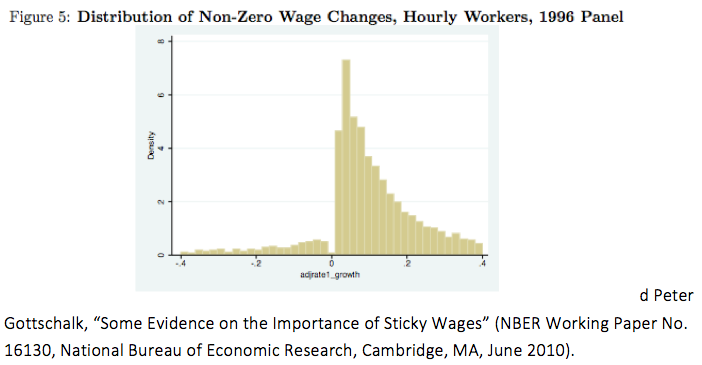

When macroeconomists talk about wage stickiness, they are generally referring to nominal stickiness. Because nominal wages are slow to adjust, a sudden and unexpected change in NGDP will usually impact employment, often in a sub-optimal fashion.

It’s possible to construct a variable called “real wages”, but I don’t view that as a useful concept. This is partly because (like Keynes) I don’t view inflation as being a particular useful concept, except perhaps when trying to come up with ballpark figures for long run changes in living standards. The problem is not so much that inflation figures are wrong; it’s not even clear what inflation is supposed to measure.

Here’s Tyler Cowen:

The restaurant used to pay you $13 an hour, now they pay you “$13 an hour plus p = ?? of Covid-19.” That new wage is a lower real wage.

That’s a defensible claim, if you define “inflation” in a certain way. But it’s also an example where the nominal wage is “sticky”, and hence this example has no bearing on “sticky wage models of the business cycle”. Again, it’s nominal wages and nominal GDP that matter, ignore real wages.

Tyler’s post is entitled “Real wages are flexible now”. But the post does not contain any supporting evidence for that claim. A change in the real wage is not evidence of increased flexibility.

For example, real wages rose sharply in 1930. Does the big change in real wages in 1930 show that real wages were increasingly flexible? No, they rose because prices fell while nominal wages were fairly stable. A flexible real wage is one that moves toward equilibrium, not one that randomly moves around due to some price level shock even as nominal wages are fixed. As an analogy, if The Soviet Union had raised the official price of bread from one ruble to two rubles, it doesn’t mean that bread prices are becoming more flexible, just that they are fixed at a different level.

I expect unemployment levels to rise to new and scary heights, and yes I do think the government should do something about that. But if you are analyzing the status quo with “a sticky wage model,” that assumption is probably wrong. Even though it is usually correct.

It’s true that sticky wages are not the reason why unemployment is about to surge much higher. We are facing an unusually large “real shock.” Nonetheless, nominal wage stickiness remains very relevant, as it is quite likely that 12 months from today we will have an elevated unemployment rate due to sticky nominal wages and lower than trend NGDP. I hope I’m wrong, but the financial markets seem to view it as a very real threat.