Over the past year, the US has been hit by a pretty severe labor supply shock. Employment is sharply depressed, but wages are rising fast and companies are having trouble finding workers. At this point the question is not whether a labor supply shock exists, rather the issue is what is causing labor supply to be so depressed. I’ve seen at least three theories:

1. A supplemental unemployment insurance program that pays lower wage workers more than they earned on their previous jobs.

2. Lack of childcare, partly due to school closures.

3. Fear of the health risk associated with working.

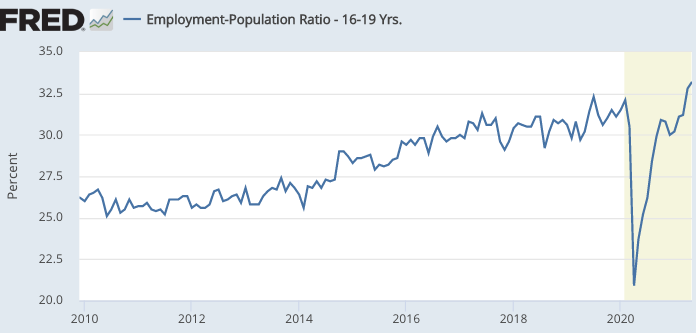

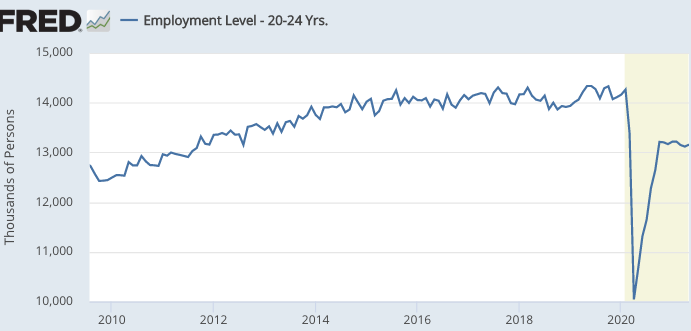

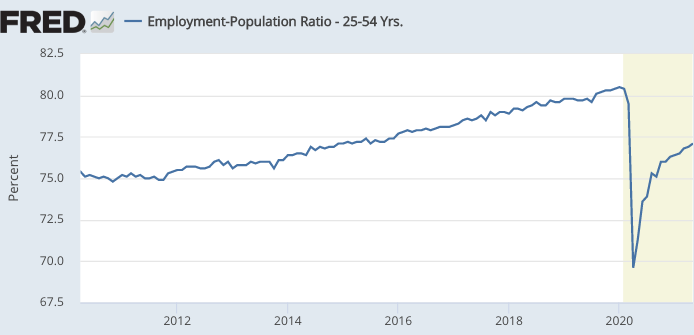

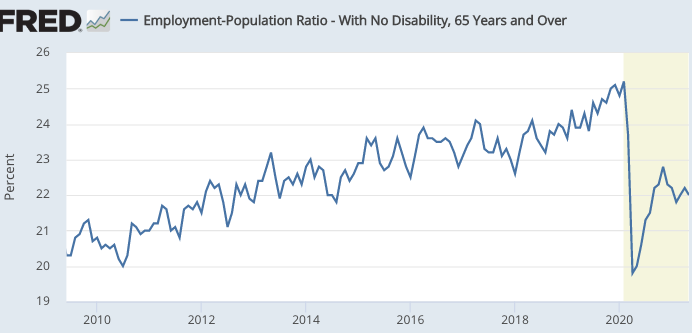

In order to evaluate those theories, let’s look at some employment data. Unfortunately, while I found employment/population ratios for three age groups, for 20-24 year olds I had to rely on total employment data. Let’s start with teenagers:

Teen employment is at the highest level since the Great Recession, even higher than the extremely strong labor market of 2019. Given the current state of the labor market, that’s actually pretty amazing. (Yes, the employment ratio is far below the levels of the 20th century, but teens were far more likely to work in the old days.)

So there’s little evidence of a negative labor supply shock for teens. To be sure, the supply curve for teens may have shifted slightly to the left, and that effect could have been offset by moving up and to the right along the curve due to higher wage rates. Even so, the teen data really stands out when compared to other age groups.

Unfortunately, the high teen rate of employment is consistent with all three theories discussed above. They typically have not been receiving UI, they typically don’t have child care issues, and they are at relatively low risk from Covid. So let’s look at three other age groups:

My first reaction is that fear of getting Covid is not the whole story. The difference between employment levels for teens vs. 20-24 year olds is pretty shocking. Teen employment is higher than during the 2019 boom, whereas employment of workers just a few years older is still severely depressed. Obviously there is very little difference between the health risk for teens and young adults. In both cases, the risk is pretty low. That means the very strong employment ratio for teens is likely due to either the fact that they typically do not received UI or the fact that they don’t need child care.

All three of the adult age groups show significant declines in employment. In percentage terms (not percentage points terms) the decline is largest for old people, somewhat less for young workers, and even less for middle age people. And yet unless I’m mistaken, childcare issues are most important for middle age people.

I am especially struck by the fact that employment for 20-24 year olds seems to have declined more sharply than for 25-54 year olds. They experience less health risk than 25-54 year olds, and they probably have less need for childcare. On the other hand, 20-24 year olds tend to be lower wage workers, the group most likely to earn more on unemployment insurance than on their former jobs.

While I suspect that all three factors are depressing labor supply, the strongest evidence seems to be for the effect of the supplemental UI program.

Labor supply shocks make things difficult for policymakers, especially policymakers that focus on the employment part of the Fed’s dual mandate. In 1974, the US experienced a negative labor supply shock, and this contributed heavily to a “supply-shock” recession. The longer this supply shock lasts, the more likely that it will trigger an outcome similar to 1974.

To be sure, the 1974 labor supply shock had completely different causes—the removal of the Nixon wage controls:

Nonetheless, a labor supply shock has a contractionary impact on the economy, regardless of the cause. Thus far, the effect is not to cause a recession, rather it is merely slowing the recovery from a recession. But there is a risk that this problem could confuse monetary policymakers and lead to an overshoot of inflation. Yes, the Fed wants to see a mild overshoot of inflation, but a major overshoot would lead to subsequent tightening (as the Fed needs to hit its 2% average inflation target.)

As always, the Fed needs to avoid targeting real variables such as employment. That’s where they got in trouble during the late 1960s and 1970s. Phillips Curve thinking also contributed to the inflation undershoot during the late 2010s. Stick to nominal targets.