At the moment, the primary problem is obviously the coronavirus epidemic, and its expected impact on business. Another problem is monetary policy, more particularly falling NGDP expectations for the medium to longer-term, when the immediate crisis is over.

The lack of leadership in Washington has not been the major problem, but there are signs that it is becoming increasingly important:

On Wednesday night the global pandemic met US nationalism. It will not take long to see which comes off best. As Donald Trump was speaking, the Dow futures market nosedived.

President Trump’s proposals are widely viewed as ineffective:

He suspended all travel from Europe for 30 days. For the first time since the second world war, direct US travel to the European continent will be closed off. He excluded the UK and Ireland from the ban despite the fact that Britain has almost half the number of US infections with less than a fifth of its population. Moreover, his action contradicted expert guidelines.

The WHO clearly advises against international travel bans because they stifle the flow of medicines and aid, and “may divert resources from other interventions”.

The problem is not the travel ban itself, which might or might not be justified; rather it is the sense of drift in Washington, where policymakers do not seem to be on top of the situation:

His most glaring omission was any plan to increase America’s capacity to test for infections. Epidemiologists say accurate testing is the single most effective method to counter the disease’s spread. It allows the authorities to isolate clusters, trace the movement of the virus and make critical decisions on where the biggest risks lie. That is what places such as Taiwan, Singapore and South Korea have done so effectively without resorting to the draconian measures taken in China.

One solution is to rely more on imports:

The shortage of US kits stems from federal bureaucratic delays. One simple fix would be to import them from Germany, which are WHO-approved.

I presume the shortage of test kits will eventually be addressed. But valuable time has been lost, as Trump issued one misleading statement after another:

1. Trump claimed the stock crash was caused by fear of Bernie Sanders.

2. Trump claimed the Democrats were overhyping the threat from the coronavirus.

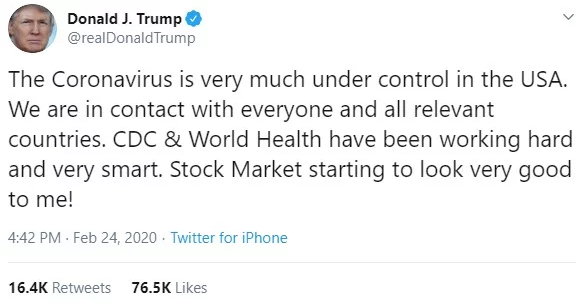

3. Trump claimed the virus was contained, and that the problem was likely to go away in April.

4. Trump suggested that it was a good time to buy stocks, right before they crashed.

5. Trump suggested that we did far better than Europe because we were the first to have a travel ban with China, even though Italy adopted a travel ban on the very same day, and has done far worse than other European countries that delayed their travel bans.

6. Trump compared the virus to the seasonal flu in a misleading fashion.

Trump told his aides to try to hold down the number of reported cases. He appointed unqualified people to top positions in the medical establishment. He dismissed claims that a crisis was imminent and that the US needed a crash program to prepare. He appointed top aides who shielded him from health officials wishing to warn him about the dangers from the coronavirus. He doesn’t like to hear bad news:

“The boss has made it clear, he likes to see his people fight, and he wants the news to be good,” said one adviser to a senior health official involved in the coronavirus response. “This is the world he’s made.”

President swayed by flattery, personal appeals

Trump’s unpredictable demands and attention to public statements — and his own susceptibility to flattery — have created an administration where top officials feel constantly at siege, worried that the next presidential tweet will decide their professional future, and panicked that they need to regularly impress him.

And yet, all of these missteps had only a marginal impact on outcomes. Presidents simply are not that influential, and even if we had a different president we’d likely be facing a severe crisis today. The real problem is that the federal government has been exposed as “the emperor with no clothes.” They had no plan for dealing with a pandemic. You need the plan in place before the pandemic reaches our shores. You need the plan before the pandemic hits Wuhan. You need the plan in place even before Trump was elected. The countries in East Asia that were hit by SARS did have a plan in place, and thus far have done a better job of preventing the virus from “going exponential”. (Of course that’s no guarantee of future success.)

In the past, Trump supporters argued that the weaknesses in his leadership style didn’t matter as long as he appointed conservatives to the Supreme Court and cut taxes. Even if I am right that presidential leadership has only a marginal impact on outcomes, Trump’s various statements may come back to haunt him with voters, especially if the crisis gets far worse.

READER COMMENTS

Ray

Mar 12 2020 at 10:00pm

Seems like there’s a political agenda to this post.

Rebes

Mar 12 2020 at 10:06pm

Yes. And that political agenda is: speak the truth.

britman

Mar 12 2020 at 10:10pm

Do ya think?

Scott Sumner

Mar 12 2020 at 10:22pm

There are undoubtedly political implications in any attempt to ascertain market responses to presidential speeches.

Thomas Sewell

Mar 13 2020 at 9:38pm

Here’s a different take on the reasons from Barron’s: Why President Donald Trump’s Speech Spooked the Stock Market

You might also note the jump/recovery today as well. Looking forward to Scott’s take on that. Will he praise Trump in response?

There’s a lot of speculation and very little fact nor economic theory present in this post.

Mark Z

Mar 12 2020 at 10:25pm

It seems cargo transportation is exempt from the travel ban, and it only applies to passenger travel. Though the reduction in bellyhold cargo in passenger planes could adversely affect the supply of goods.

That guy’s obsession with the stock market, it defies comprehension. Presidents historically have embraced their legacies being defined by the crises that occurred during their tenures and their reactions thereto; FDR and Pearl Harbor, Bush and 9/11; and posterity generally rewards them. There’s no earthly reason to respond to an exogenous crisis by minimizing it.

Michael Sandifer

Mar 13 2020 at 1:29am

Scott,

While I appreciate your push for looser policy during crises and in the immediate years following, does your model ultimately have a problem?

For example, since wages are typically said to adjust vis-a-vis NGDP within about 3-4 years, why should the yield curve recently have flattened decades into the future in response to a real crisis that might last two years, at the very most? Are markets predicting hysterisis, and/or other real problems, or is this all nominal?

Is the simple average wage/MGDP or ECI/NGDP ratio really the indicator of choice when it comes to determining the level of wage adjustment, or the long-term trend path of those ratios?

https://fred.stlouisfed.org/graph/?g=ql45

Notice in the graph that the average wage/NGDP ratio returns to the pre-recession ratio by 2013. However, the decline in average wage/NGDP is still behind the pre-recession trend.

Granted, Treasury trading has some nuances, as the lack of liquidity in the market that was alleviated today demonstrates. Still, long rates are way, way down.

Scott Sumner

Mar 13 2020 at 12:18pm

I don’t know all the reasons for the sharp fall in long-term rates. It may be a mix of a rush for safety, lower inflation expectations, and lower real growth expectations. But it’s a bit of a puzzle.

Thomas Knapp

Mar 13 2020 at 6:30am

“Trump claimed the Democrats were overhyping the threat from the coronavirus.”

Well, that one is true, anyway.

At the moment, it still looks like the hysteria over the virus is going to do far more damage than the virus itself.

Michael Sandifer

Mar 13 2020 at 7:04am

Thomas,

I’m curious, how many Americans have to die of this virus before you say it wasn’t over-hyped? 500,000? 1,000,000? 1,500,000?

Thomas Hutcheson

Mar 13 2020 at 8:15am

Have Republicans been hyping it exactly enough? 🙂

Agree that across the board, too little thought has gone into trying to balance the costs and benefits of prevention measures. Total lock-down of a city seems too much. OTOH, there will be long term benefits from firms discovering just how much more effective judicious mixtures of work from home can be.

Thomas Hutcheson

Mar 13 2020 at 7:41am

I’d say that markets are far more worried that the Fed will not “do what it takes to keep NGDP growing at 4-5% pa than what the President said or did not do.

Mark

Mar 13 2020 at 8:05am

I think a major reason behind the markets’ pessimism is the possibility that some form of the travel restrictions, social distancing, and other measures stay in place permanently. Suppose we don’t have a vaccine for two years and we just have to live like this for the next two years and people get used to it. Or even if there is a vaccine, governments insist travel has to remain limited so they have the ability to respond to the next disease. Restrictions on people’s liberty frequently never go away even after the original threat is over, such as many restrictions after 9/11. If this scenario comes to pass, the world’s economy will remain permanently depressed.

Scott Sumner

Mar 13 2020 at 12:20pm

Yes, I’ve wondered the same thing. Very depressing, but quite plausible. Look how 9/11 changed our lives permanently.

sty.silver

Mar 13 2020 at 8:52am

I’m having some trouble believing this. The stats I’ve seen indicate that republicans are significantly less worried about the virus than Democrats, and I’ve imagined a fairly direct link to this from Trump’s rhetoric. Imagine that, instead of downplaying the virus, he had given a speech weeks ago about how (a) this is extremely serious and (b) the thing everyone needs to remember is to stay away from coughing and sneezing people and not touch their face. Would the difference between the current world and that hypothetical world really be small?

Scott Sumner

Mar 13 2020 at 12:22pm

In my view the main issue is not a lack of presidential speeches to warn the public, it’s a lack of testing kits. To the extent Trump has not helped things, it’s mostly appointing the wrong people and not lighting a fire under the bureaucracy to move faster.

Peter McCluskey

Mar 13 2020 at 10:28am

The markets are saying that they don’t have enough liquidity to handle margin calls very well.

The markets will mostly have a sensible reaction to the virus next week. The Fed will likely be slower to react sensibly. And who know whether Trump will learn enough from the market to keep his job?

pc

Mar 13 2020 at 12:25pm

Scott,

I agree with the post, but I wonder if you could comment on markets assuming weakness in other sectors of the economy that won’t be able to withstand this shock. Where are they? Will they cascade?

My biggest structural concern is the % of population who have effectively zero savings, relying on credit cards for life basics let alone healthcare. Will unprecedented personal bankruptcy have a broader impact?

Ilverin

Mar 13 2020 at 10:48pm

It seems the team Trump fired did not have a good plan in place, but he did fire the team. Any plan is probably better than no plan. https://www.snopes.com/fact-check/trump-fire-pandemic-team/

Mark Z

Mar 14 2020 at 8:57pm

One reason why I don’t quite trust Snopes: regarding the related claim that “Trump also cut funding for the CDC,” they call it partially true, then provide an elaboration which shows that it is actually false.

Philo

Mar 14 2020 at 12:21pm

“Trump’s various statements may come back to haunt him with voters . . . .” It seems likely that the coronavirus, if it doesn’t kill him first, will make Joe Biden President.

Comments are closed.