The media reports that Japan’s GDP plunged at a 6.3% annual rate in the 4th quarter of 2019. Here’s the Financial Times headline and subhead:

Japan on course for technical recession, economists warn

Coronavirus impact looms as GDP shrinks at 6.3% rate after consumption tax rise

The consumption tax increase on October 1, 2019 does largely explain the fall in GDP, but it won’t cause a recession. The coronavirus might cause a recession this year, but it obviously had no impact on 4th quarter GDP.

The fall in GDP was similar to what occurred in April 2014, the last time Japan increased its consumption tax:

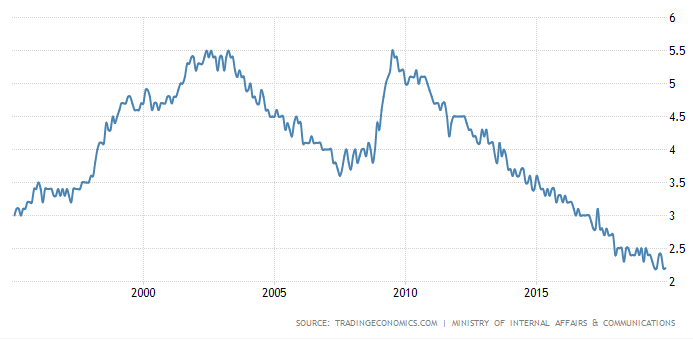

Consumers buy before the tax increase and sales plunge immediately afterwards. But this isn’t a recession in any meaningful sense of the term. When Japan has an actual recession its unemployment rate rises significantly, as in 1998, 2001 and 2008-09. In contrast, the sales tax increases of 2014 and 2019 were followed by a very strong labor market:

The coronavirus poses a risk to Japan because Chinese tourists had become a big source of revenue. It might also disrupt supply lines for manufacturers. I don’t know if Japan will have a technical recession, but I expect Japan’s unemployment rate to show only a very modest and temporary increase. If the coronavirus problem is resolved soon, then it will probably be like 2014, a “recession” in name only.

Most recessions are caused by declines in NGDP that are expected to persist for several years. I.e., by tight money.

READER COMMENTS

TMC

Feb 17 2020 at 1:49pm

A recession is typically longer than a single quarter, I thought at least. I suppose the definition is a little vague.

It’s odd that there was the bump of spending in 2014, but 2019 shows this as the third reduced spending quarter in a row.

FasihZ

Feb 18 2020 at 2:48pm

As far as I’ve heard, the GPD must decline for 2 consecutive quarters for it to be called a recession.

Scott Sumner

Feb 19 2020 at 2:21pm

That’s not the technical definition, at least in the US.

FasihZ

Feb 19 2020 at 2:49pm

Yep, that’s the definition in the UK–not sure about the US.

Mark Z

Feb 17 2020 at 3:16pm

I was a bit confused by Paul Krugman’s tweet blaming this on austerity, but perhaps he was referring to this tax hike? In any case, looking at your graph, it doesn’t seem like these tax cuts have any discernible effect on unemployment. The case for fiscal stimulus seems weak.

Someone in the ensuing Twitter thread remarked that Japan spent “only” 24% of its budget on servicing its debt. Tax increase (and maybe some spending cuts) don’t seem like such a bad idea.

Thaomas

Feb 18 2020 at 10:45am

So was BOJ surprised by the increase? Does the public doubt their commitment to maintaining the PL trend or whatever they are targeting?

Todd Kreider

Feb 19 2020 at 10:38am

1) Japanese labor market simply followed a years long trend in 2014.

2) “Consumers buy before the tax increase and sales plunge immediately afterwards.”

Yet note that this did not occur in 2019, unlike in 2014.

Scott Sumner

Feb 19 2020 at 2:20pm

Yes, the “years long trend” was a strengthening labor market.

There may have been some buying to beat the tax increase, but probably less than in 2014. (The increase was smaller than in 2014.)

Comments are closed.