Tyler Cowen recently linked to a study by Alina Bartscher, Moritz Kuhn, Moritz Schularick, and Paul Wachtel of the effects of “monetary policy” on racial inequality. The study focuses specifically on the effect of unanticipated monetary shocks on racial inequality:

For the empirical analysis, this paper relies on the most widely used monetary policy shock series – the (extended) Romer-Romer shocks (Coibion et al., 2017) as well as different financial market surprise measures taken from Bernanke and Kuttner (2005) and Gertler and Karadi (2015). The estimations yield a consistent result. Over a five-year horizon, accommodative monetary policy leads to larger employment gains for black households, but also to larger wealth gains for white households. More precisely, the black unemployment rate falls by about 0.2 percentage points more than the white unemployment rate after an unexpected 100bp monetary policy shock. But the same shock pushes up stock prices by as much as 5%, and house prices by 2% over a five-year period, while lowering bond yields on corporate and government debt and pushing up inflation. The sustained effects on employment and stock and house prices appear to be a robust feature in the data, across different shock specifications, estimation methods, and sample periods.

These empirical results seem plausible to me, but what are the policy implications? In my entire life, I’ve never met anyone who favored having the Fed go around and create a bunch of “unexpected 100bp monetary policy shocks”.

You might argue that this doesn’t matter, and that the results would also hold for anticipated changes in monetary policy. But decades of macroeconomic research suggests that one cannot draw this inference; unexpected changes in monetary policy have vastly different effects from expected changes in monetary policy. For instance, an unanticipated easing of monetary policy will often boost asset prices, while an anticipated expansionary policy will often reduce asset prices, as during the 1970s.

Now you might argue that asset prices didn’t do poorly during the 1970s because of easy money, they did poorly because of high inflation.

Ahem . . .

When economists have debates about the appropriate monetary policy, they usually agree that policy should in some sense be predictable and stable. Disagreement may occur over issues such as the optimal rate of inflation. One economist may advocate 2% trend inflation, another may advocate 4%, and a third may advocate 0% inflation. Or they might prefer a different target, such as NGDP growth.

A study of the effect of monetary shocks on asset prices tells us nothing about the effect of changes in the steady state rate of inflation. Thus unexpected monetary stimulus often creates a temporary boom, boosting asset prices, while a permanent increase in inflation raises the effective tax rate on real capital income, thus depressing real capital prices. This is what happened during the 1970s.

This means that a temporary switch to easier money will boost the racial wealth gap by raising asset prices, and a permanent switch to much easier money (say 10% inflation) will reduce the wealth gap—but only by making the rich poorer at a faster rate than it makes the poor even poorer.

While I question the authors’ interpretation of their results, I completely agree with the final sentence of their conclusion:

Clearly, this does not mean that achieving racial equity should not be a first-order objective for economic policy. We strongly think it should. But the tools available to central banks might not be the right ones, and could possibly be counter-productive.

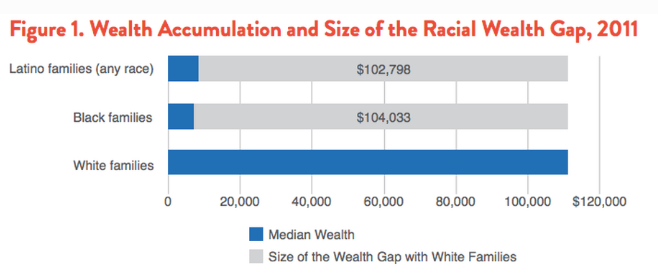

PS. Here’s some data on the racial wealth gap:

READER COMMENTS

Brandon Berg

Feb 9 2021 at 10:27pm

Note that the median white American is nearly a decade older than the median black American, and 15 years older than the median Latino American. Whites are also far more likely to be married. This alone explains a large portion of the gap, but does not fully erase it.

The media like to hype up the racial wealth gap because it’s much larger and more easily sensationalized than the racial income gap, but it’s not at all clear to me that these are distinct phenomena. To establish that they are, we would want to look at wealth controlled for age, marital status, and lifetime earnings.

nobody.really

Feb 10 2021 at 4:00pm

Nice!

Moral: Laymen can rarely understand raw data, even when accurate. Understanding comes from context–and context comes from knowledge.

Thomas Hutcheson

Feb 10 2021 at 10:00am

I’m glad to see Scott address this. I had a different problem with the study as abstracted, the concept of “accomodative” monetary policy. Does that mean macroeconomic results that are greater than its targets? PCE inflation > 2% and “overfull” employment (if that is even possible)?

nobody.really

Feb 10 2021 at 4:08pm

Depressing real capital prices … relative to what? If I anticipate higher inflation, what is a better investment than capital assets? (Ok, I’ll spot you “inflation-indexed investments.”)

Scott Sumner

Feb 10 2021 at 7:56pm

People get pushed toward current consumption, as the after-tax return on capital falls.

nobody.really

Feb 11 2021 at 9:34am

Ah–got it. If we indexed tax brackets to inflation, would that eliminate this dynamic?

Michael Sandifer

Feb 12 2021 at 9:34am

To me, the real message here is that tight money will likely hurt African-Americans disportionately, so avoid tight money by level targeting NGDP.

Comments are closed.