Oil Speculators: Bad or Good

By Robert P. Murphy

“If speculators had driven futures prices far above the level justified by fundamentals, we should have seen contango and/or large buildups in inventories. Yet, we see neither telltale sign.”

In this article, I make three main points. First, the theory of speculators driving oil prices does not fit the empirical evidence. Second, speculation—even by large institutional investors—plays a beneficial role in the oil markets. Finally, even if it were true that speculators were driving up prices, and even if this were a bad thing, it still would not follow that a federal government crackdown would make things better. Once again, it seems that the government has proposed a solution to an imaginary problem—a solution that won’t work as advertised. The situation is roughly analogous to the head of FEMA performing a rain dance after Hurricane Katrina, on the theory that extra precipitation would help displaced residents move back into their flooded neighborhoods.

Speculators Are Casing An Oil Bubble? Prove It!

Although hedge fund manager Michael Masters’s congressional testimony2 contained many impressive statistics showing the correlation between the rise in the price of oil and the amount of institutional money invested in commodities, economic theory shows that crucial telltale signs of an investment bubble are missing.

Let’s suppose for a moment that speculators really were driving oil prices above the level supported by the so-called fundamentals. For concreteness, imagine that at a price of $70 per barrel, producers would bring 85 million barrels (roughly the world’s current output of petroleum) to market per day, while physical consumers (refiners, industry, etc.) would purchase 85 million barrels per day. Quantity supplied equals quantity demanded, and economists can sleep at night.

Now imagine that, for whatever reason, outside investors who have nothing intrinsically to do with the oil market, begin buying billions of dollars’ worth of futures contracts. That is, they enter legally binding contracts with oil producers, where the investors agree that on a specified future date—say, twelve months in the future—they will hand over a certain amount of cash in exchange for 1,000 barrels of oil.

Naturally, the more of these contracts the investors snatch up, the higher the price they need to pay the oil producers. As the producers sell more and more, they realize that their capacity at that future date will eventually be reached. (They’ve already sold the “normal” number of futures contracts to airlines and other hedgers.)

Yet, the speculative investors continue to bid ever-higher amounts for the futures contracts for oil to be delivered in one year’s time. As the futures price climbs higher and higher, more and more people in the market believe it is excessive. When it hits $100 (compared to the current spot price of $70), there are many bearish speculators who have entered the futures market to take a short position, meaning that they have sold some of the futures contracts being purchased by the other, bullish speculators. At this point, the physical producers of oil aren’t even involved because the long and short speculators are simply making a side bet, as if they were spectators watching the “game” of the oil market play out.

This suggests the first sign to look for if we want to establish that speculators have manipulated the price. If they were truly responsible for a massive spike in oil prices, there should have been a period of contango, a situation in which futures prices are higher than spot prices. (Note, though, that although price manipulation implies contango, contango does not necessarily imply price manipulation. Contango can exist in a market in which no price manipulation occurs.) Although there was a long stretch of contango, it ended in July 2007, and, since then, the oil market has generally been in backwardation,3 where the spot price has been higher than the futures prices for various future dates.

For more on the contango, see The Bootstrap Theory of the Oil Price, by Anthony de Jasay. Library of Economics and Liberty, July 7, 2008. For more on futures markets and speculation, see Futures and Options Markets, in the Concise Encyclopedia of Economics.

But wait—there is a possible explanation for the lack of contango. If the gap between the futures and spot price becomes large enough, people have the incentive to stockpile physical barrels of oil. For example, in our story, suppose that the futures price for one year out hits $140. Investors could then buy 1,000 barrels of spot oil at $70 each, short a futures contract, wait twelve months, and finally deliver the oil for $140 per barrel as the contract stipulates. The $70 profit per barrel would surely cover interest on the invested capital, storage costs, insurance, and other risks.

Obviously, this type of arbitrage opportunity would not persist. Assuming that the bullish speculators (who had initially driven up futures prices) kept buying contracts no matter what, that futures price would remain stuck at $140. Investors today would buy oil on the spot market to stockpile it, until the spot price had risen so high that it no longer made sense to tie up one’s money in the operation for twelve months. This, in fact, is the mechanism through which speculators in futures contracts could drive up spot prices. If the term structure data being analyzed came out infrequently, all of the dynamism might be missed; the analyst could see spot and futures prices at $70 in week one, and then both would be around $140 in week two. Thus, say some proponents of the speculative bubble theory, the lack of the contango signature doesn’t exonerate speculators from manipulating prices.

Even so, we would have another telltale sign that speculators were driving the massive price increase: Crude inventories would grow. After all, for the spot price to be driven up, the barrels being delivered to market have to be diverted from the traditional (fundamental) users. If we initially had an equilibrium of 85 million barrels per day at $70 per barrel, a new price of $140 per barrel would lead to a large surplus. It’s true that supply and demand in oil markets are notoriously inelastic, meaning that large changes in price cause only small changes in quantities supplied and demanded. Nonetheless, a 100-percent increase in price would surely lead to a large excess of quantity supplied over quantity demanded (by traditional users) in the spot market. At $140 per barrel, perhaps producers would bring 86 million barrels to market, while refiners, industrial customers, and other traditional purchasers would buy only 84 million barrels. For this to occur, two million barrels a day would need to flow into inventories.

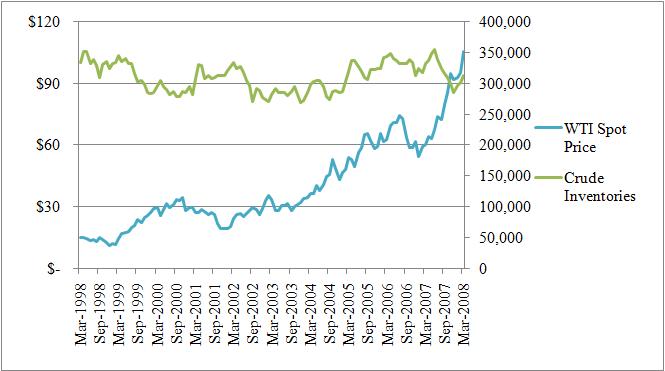

As with the term structure of oil prices, the data do not show any signs of such inventory accumulation. As the chart below illustrates, commercial inventories in the United States appear to be unaffected by the sharp jump in spot crude prices.

Figure 1. West Texas International Crude Oil Spot Price versus U.S. Commercial Crude Inventories (monthly, thousands bbls)

To repeat: If speculators had driven futures prices far above the level justified by fundamentals, we should have seen contango and/or large buildups in inventories. Yet, we see neither telltale sign; oil prices have been in backwardation for much of the run-up in prices, and (as Figure 1 illustrates) commercial oil inventories in the United States have hovered in a stable range for a decade.

Those promulgating the speculative bubble theory have one final card to play: Suppose that the investors in futures contracts have indeed pushed up the futures price to $140, even though the fundamentals would support only $70. But now, the way to raise the spot price up to $140 isn’t to increase demand (from those stockpiling crude), but rather to reduce supply. For example, suppose that OPEC ministers supply the bulk of the contracts purchased by the institutional investors, and this doesn’t represent a problem because OPEC countries originally had plenty of spare pumping capacity available in twelve months. Knowing that they can unload their oil next year for a locked-in price of $140 per barrel, why would they continue pumping at the same rate in the present, earning only $70 per barrel?

Under this theory, the OPEC ministers accompany their huge short position in futures contracts with a cutback in current output. This would explain the similar level of spot and futures prices at $140, and the lack of growing inventories. In effect, OPEC would be propping up spot prices by diverting supplies from the market, but they would be hoarding it underground, not in above-ground tanks or storage facilities where statisticians could count it.

Alas, the data simply do not support this theory. As with the term structure of prices, the data on OPEC production are the exact opposite of what our story requires. According to EIA estimates, though OPEC output did indeed decline from 2005 through the first quarter of 2007, it increased every quarter from that point on. In particular, OPEC output was at an all-time high in the first quarter of 2008.5 Thus, OPEC ramped up its output during the very period when spot oil prices increased the most.

It is clear, then, that in light of the facts, the theory that institutional investors have doubled oil prices grows ever more convoluted. The latest twist involves massive quantities of oil stockpiled in Iranian tankers. 6 Although it is always possible that speculators are responsible—and have eluded the obvious signs described above—it seems more plausible that the bulk of the increase in oil prices is due to more-mundane causes: increases in demand (especially from China); stagnant world supply; and a dollar that plunged more than 15 percent against the euro between June 2007 and June 2008.

The Beneficial Role of Institutional “Speculators”

I’ve shown that speculators probably are not responsible for record oil prices. Now consider the benefits of their activities.

First, all speculators perform the vital service of speeding price adjustments and reducing volatility. After all, a speculator buys low and sells high (or short sells high and buys back low). Over the entire cycle of the commodity’s price, speculation actually reduces volatility because buying (when the price is low) pushes up prices, and selling (when high) pushes them down. Thus, the true speculator—i.e., one who is not connected with the commodity and is truly just betting on the price move—profits to the extent that he accurately anticipates the future and is penalized in exact proportion to how poorly he forecasts. In an oil market plagued by a possible Israeli or U.S. airstrike on Iran, saboteurs in Iraq and Nigeria, sputtering economies that may restrict demand, and political wrangling over offshore drilling, speculators ensure that expert knowledge in all of these fields gets reflected in the market prices very quickly.

The reasoning above shows that, ironically, even if the evidence showed that speculators had been responsible for the huge increase in oil prices, there would still be a prima facie case for saluting their behavior! For example, if Israel bombs Iran, which then cuts off exports and mines the Strait of Hormuz, as many fear, then spot oil prices could exceed $400 per barrel. In such an environment, people would be grateful for large inventories that had been accumulated because of speculative changes in the term structure, and for the increased conservation that $140 oil had enforced in the months before the new war. Free-market economists understand the beneficial role that prices play in coordinating production and consumption; this role holds true for futures prices and the allocation of resources between present and future uses. True speculators ensure that futures prices are as accurate as possible and, thus, that futures prices coordinate behavior as effectively as possible.

But what of institutional investors, such as mutual or pension funds? If managers of these entities opt for a two-percent exposure to an index of commodities, this is because they’re trying to ride the momentum; it’s not that they have a hotline to commandoes in Iran and realize that war is imminent. So aren’t these investors distorting the price- discovery process by throwing their billions into the mix?

Again, the market has built-in incentives to discourage the truly ignorant from throwing their money away. If these investors are wrong, if they are pushing up prices in a self-fulfilling but unsustainable bubble, they stand to lose the most from their foolishness. Yes, bubbles are possible—the housing market comes to mind—but if the government slaps on artificial penalties or constraints for those who make mistakes, it distorts the incentives for risky investment. Moreover, if politicians really knew beforehand which investments were smart and which were foolish, we wouldn’t need financial markets.

A final point is that the reason pension managers and others are buying oil futures is not necessarily that they can accurately predict continued price increases. Rather, they may be incorporating commodities directly into their portfolios to hedge their clients against further pain from unprecedented price spikes. Even the harshest critics don’t mind when airlines buy futures contracts in oil because they are obviously hedging themselves against price moves that could devastate their business. When Southwest Airlines, for example, adjusted its fuel-hedging operations in 2000 with swaps and call options, it was only trying to protect itself from price increases that did, in fact, occur; Southwest was not trying to drive up the price of oil.7 But, by the same token, a retired schoolteacher living on a fixed income can be devastated when gasoline prices double, and so if her pension manager invests in oil futures, this can be viewed as simple hedging.

Federal Meddling Never Helps

This last observation shows the danger of proposals to further regulate or even ban institutional investment in commodity futures. Even if speculators were driving up oil prices, and even if this were a bad thing, the measures being discussed would barely change things. Millionaires who wanted to bet on oil could still do so in foreign markets and would, thus, still push up the price of oil. The government can’t stamp out cocaine trafficking, and it can’t prevent oil speculation.

However, just as the Drug War can distort markets and lead to all sorts of unnecessary misery, the same will happen if the federal government cracks down on institutional investments in oil futures. The underlying “problem” would remain, but now citizens of modest means would have no way to protect themselves against further increases in oil prices, which not only lead to higher gas prices, but also tend to hurt other stocks.

In short, the data do not support the theory that speculators are responsible for the huge increase in oil prices. Moreover, even if they were responsible, markets provide incentives for speculative activity to be helpful; they do so by causing smooth and rapid price adjustments. Finally, the proposed legislation wouldn’t prevent speculators from moving oil prices; it would simply prevent institutional managers from shielding their clients from volatile markets.

“Gas could fall to $2 if Congress acts, analysts say,” MarketWatch.com, June 23, 2008.

See Paul Krugman’s New York Times blog post of June 23, 2008, “Speculative nonsense, once again.”

In Figure 1, the WTI spot price data are available in this EIA menu of Spot Prices while the commercial inventories data are available in this EIA menu of Total Stocks.

See EIA’s World Oil Balance [MS Excel .xls file], accessed July 16, 2008.

Ed Wallace, “ICE, ICE, Baby,” Star Telegram, May 19, 2008.

The Wikipedia entry on Southwest Airlines contains a description of its very successful hedging strategy.