability to cover the interest payments on new short term debt would become strained. The flat/inverted portion of the curve now gives the Treasury the opportunity to refinance their short term debt to lock in the lower rate. Will the US government seize this golden opportunity?

Comments are closed.