China's Growth: Planning or Private Enterprise?

By Paul Gregory

“The remarkable feature of China is that despite the private sector’s disadvantages in credit markets, it has advanced and outgrown the privileged state sector.”

But Ludwig von Mises in the 1920s and F. A. Hayek in the 1930s discredited the idea that planners can manage an entire economy. Hayek pointed out that central planners lack “the knowledge of the particular circumstances of time and place.”2 Because the planners do not have the information that rests with hundreds of thousands of companies and millions of consumers, planning fails, as it did spectacularly in the Soviet Union. Interestingly, even socialist economist Robert Heilbroner admitted as much.3 China is not an exception. Its economic growth has occurred despite the government’s economic planning and because of its large, dynamic private sector.

China’s Economic Growth

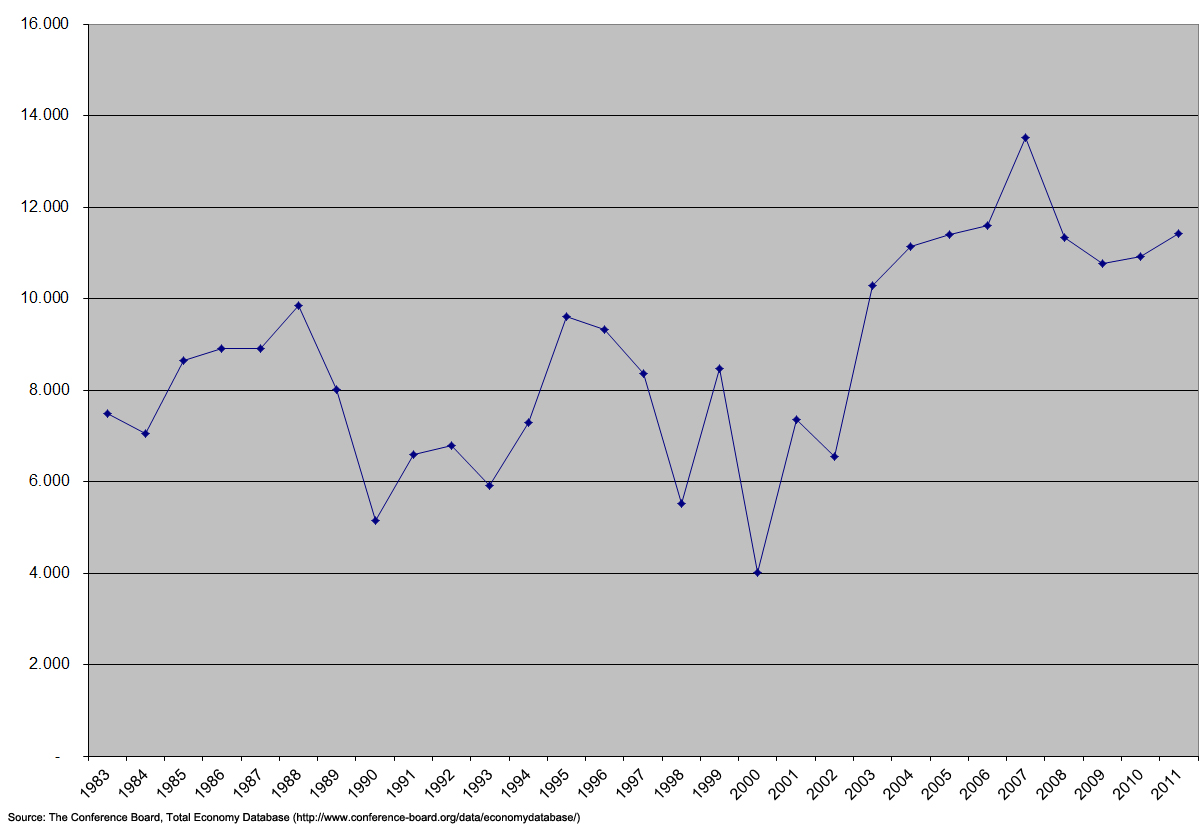

As Figure 1 shows, China’s Gross Domestic Product grew from 1979 to the present at an average of slightly over 8.5 percent per annum. Although Japan and the Four Tigers (Hong Kong, Singapore, South Korea, and Taiwan) matched that growth rate at various points in the past, more than thirty years of such high growth is unique. The CPC would like us to believe its growth is due to its peculiar brand of socialism with a Chinese face. In fact, what deserves credit is the entrepreneurship of the Chinese people.

Figure 1. China’s Growth Rate of GDP, 1983-2011

The Official Narrative

The official narrative of an enlightened CPC echoes the “scientific planning” claims of the Soviet Union. Defenders of the official narrative refer to the CPC as “more enlightened” and “learning-minded” and claim that its major mistakes (Great Leap Forward, Cultural Revolution) are things of the past. Competing in the world economy is difficult, but the Chinese economy, they claim, is guided by party leaders who are “highly intelligent, extremely well educated, and have wide ranging experience.” They are “some of the most capable leaders in the world.” Premature democracy is dangerous because it “sacrifice[s] long-term economic development for short-term political freedom, and therefore does not bring the greatest good to the greatest number.”4

Some economists buy the story that one-party rule enables poor countries to make tough decisions that “messy” democracies cannot.5 The most developed line of argument comes from Nobel laureate Eric Maskin and his Chinese co-authors, who cite regional competition among officials as the key to Chinese success.6 Instead of micromanaging the entire economy, they write, the CPC appoints and monitors the bosses who run its provinces, cities, and municipalities. Because of China’s size, regions are often the equivalent of medium-sized countries. Regional mayors, governors, and local party bosses run relatively self-contained and self-sufficient regions. Nearly 70 percent of total government expenditure in China takes place at the sub-national level.7

The CPC, however, tightly controls appointments, promotions, demotions and firings. Maskin et al. argue that the CPC runs a tournament among regional bosses to promote those who produce high growth rates, achieve low rates of unemployment, or attract foreign direct investment.8 Indeed, empirical studies show that promotions of Chinese regional officials depend on relative growth and job creation.

This “efficient CPC” narrative rings false on a number of accounts. Tales of lurid corruption and excesses of princelings (children of the first-generation CPC leaders)9 belie the image of a benevolent CPC. That still-poor China has more billionaires than any country other than the United States raises additional suspicions.10 Political economists have long demonstrated that “benevolent” dictatorships are torn apart by principal-agent problems, greed, opportunistic behavior, and corruption. Why would China be an exception?

Competition among regional state and party leaders proved disastrous in the planned Soviet economy. Competitors found that cheating was best way to win. At the end, the Soviet economy generated more false information than even Hayek might have expected. Chinese regional bosses have also learned to manipulate growth through public investments or by simply cooking the books, as recent investigations of a disgraced princeling revealed.11

Another sour note for China’s state capitalism is that China’s weak property rights, corruption, and absence of a rule of law and of economic freedom put China in league with some of the worst countries in the world. China ranks 75th on Transparency International’s corruption index12 and 138th in the Economic Freedom Index, right between Guyana and Syria.13 World experience shows that poor institutions are inconsistent with growth. The Chinese state economy is rife with such impediments to growth. Yet it grows. That is the puzzle.

China has Grown because of Private Enterprises

China’s private enterprise reforms began first in agriculture in 1978 and spread from there. Agriculture accounted for most of Chinese output and most of the labor force when Mao died in 1976 and the reform period could begin. The freeing of agriculture from collective farms is the most important untold part of the Chinese growth story.

Agricultural reforms began spontaneously from below, even before the “Reform” Party Congress of 1978 that installed reformer Deng Xiaping in power. A Chinese reform official later admitted: “In fact, reform wasn’t discussed. Reform wasn’t listed on the agenda, nor was it mentioned in the work reports.”14 What became known as the “contract responsibility system” was sparked spontaneously by eighteen peasants from Xiaogang village in Anhui province. They secretly divided communal land in November 1978 and agreed to farm their plots individually, each contributing their share of the state quota. The state got its due and the peasants kept what was left over. The peasants’ separation of their land from the collective farm was illegal, highly dangerous, and done without the approval of regional officials. Why did they take the chance?

Kate Zhou explains that the peasants had seen their parents and children die from starvation during the 1958-1961 famine of the Great Leap Forward. They understood they had to take care of themselves. The contract responsibility system spread like wildfire from village to village and from province to province, notably without endorsement by or encouragement from regional or national authorities.15

As agricultural production soared, Deng Xiaping and his CPC realized that they should not resist something that was working. By 1982, more than 90 percent of rural dwellers worked under the contract responsibility system, but they were allowed only one- to three-year contracts on their land. It was only in 2003 that the state gave out longer-term leases.16

The spontaneous reforms in agriculture meant that new supplies of food products needed markets and that markets needed infrastructure. Rural dwellers created a private trade network, and, within one year, most state food stores were out of business. Rural entrepreneurs then created new businesses, such as hotels, services, private restaurants, and small-scale manufacturing, through the three Fs (friends, family and fools17). They bribed local officials to register their companies as “township and village enterprises.” They created fake “red hat” enterprises, that is, private companies masquerading as state companies, and sham collective enterprises, or they used state enterprises to issue receipts and open bank accounts. Large private manufacturing firms developed first in predominantly agricultural provinces. China’s largest agribusiness was founded by brothers who left the city to found their company in rural Sichuan. Rural entrepreneurs built the largest refrigeration and air-conditioning companies in China.

China at the Crossroads: State Advance, Private Retreat?

China is, in fact, two separate economies: the private and the state. The “private” economy includes joint ventures with Hong Kong and Taiwanese entrepreneurs, medium and small manufacturing and service businesses, food-processing plants, and just about everything else. The most successful private enterprises are listed on Chinese stock exchanges. Having shareholders gives added protection from arbitrary state action. State officials think twice about alienating hundreds of shareholders versus only a few owners. The private economy has operated in a shadowy world of semi-legality and has had to survive on its own wits. It had to wait until 2007 for the Chinese legislature to recognize the legitimacy of private property.

The state sector of “national champions,” run by the CPC or by closely-connected persons, is the second Chinese economy. There are more than 150,000 state-owned enterprises after the weeding out of unprofitable state enterprises under the policy of “grasping the big and letting go of the small,” begun in 1998.18 They decided that the government would control the biggest and most important companies but let the smaller ones fend for themselves. These 150,000 companies account for only three percent of the total number of state and private companies, but for more than 90 percent of the market value of listed Chinese companies.

Many private enterprises formally operate under the legal protection of state or collective enterprises. Hence, it is difficult to calculate the shares of the state and private economies. If we adopt the broadest definition, the state economy is, at most, half.19 China today is split roughly fifty-fifty between the state and private economies.

We lack exact calculations of the relative rates of growth of the state and private economies, but the private economy, with an average growth rate of nearly nine percent from 1980 to the present, has grown much faster than the state sector. In 1978, state enterprises and rural communes produced all of China’s GDP. By 2004, there were more than three million private companies employing more than 47 million workers.20 By 2011, there were 52 million private companies employing 160 million workers.21 Clearly, the major part of China’s growth has come from private initiative.

The private economy performs better than the state economy. An OECD study finds that total factor productivity of privately controlled enterprises is twice that of state-owned enterprises.22 (Total factor productivity is the amount of output for each unit of labor and capital input.) Private companies earn higher profits, and state enterprises earn a four- percent return on capital, versus much higher rates for private companies. 23 If state enterprises average profit rates of four percent, then, whenever inflation exceeds four percent, their real profit rate is negative. Private companies borrow in private markets at rates up to 18 percent. They must earn profit rates above that if they are to continue in business.24

Private-sector growth has occurred despite many obstacles and disadvantages. CPC policy over the past two decades is captured by the slogan, “The state advances, the private sector retreats.” A Chinese official characterizes this policy as “leaving the private sector drinking the soup while the state enterprises are eating the meat.”25 Discrimination against the private sector is seen in its higher taxes, stricter regulation, and bureaucratic meddling. State companies use their advantages to drive out private competitors, as did the three state air carriers in driving seven of eight private competitors out of the market.26 The most blatant form of discrimination is practiced by the state banks, which make only four percent of their loans to private businesses. Private businesses must borrow in unofficial credit markets, which can be a criminal offense punished by long jail terms or worse. 27

China’s credit market is a “political market,” which lends on connections and government intervention rather than commercial considerations. A nation’s capital market is a primary determinant of its economic performance. If scarce credit goes to projects with low rates of return and higher-return projects are excluded, economic growth and efficiency suffer. This is a universal rule of economics. China appears to squander a great deal of its huge household savings on roads and bridges to nowhere, opera houses in towns with no opera, and empty high-speed trains.

As I write this piece, China’s National Party Congress is poised to select new leaders to run the party and state for the next decade. Such a selection process reveals factional rifts within the party. One important such rift is between those who favor further reform and those who yearn for the glorious revolutionary days of Mao.

The World Bank and the Development Research Center, an influential Chinese government think tank, jointly submitted its “China 2030” report recommending new reforms.28 They propose that China scale back the state economy, suggesting that the state limit itself to policy making and oversight and not intervene in the affairs of state enterprises. State-owned companies should be run by professional asset managers and should be privatized and broken up if they hold monopoly power. The “China 2030” report warns that powerful domestic interests will oppose reform, but implementation of the reforms will provide vital improvements in economic performance.

The CPC is, therefore, at a crossroads. To date, it has played the “leading role” in politics, economics, and civic life. If people are allowed to make their own decisions in relatively free markets, the CPC will lose much of its leading role. The control of economic resources is what gives party leaders power and personal wealth. An authority on Chinese finance characterizes credit markets as a “bountiful source of political resources…. [T]he enormous pool of savings in the banking sector made it an indispensible policy and political instrument.”29

For more on the topics in this article, check out the EconTalk podcasts Ron Coase on Coase on Externalities, the Firm, and the State of Economics and Dani Rodrik on Globalization, Development, and Employment.

The CPC must decide whether it wants control or economic performance. Economic growth, emanating largely from the private economy, has allowed the CPC to delay this decision. How it decides will affect political and economic performance for the coming decades. As the Economist writes: “China is often held up as an object lesson in state-directed capitalism. Yet its economic dynamism owes much to those outside the government’s embrace.”30

The remarkable feature of China is that despite the private sector’s disadvantages in credit markets, it has advanced and outgrown the privileged state sector. Perhaps, one day, we will see what it can accomplish on a level playing field.

Thomas Friedman, “Our One-Party Democracy,”New York Times, September 8, 2009.

F. A. Hayek, “The Use of Knowledge in Society,”American Economic Review, 35, no. 4 (September 1945), 519-30.

Robert Heilbroner, “Socialism,” in David R. Henderson, ed., The Concise Encyclopedia of Economics. Indianapolis: Liberty Fund, 2008.

All quotes in this paragraph are from “China ‘Best Served’ With CPC at the Helm,”. China Daily, June 6, 2011 (Interview with Robert Lawrence Kuhn).

Michael Spence, The Next convergence: the Future of Economic Growth in a Multispeed World (New York: Farrar, Straus and Giroux, 2011).

Eric Maskin, Yingyi Qian, and Chenggang Xu (2000), “Incentives, Information, and Organizational Form.” Review of Economic Studies, April 2000, 67(2), pp. 359-78.

Chenggang Xu, “The Fundamental Institutions of China’s Reforms and Development,” Journal of Economic Literature 2011, 49:4, 1076-1151

Barry Naughton, and Dali L. Yang (eds.), Holding China Together: Diversity and National Integration in the Post-Deng Era (New York: Cambridge University Press, 2004).

“China’s Railway Minister Loses Post in Corruption Inquiry.”New York Times, February 12, 2011.

Russell Flannery, “The 400 Richest Chinese.”Forbes, September 13, 2011.

“Brother of Fallen Chinese Politician Resigns Lucrative Business Role,”New York Times, April 25, 2012.

Transparency International, Corruption Perceptions Index.

Heritage Foundation, Economic Freedom Index.

Bao Tong, “A Pivotal Moment For China,” Radio Free Asia, December 29, 2008.

Kate Zhou, How the Farmers Changed China: Power of the People (Boulder, CO: Westview Press, 1996).

Paul Gregory and Kate Zhou, “How China Won and Russia Lost: Two Dissimilar Economic Paths,” Policy Review, No. 158, December 1, 2009.

This is a term that venture capitalists use to refer to three types of early investors.

“We Are the Champions,” The Economist, March 18, 2004.

Andrew Szamosszegi and Cole Kyle, “An Analysis of State-owned Enterprises and State Capitalism in China,” U.S.-China Economic and Security Review Commission, October 26, 2011. PDF file.

“Private enterprises expanding quickly,”People’s Daily Online, February 04, 2005.

Statistical Yearbook of China (English edition). 2011.

Szamosszegi and Kyle, 123.

“Entrepreneurship in China: Let a million flowers bloom,” The Economist, March 10, 2011.

Qiao Liu and Alan Siu, “Institutions, Financial Development, and Corporate Investment: Evidence from an Implied Return on Capital in China,” Hong Kong Institute of Economics and Business Strategy, December 2006

Patrick Chonanec, “China State Enterprises Advance, Private Sector Retreats,”Forbes.com, August 31, 2010

Michael Wines, “China Fortifies State Businesses to Fuel Growth,” New York Times, August 29, 2010.

“When Fund Raising is a Crime,” Economist, April 16, 2011, 69.

Bob Davis, “Blueprint of China Reforms: Leaves Role of Party Vague,” Wall Street Journal, February 28, 2012.

Victor Shih, Factions and Finance in China (New York: Cambridge University Press, 2008), 191

“Entrepreneurship in China: Let a million flowers bloom,” The Economist, March 10, 2011.

*Paul Gregory is a Research fellow at the Hoover Institution, Stanford, and the Cullen Professor of Economics at the University of Houston. His latest book is a non-fiction political thriller entitled Politics, Murder, and Love in Stalin’s Kremlin: The Story of Nikolai Bukharin and Anna Larina.

For more articles by Paul Gregory, see the Archive.