Carbon Taxes and the "Tax Interaction Effect"

By Robert P. Murphy

“Introducing a new carbon tax amplifies the distortions caused by the pre-existing taxes, so that the original tax (even at a lower rate than previously) in conjunction with the new carbon tax leads to more total tax distortion in the economy.”

For years, many economists have advocated a tax on the emission of carbon dioxide and other greenhouse gases as a way to correct the negative externality of manmade climate change. More recently, even a growing number of conservative economists have embraced a carbon tax, not only as a way to correctly align market forces, but also as a way to offset other, more distortionary taxes. The slogan underlying such “carbon tax swap” proposals is that the government should “tax bads, not goods.”

Although the thinking underlying the conservative case is correct, there is a potential downside from a carbon tax swap. This negative side effect is rarely mentioned in any but the most technical discussions. It is the “tax interaction effect.” A new carbon tax can exacerbate the harms caused by pre-existing taxes, thereby offsetting the potential environmental benefits. What’s worse, not only can the tax-interaction effect operate in theory, but also numerical simulations suggest that it might be very large in practice, greatly reducing the “optimal” carbon tax.

The Conservative Case for a Carbon Tax Swap

Perhaps the best summary of the conservative case for a carbon tax swap comes from the 2008 New York Times op-ed by famous supply-side economist Arthur Laffer and South Carolina Republican representative Bob Inglis. They write:

We need to impose a tax on the thing we want less of (carbon dioxide) and reduce taxes on the things we want more of (income and jobs). A carbon tax would attach the national security and environmental costs to carbon-based fuels like oil, causing the market to recognize the price of these negative externalities….

Conservatives do not have to agree that humans are causing climate change to recognize a sensible energy solution. All we need to assume is that burning less fossil fuels would be a good thing….

Yet the costs of reducing carbon emissions are not trivial…. It is essential, therefore, that any taxes on carbon emissions be accompanied by equal, pro-growth tax cuts…. Fiscal conservatives would gladly trade a carbon tax for a reduction in payroll or income taxes, but we can’t go along with an overall tax increase.1

Although the intuition in the above arguments is correct, Laffer and Inglis’s analysis omits an important consideration: Just about every public discussion of carbon tax swaps implicitly assumes that the distortions emanating from the tax code must decrease if the government begins taxing a negative externality (carbon emissions) and uses the revenue to reduce tax rates on productive activity. However, the analysis of the tax interaction effect shows that this assumption may be wrong.

The Tax-Interaction Effect

Two pioneers in this area are A. Lans Bovenberg and Lawrence H. Goulder, whose 1996 article in the American Economic Review showed the theoretical possibility, and estimated magnitude, of the tax-interaction effect.2 Whereas the discussion in that paper is technical, Goulder has a more readable discussion of his work in this area in a 2000 NBER Reporter piece.3 There, he writes:

Are the costs of the green tax negative? Over the last decade, many researchers have addressed this question. The simplest analytical models suggest that the answer is no. These models point out that green taxes usually are a relatively inefficient way to raise revenue: the economic cost of raising a dollar through green taxes tends to be higher than that of raising a dollar through ordinary income taxes. Intuitively, that is because green taxes have a much narrower base than income taxes. They focus on individual commodities (such as fossil fuels) or on emissions from particular industries. As a result, they tend to imply larger “distortions” in markets for intermediate inputs, for consumer goods, and for labor and capital. Hence, swapping a green tax for part of the income tax augments the (nonenvironmental) distortions of the tax system, and there is an economic cost of this revenue-neutral tax reform. [emphasis added.]

Although, in this piece, Goulder verbally explains his result—namely, that carbon taxes are not “consumption taxes,” as is sometimes asserted, and that they have a smaller tax base than other taxes on production—I urge professional economists to read Bovenberg and Goulder’s technical paper. The problem is not simply that a carbon tax imposes gross harms to the economy; after all, these should be more than offset by the benefits of avoided climate-change damages, according to the standard argument for taxing negative externalities. Rather, what’s really happening is that introducing a new carbon tax amplifies the distortions caused by the pre-existing taxes, so that the original tax (even at a lower rate than previously) in conjunction with the new carbon tax leads to more total tax distortion in the economy. This is why the phenomenon is called the “tax-interaction effect” and why economists must apply their textbook externality arguments cautiously.

Walking Through the Logic of a Carbon Tax Swap

When first encountering the possibility of the tax-interaction effect, the reader may have trouble understanding where, precisely, the standard arguments for a carbon tax swap go awry. To repeat, the claim is not that the intuition behind these proposals is wrong, but that it overlooks a crucial consideration. An easy way to illustrate the danger is to work our way through three different scenarios, building up to the situation we actually face. For the sake of argument, we shall assume throughout this discussion that the “social cost of carbon”—the present discounted value of future climate-change damages—is $50/ton. (This is a round number that’s somewhat higher than what many economists would estimate as the social cost of carbon over the next decade.4)

Scenario #1: Perfectly Efficient Market Except for Carbon Externality

In the first scenario, we assume that the only distortion to the market is the carbon externality. In this case, implementing a tax on carbon of $50/ton, with the revenues then mailed back to all citizens in equal checks, would be an optimal, “first best” government policy. It’s true that the new carbon tax would impose gross costs on the economy: Gasoline and electricity would be more expensive, hurting poorer consumers, and the owners of coal mines and oil wells would probably be worse off on net. However, the benefits of avoided future climate-change damages would more than offset these gross costs, so that the winners from this tax would, in theory, be able to more than compensate the losers. The sloppy language that economists often use to describe such a situation is “society as a whole would gain.”

Scenario #2: Pre-Existing Yet Modest Income Tax as Well as Carbon Externality

In the second scenario, we assume that, initially, there is an income tax that raises a small amount of revenue, and does so in an inefficient manner. In other words, there is “deadweight loss” associated with the income tax—it costs society more than $1 in order for the government to raise $1 of tax revenue. In addition, we continue to assume that there is a carbon externality of $50/ton.

Suppose that the government imposes the same carbon tax of $50/ton, but now it uses some of the revenue to eliminate the income tax, with any excess being mailed back to citizens in equal per-capita checks. The net benefits of the carbon tax in this scenario are even higher than in the first because now, in addition to the environmental benefits from reduced carbon emissions (which we already know are high enough to offset the gross costs of the carbon tax itself), we have eliminated the deadweight loss from the original income tax. If the carbon tax is a good idea in Scenario #1, then it is an even better idea in Scenario #2.

Scenario #3: Pre-Existing and Large Income Tax as Well as Carbon Externality

Finally, the third scenario characterizes the real world. Here, we assume that the government imposes a $50/ton carbon tax, but that the revenues it raises can only partially reduce the pre-existing tax rates on income. Most economists in public discussions of such policies seem to believe that the analysis here is the same as in Scenario #2.

Yet since Scenario #3 leaves us with an income tax and the new carbon tax, operating side by side, we have to consider the tax-interaction effect. Is it possible that the total distortion to the economy, caused by the combination of the income tax (albeit at lower marginal rates) and the new carbon tax, is higher than the original deadweight loss due to the income tax alone (albeit at its higher, original marginal rates)?

The answer is a resounding yes: It is definitely possible for the total tax distortions to increase. To be fair, some models do show the opposite result, but (as Goulder suggested in the quotation above) the straightforward result is that a revenue-neutral carbon tax will increase the total distortions to the economy caused by the tax code.

The precise reasons for the extra deadweight loss depend on the particular model, and ultimately it is hard to point to a “cause” in a comparison of two different general equilibrium outcomes. Even so, Goulder in his 2000 summary article gives this explanation:

[T]o the extent that environmental taxes raise producers’ costs, they imply higher prices of commodities. This effectively reduces the real returns to factors—a given nominal wage payment or given nominal distribution of profits has less purchasing power. When there are pre-existing taxes on these factors, the environmental tax functions like an increase in factor taxes, compounding the distortions in factor markets from prior taxes. This adverse impact on factor markets is the tax-interaction effect.

Thus we see the subtlety of the tax-interaction effect: The rearrangement in factor prices due to a new carbon tax—which would be welfare-enhancing if there were no taxes originally, because the change in factor prices would properly reflect the negative externality—can actually exacerbate the distortions caused by pre-existing taxes on factors of production. Rather than shifting the tax burden away from producers and onto pollution, a new carbon tax, even if revenue-neutral, could end up increasing the tax burden on carbon emitters and on generic production.

It is important to note that the tax-interaction effect does not necessarily negate the case for a carbon tax. However, on the margin, the carbon tax would be less desirable compared to a situation with no tax-interaction effect. What this means in practice is that the $50/ton carbon tax would no longer be optimal, but, instead, a smaller carbon tax would be a more efficient policy response.

The Magnitude of the Tax-Interaction Effect

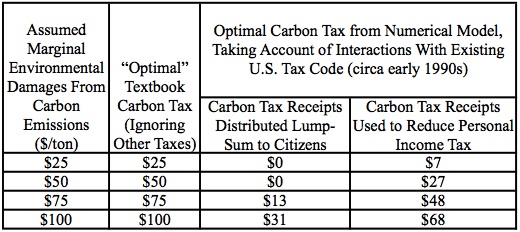

To get an idea of just how important the tax-interaction effect could be, consider Table 1, adapted from Bovenberg and Goulder’s original paper. They estimate a fairly complex numerical model involving the petroleum sector, as well as the structure of the U.S. tax code. They find that once tax-interaction effects are considered, the case for a carbon tax is considerably reduced.

Table 1. Textbook Carbon Tax versus Optimal Carbon Tax, in Presence of Tax Code Distortions ($/ton)

The results in Table 1 are striking. For example, assuming a $50/ton “social cost of carbon,” the textbook response is for the government to levy a $50/ton tax on carbon. Yet once the tax-interaction effect is taken into account, if those carbon tax receipts were distributed back to citizens in equal per-capita checks, then the revised optimal carbon tax would be $0. In other words, a carbon tax at any level would increase total tax distortions so much that the environmental benefits would not be able to compensate. The government, by imposing any carbon tax, would make society worse off.

Yet even if the carbon tax receipts are used to offset personal income taxes, the optimal carbon tax is still only $27/ton. Thus, the logic of the carbon tax swap proponents is correct: The case for a carbon tax becomes stronger if its receipts are used to reduce pre-existing, distortionary taxes. However, this true statement does not mean that the prior existence of distortionary taxes makes the case for a carbon tax stronger. In fact, it probably weakens the case for a carbon tax. In terms of the numbers we have been discussing from Table 1, the typical proponent of a carbon tax swap would likely focus on the fact that $27 is higher than $0, rather than the equally important fact that $27 is lower than $50.

Conclusion

For more on this topic, see also The Economics of Climate Change, by Robert P. Murphy. Library of Economics and Liberty, July 6, 2009.

Proponents of a carbon tax swap deal are right when they claim that the gross harms of a new carbon tax can be partially offset if its receipts are used to reduce other taxes. However, they typically leap from this true claim to the unjustified conclusion that a revenue-neutral carbon tax will be a “win-win” for the economy—by reducing distortions from the tax code as well as providing environmental benefits. On the contrary, it is theoretically possible and empirically likely that a revenue-neutral carbon tax will impose more deadweight loss on the economy, offsetting at least some of the potential environmental benefits. A carbon tax may still be a good policy, but its proponents should first understand the tax-interaction effect before making their case and choosing the tax level.

Inglis, Bob and Arthur Laffer. (2008) “An Emissions Plan Conservatives Could Warm To.” New York Times, December 28, 2008, available at: http://www.nytimes.com/2008/12/28/opinion/28inglis.html.

Bovenberg, A. Lans and Lawrence H. Goulder. (1996) “Optimal Environmental Taxation in the Presence of Other Taxes: General Equilibrium Analyses.” American Economic Review 86: 985-1000. A 1994 NBER Working Paper No. 4897 version of their article is available at: http://www.nber.org/papers/w4897.

Goulder, Lawrence H. (2000) “Economic Impacts of Environmental Policies.” NBER Reporter, Spring 2000, available at: http://www.nber.org/reporter/spring00/goulder.html.

For example, as I discuss in my 2009 article in the Independent Review, “Rolling the DICE: William Nordhaus’ Dubious Case for a Carbon Tax” (vol. 14, no. 2), expert Nordhaus’s model (as of 2007) estimated that the social cost of carbon in 2015 would be $42, and, by 2025, would have risen to $53. My article is available at: http://www.independent.org/pdf/tir/tir_14_02_03_murphy.pdf.