I have a new piece at The Hill, discussing the problem of unsustainable budget deficits:

Governments have little incentive to run budget surpluses and today seem to be ignoring even the more modest goal of keeping the deficit at sustainable levels.

The economics profession shoulders some of the blame for this situation. Many economists relied on dubious macroeconomic theories to advocate deficit spending during the past recession. This provided a cloak of respectability to large budget deficits.

When that sort of “fiscal stimulus” later became inappropriate — even according to the sort of Keynesian models that call for deficit spending when unemployment is high — it was difficult to get average people to understand why they should all of a sudden worry about budget deficits.

In contrast, some conservatives issued excessively alarmist warnings during earlier decades, when deficits were not at unsustainable levels:

As with the boy who cried wolf, the public is becoming numb to the constant warnings about a debt crisis.

Today, however, there really is reason to be concerned about the budget deficit.

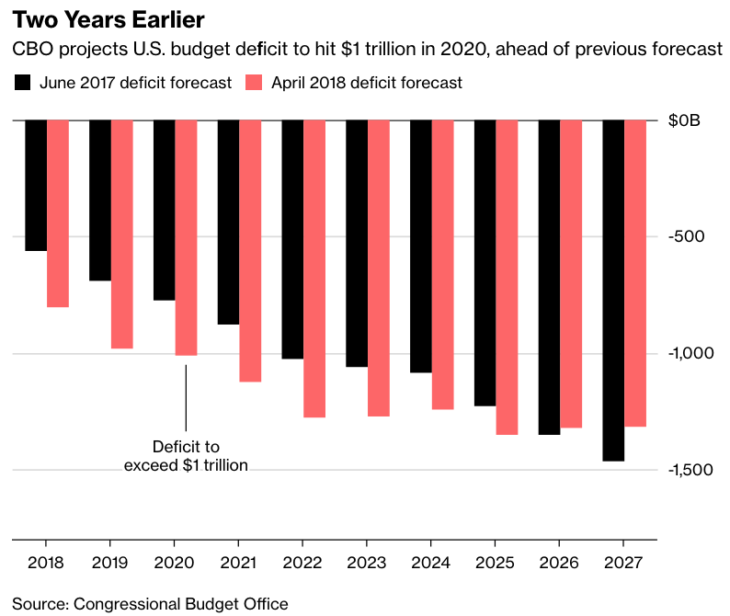

For the first time in history, America is seeing its budget deficit rise dramatically higher during a period of peace and prosperity. While there have been even bigger deficits on occasion — measured as a share of GDP— they were always associated with a temporary situation such as war or high unemployment.

Just as I try to avoid being a perma-hawk or a perma-dove on monetary policy, I try to avoid constantly warning that any budget deficit is excessive, or going to the other extreme of claiming that deficits never matter.

Notice that the recent tax cuts are not paying for themselves with faster growth (and this is the optimistic forecast, assuming no recessions):

READER COMMENTS

Brian Donohue

Dec 3 2018 at 12:27pm

“For the first time in history, America is seeing its budget deficit rise dramatically higher during a period of peace and prosperity.”

The deficit has been ballooning since FY2015. Those black lines on the graph look wrong. Deficit went from $438bn in FY2015 to $585bn in FY2016 and $666bn in FY2017 (all basically pre-Trump, and all pre-tax bill), but CBO was estimating a FY2018 deficit of just a bit more than $500bn? I call BS.

Scott Sumner

Dec 3 2018 at 1:26pm

Brian, The deficit would normally shrink during a boom. The CBO forecast presumably did not take into account the big spending increases and tax cuts under Trump. It was a “baseline” forecast.

I’m sure a market forecast would have predicted a bigger deficit, as the market would have seen the irresponsible fiscal policies that were on the way.

Brian Donohue

Dec 3 2018 at 1:55pm

“The deficit would normally shrink in a boom.”

Yes, this is why I provided data showing a 52% increase in the deficit between FY2015 and FY2017, during a boom and before Trump. That’s your baseline, but somehow CBO expected the number to shrink back to a bit over $500bn in FY2018? Gimme a break.

The tax bill doesn’t help the deficit, but the problem of ballooning deficits during a recovery predates Trump by a couple years.

Scott Sumner

Dec 3 2018 at 2:15pm

Brian, Your final sentence is true, but I think you fail to understand that the CBO is required to make predictions based on current government policy. I doubt anyone at the CBO actually expected that outcome.

robc

Dec 3 2018 at 2:36pm

When people (economists?) measure whether a tax cut pays for itself with growth, are they only looking at the just federal revenues or even just the tax in question?

It seems to me, and I have no data to back this up, that even if the the income tax revenue only “pays back” 50% of the tax cut, that the increase in state income tax revenue and state and local sales tax revenue and property tax revenue and FICA revenue might more than “pay back” the other 50%.

So the Feds could come out negative on the deal, but the states and local governments are rolling in extra money. But the net government revenue is positive.

Brian Donohue

Dec 3 2018 at 3:18pm

Scott,

You provided a graph to show the impact of the tax law. The reader is invited to assume that the law produced an increase in the deficit in FY2018 of something like $300 billion. That’s wrong (presumably unintentional.) 2019 and 2020 numbers are likely similarly misleading.

Yaakov

Dec 3 2018 at 5:01pm

I think that in order to change the public attitude we need more details explaining what will happen and when. The public will not worry about general statements that there will be inflation. Most people do not have that much assets that are not protected against inflation.

I think a good measure would be the percentage of the tax revenue required to service the debt. In 2016, the interest on the debt was $240 billion, which was 6% of the budget. That does not sound alarming to me. An estimate as to when interest payments will require 30% or 50% of tax revenue may help explaining the situation.

Another issue is what options will there be when the problem arrives. The public is used to the politicians working something out. An explanation would require pointing out what was used in the past and why this will not work this time.

One more point is that since the next generations are expected to be much richer than ours, it is hard to convince people that it is bad to steal from the next generations. An analysis showing that despite being richer than us they will have less because of heavy taxes required to service the debt, may change the public attitude, if the analysis is convincing.

Kenneth P

Dec 3 2018 at 11:14pm

The tax cuts contribute to the deficit but at an estimated cost of $100 bil/yr they can hardly be blamed for a trillion dollar deficit. Revenue is up just not as much as spending with the big drivers being defense, social security, homeland security and interest on the debt. Also, I think not being at war is a technicality. War is one of many things that is consistent across administrations.

Scott Sumner

Dec 3 2018 at 11:48pm

robc, Possible, but the S&L effect is small, as state taxes are much lower and less sensitive to economic growth. BTW, I consider myself a moderate supply-sider.

Brian, I’ve never suggested that the entire $300 billion increase was due to taxes. In other posts, I’ve also complained about the surge in government spending. But keep in mind that the deficit should be falling very fast right now. The increase in the deficit is not the impact of Trump’s policies, rather Trump’s policies are far worse than you’d estimate from just looking at the increase in the deficit. The deficit probably should be close to zero right now, and yes, some of the blame goes back to the previous administration.

Bob

Dec 5 2018 at 4:07pm

Brian,

Per Scott, the CBO is required to make it’s projections based on current law. Spending as a percentage of GDP has been pretty flat in recent years. The increase in deficit from 2015 to 2016 was due to the extension of expiring tax cuts from 2009. The CBO’s projections as required assumed the the tax cuts would expire. The 2017 tax bill includes middle class tax cuts that are set to expire in 2022 which is why the 2018 projection flattens out after 2022. The expiring tax cuts were included int he bill to juice the CBO projections so that the impact on the deficit looks smaller. The same was true of the Bush tax cuts. However, the Bush tax cuts were partially extended when they expired, the 2009 tax cuts were partially extended in 2015 when they expired, and the 2017 tax cuts will likely be extended in 2022 when they expire. There is a good chance that they will be offset by rolling back the less popular tax cuts on the higher marginal rates and they will likely juice the CBO numbers with some future spending cuts to occur in 2027, which will likely be repealed in 2027. The folks at the CBO do excellent work. However, Congressional leaders routinely take advantage of the “current law” requirement to force the CBO to deliver unlikely projections. CBO projects remain very useful is you discount for anything with an expiration date.

BTW: If you go back and look at the Paul Ryan spending bills when he chaired appropriations, you’ll see that all of the advertised deficit reduction was due to spending cuts scheduled to occur in the out years. He did so to game the projections.

Mark Z

Dec 4 2018 at 12:42am

I think the ‘crying wolf’ is an inevitable product of short-term electoral politics, and you see it play out similarly with other issues, like climate change. “In about century, the temperature will be 2 degrees celsius higher, and there will be moderately more tropical storms” doesn’t help to win this years election as much as, “in just a few years, there will be three times as many hurricanes and five times as many droughts.” Giving people a precise – and near – day of reckoning, with far more certainty than justified, is useful politically today, but in the long run, it discredits such claims in the minds of the public regardless of who makes them. It’s like credibility inflation. Only by bringing the magnitude/time frame of the rhetoric in line with what’s dispassionate expectations instead of resorting to politically useful exaggeration or over-certainty can confidence in the credibility of those making the claims be restored.

BC

Dec 4 2018 at 2:36am

Deficits seem to be the perfect example of concentrated benefits and dispersed costs. Concentrated interests benefit from spending programs, the costs of which are dispersed among many taxpayers. Then, it is easier still politically to spread those costs among many different not-presently-identifiable people in the future than to impose those costs on any present constituency. Scott’s article, for example, lists many different potential future effects of deficits: more inflation, spending cuts, tax hikes, less capital formation. No one right now can really understand what combination of these will impact whom by how much. For example, who’s future income will be cut by how much as a result of less capital formation? Thus, we have no constituency to push back against deficits.

One obvious solution would be to impose some sort of balanced budget constitutional amendment, if necessary taking effect far enough into the future that no present constituency has a concentrated interest in blocking the amendment. So far, though, there has appeared to have been constituencies with concentrated ideological interests that have blocked past efforts to pass such an amendment.

A more radical approach might be to try to create an anti-deficit constituency. For example, if future deficits automatically triggered future Social Security cuts, then we might expect future seniors to become deficit hawks. However, enacting such a trigger to begin with, or preventing its repeal, would run into the same concentrated benefits problem.

Brian Donohue

Dec 4 2018 at 9:26am

Scott,

I think you suggested precisely that. Quoting:

“Notice that the recent tax cuts are not paying for themselves with faster growth”

followed directly by a graph with two bars. The only logical interpretation I can come up with is that the difference between the two bars, – about $300 billion in FY2018 – is the impact of the tax cut on the deficit. Which is way wrong and misleading.

But maybe I got the wrong end of the stick, and you were trying to make some other point with your comment followed by graph. If so, I’m all ears.

Bob Murphy

Dec 4 2018 at 8:27pm

I like your general take, Scott, but for what it’s worth, I agree with Brian Donohue that your graph doesn’t really prove what you’re claiming. Wouldn’t it be a lot better to show forecasts of revenue collection, pre- and post-tax bill?

Benjamin Cole

Dec 4 2018 at 11:52pm

Give up hope on balanced federal budgets. Dude, this game is over.

From that position, start to devise best (or least bad) options.

Moderate inflation to decrease debt-to-GDP ratios?

The Bank of Japan has bought back 45% of Japan’s gigantic pile of JGBs. They have little inflation. The Fed St. Louis says Fed QE would have to have been four ties larger to have impacted inflation much (Wen paper).

So heavy QE in every recession, and just let the Fed balance sheet grow?

Instead of deficit spending, go to money-financed fiscal programs?

Remember, the option of balanced federal budgets is not on the table. So what is the next best, or least bad, option?

I think heavy QE in recessions is doable, but even better is money-financed fiscal programs.

Thaomas

Dec 5 2018 at 6:55am

I don’t think economists bear very much of the blame for the US deficit being too high at full employment. The clear implication of even “vulgar Keynesianism” is something like a balanced budget over the business cycle or a constant debt/GDP ratio. The structural deficit is clearly the result of the desire of one party to reduce tax collections on the incomes of high income individuals (with the argument that this would increase the supply of entrepreneurship and effort,which economist mainly did not buy) and willing to reduce collections on middle income individuals somewhat to sugar coat the pill, without being able to persuade the public to reduce transfers and government consumption accordingly.

Mark Z

Dec 5 2018 at 11:12pm

But that isn’t clearly the case. One could say, and be equally correct, that it is the result of the desire of (not just one party, but perhaps more one than another) to increase government spending without being able to convince the public to increase taxes accordingly.

In fact, revenue as a % of GDP has been fairly stable for the past few decades, with current revenues pretty close to the trend line, while spending as a % of GDP has soared over the same period, so the spending focused narrative is more consistent with the data than the revenue-focused one.

Thomas Sewell

Dec 6 2018 at 3:22am

Exactly. Federal per capita constant dollars revenue has significantly increased over the last few decades.

The obvious problem is that spending measured the same way (or any other way you want) has simply increased much more, with the obvious results of higher deficits.

Blaming “tax cuts” for a deficit when revenue is actually up over time is ignoring the actual problem of the apparently limitless spending Congress has decided to authorize over time.

Comments are closed.