Insider Trading Turned Inside Out

By Charles L. Hooper

“The insider mitigates the effects of the stock market lottery.”

Unfortunately, the case for prosecuting insider trading has some fatal flaws. First, approximately 83 percent of the possible insider trading scenarios can never be prosecuted. Second, luck is involved and a legal system should not be based on luck. Third, insiders will always have information that the rest of us don’t have—it’s just a fact of life, and sometimes a fortunate one at that. Fourth, insider trading cannot harm regular investors as a whole. Fifth, insider trading has some beneficial characteristics. Sixth, the relatively recent prohibition on insider trading has no basis in common law and, in fact, could be handled outside of the government. Seventh, the prohibition on insider trading is expensive and ineffective.

Although the SEC website provides examples of the practice,2 neither the SEC nor legislators have ever even defined insider trading. Insider trading is often interpreted as acting on inside information, that is “knowledge of specific events or of the probability of future events that will ultimately cause a change in share prices.”3 The relatively recent prohibition on insider trading started slowly after the Great Depression and has mushroomed since the early 1980s. The SEC claims that it has prosecuted such cases because they have “undermined the level playing field that is fundamental to the integrity and fair functioning of the capital markets.”4

The following example illustrates why insider trading laws are seriously flawed.

Two decades ago I was an “insider” at an up-and-coming biotechnology company, Gilead Sciences. Never before had this company’s entire portfolio been forecasted systematically. And yet, as a consultant to Gilead, I had all the 20-year forecasts right in front of me. At that moment, I knew more about this company’s prospects than any investor and, in fact, than the CEO who sat in his office down the hall. I was the quintessential insider.

I was also confused, faced with so many unanswered questions—the major one being: How good was my insider information?

What I had were forecasts. Did we do a good job understanding the current markets, the veracity of epidemiological data, the true merits of the company’s new medicines, the nuances of the clinical trial data, the potential threats from better products launching, or even the FDA’s likelihood of approving the company’s drugs, provided that they survived the clinical trials process? Would a few adverse events sink this company’s top products? Would the CEO stumble or leave for greener pastures? Would the company sell to a larger company at a fraction of its true value? Could this young company execute?

There was another problem: Wall Street was expecting Gilead to grow, and that expectation was built into the stock’s price. Gilead would be a good “insider” purchase only if it would make more money than other investors were anticipating. Even with all the forecasts in front of me, I was not certain that this company would do better than the market expected. At most, this information would increase my odds. But I also knew that a jury would see it differently if I violated my blackout period and traded. If I made money, a jury would use 20-20 hindsight to see how I had benefited from insider information and traded for a profit.

Decisions are forward-looking and good decisions do not always produce good outcomes. As David R. Henderson and I wrote in our book, Making Great Decisions in Business and Life,5 a good decision is the one you’d make the next time, given the same information, not the decision that happened to give a good outcome this particular time. Insider trading laws are intended to punish bad decisions, but what they really punish are good outcomes. If you trade and benefit, that “proves” that you had inside knowledge. If you trade and lose, you are left alone with your losses.

Changes in stock market prices are a maddeningly random walk, subject to luck. A company can announce good earnings and have its share price fall. Another company can announce good earnings and have its share price rise. Why? Even the sage Warren Buffett is perplexed by this: “Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month—or a year—from now.”6 Insider trading prosecutions rely on that market fickleness, and it is not prudent to base a legal system on luck.

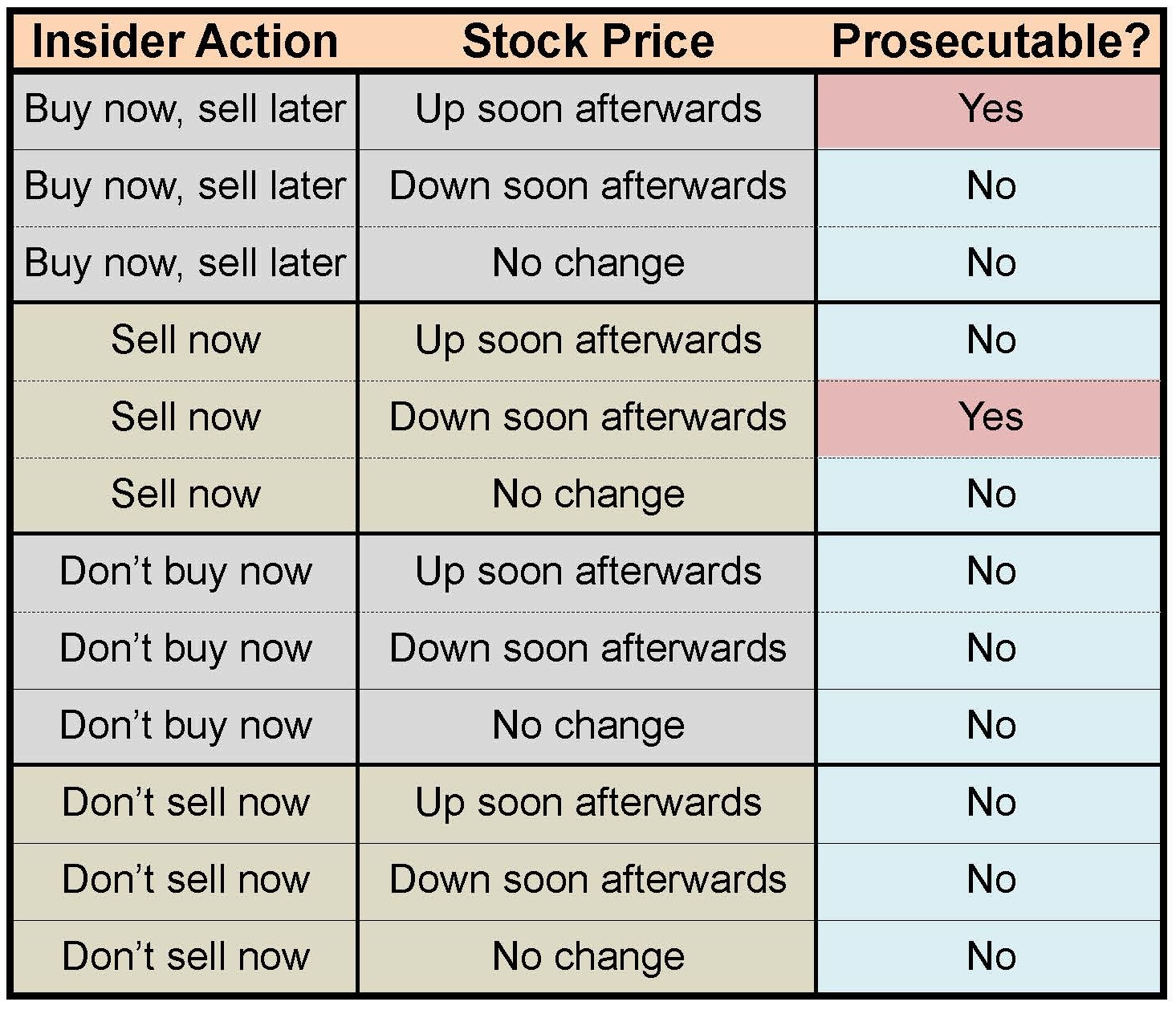

It is startling to note that at least five-sixths of all insider trading scenarios (it would be practically impossible to measure actual cases) could never be prosecuted, even with a policeman shadowing each and every insider. Why? Consider how inside information can affect the behavior of an insider. He or she can think the stock will appreciate and buy shares or think the stock will decline and sell shares. The insider can also decide not to sell or buy shares. Next, after this action or inaction, the share price can rise, fall, or stay the same. Even if the price rises or falls, it may match the market as a whole, complicating the picture.

There are twelve possible scenarios and only two of them can be prosecuted, as shown in Figure 1.

Figure 1. Prosecution Table

Insiders have different, and usually better, information than the rest of us. A pervasive myth is that it is both possible and beneficial to endow all market participants with the same level and depth of information to create a so-called “level playing field.” But it is impossible for all people to have the same information. Indeed, Friedrich Hayek, who won the Nobel prize in economics in 1974, pointed out that each person has information about his or her own circumstances and that one main reason the free market works so well is that it allows us to act on that information. This information, in short, is decentralized among billions of participants. Economists call this decentralized information “local knowledge.” In his famous 1945 article, “The Use of Knowledge in Society,” Hayek wrote, “[P]ractically every individual has some advantage over all others because he possesses unique information of which beneficial use might be made, but of which use can be made only if the decisions depending on it are left to him or are made with his active cooperation.”7

The legendary Magellan fund manager, Peter Lynch, agreed and held as his first investment principle: Invest in what you know.8 He advocated acting on our unique local knowledge. Investing this way clearly benefited Lynch and Magellan investors. Did it harm other investors? There were some who sold when Lynch was buying. They missed out on the “next big thing,” but they were happy to sell. Those who bought when Lynch was selling were happy to buy. It would be hard to argue that Lynch harmed anyone given that everyone acted voluntarily and no one purposely misled anyone.

Does insider trading hurt other traders? Actually, no. To see why, first consider the case without an insider trading. Investors happily buy and sell shares in a company at a certain price, say $100 per share. Later, when information—such as an earnings report—becomes public and the price jumps to $110, those who bought at $100 look back and consider themselves lucky and those who sold at $100 bemoan their unlucky move. Both groups could have avoided this “lottery” by waiting to act until after the earnings report, by buying shares in a mutual fund instead, or by keeping their money safely in the bank. They voluntarily “played the market.”

Investors accept the vicissitudes of the stock market; there is no one to blame. The insider who trades does not create this lottery nor does he or she exacerbate the lottery; the insider mitigates the effects of the stock market lottery.

Consider the case where an insider trades ahead of a public news release. Before the insider buys, investors happily buy and sell at $100 per share. After the insider buys, investors happily buy and sell at the new higher price, say $101. When the news finally becomes public, the lucky ones realize they made $9 per share and the unlucky ones lost $9. The gains and losses were $9 per share instead of $10 without the insider.

The insider did not create the lottery and did not cause anyone to make or lose money. The insider merely took the existing lottery and reduced the magnitude of the losses and gains to the other participants. Those who blame the insider for causing some to lose money ignore two important points: (1) there are those who gain and their gains exactly offset the losses suffered by others; (2) people would have made more or lost more had the insider not acted. In effect, those who blame the insider find fault in the fact that the insider didn’t do more to dampen the stock market lottery. To be consistent, they should blame the insider for not shouting the information from rooftops.

For more on this topic, see “Insider Trading,” by David R. Henderson. EconLog, November 18, 2008.

One legitimate complaint against insider trading is the harm it does to “specialists” who charge a “bid-ask spread” and “make a market” for selected securities. Because specialists will buy even if there are no other willing buyers, “specialists will insist on larger bid-ask spreads if insider trading is widespread.”9 That bid-ask spread is a trading cost to investors. However, even though this complaint is theoretically sound, “econometric attempts to find a relationship between the bid-ask spread and the risk of insider trading have been inconsistent and unreliable.”10

Everyone, even specialists, benefits from insider trading in another way. One purpose of the stock market is to quickly disseminate information about companies. An insider selling on bad news causes a stock to drop a little sooner. That’s good, especially if the company, like Enron, is involved in shady dealings. All inside information will come out eventually, or else insiders wouldn’t trade on it, so we can think of insiders as whistleblowers, leaking news and alerting the outside world to the good or bad things happening behind the walls of Corporate America.

If insider trading is a problem, then corporations themselves should oppose it because such disclosures of “inside information” could release proprietary information and affect executives’ compensation. Companies already have it within their power to control such disclosures through contracts with employees—through the common law. Companies can enact their own prohibitions against insider trading, but, as it turns out, few have. Indeed, in the famous Texas Gulf Sulphur case that kicked off the modern insider trading era, the offending party, Charles Fogarty, was later promoted to chief executive officer. Clearly, the board of directors did not consider Fogarty’s actions to have harmed the company. If companies don’t care, the government should care far less.

In addition to the corporations themselves, stock exchanges could deal with insider trading. Such efforts would be perfectly legal and would not involve the government. “The case for having public regulation of insider trading must, therefore, rest on such factors as inefficiency of private enforcement or insider trading’s overall adverse impact on securities markets.”11

Corporate law scholar Henry Manne made a strong case in his 1966 book, Insider Trading and the Stock Market, that insider trading, as distasteful as it is to some, is beneficial overall. He argued that neither precedent nor reason supports the view that insider trading is harmful and should be prohibited, except in the case of government officials who could profit from inside information of contracts, regulations, and lawsuits. In 2014, he claimed, “Insider trading not only does no harm, it can have significant social and economic benefits including a more accurate pricing of stocks.”12

The free market succeeds by moving resources to their highest-value use and provides prices as a complementary byproduct. Shares in publicly traded companies behave the same, and stock prices are the byproduct.

How is insider trading on securities any different from other transactions with asymmetrical information? The cattle buyer might have better information—not publicly known—about what packers would pay. The rancher might have better information—not publicly known—about the health of the herd. To prosecute one or the other would be almost impossible. “It also should be noted that transactions based on unequally distributed information are common and often legal in labor, commodities, and real estate markets, to name a few.”13

Prohibitions on insider trading clearly benefit government agencies by providing a ready source of power and money. For the rest of us, these prohibitions are costly. Taxpayers pay the salaries of prosecutors like Preet Bharara—and for his wiretaps, investigations, lawsuits, etc. If people are convicted, even though they are nonviolent, they may spend time in jail and be unable to continue working, earning, and paying taxes. Many people, even if they are not true insiders, do not trade because they fear prosecution. That fear is a real cost, as it puts a damper on their portfolios and spills over into the larger stock market, where shares are not priced based on the best information. Consequently, the market operates below peak efficiency. Also, corporations must train and monitor their employees to avoid running afoul of insider-trading laws. There is also a cost to our privacy. All of these costs are substantial.

While economists try to empirically measure the net effect of insider trading regulations, insider trading is clearly not the bogeyman that many believe it to be, as evidenced by well-functioning markets in which insider trading cases cannot be or simply are not prosecuted. “[T]he effectiveness of the insider trading prohibition and the commitment to enforcing it have been low in most countries.”14 Even in this country, the SEC has flagged only a small percentage of insider trading instances, yet the markets function well.

Henry Manne pointed out the ultimate futility of the government’s attempts: “There is about as much chance of stopping trading on undisclosed financial information as there ever was of stopping the consumption of booze [during Prohibition].”15

Peter Lattman, “The Bruce-Bharara Bromance,”The New York Times, 1 November 2012.

U.S. Securities and Exchange Commission, SEC Enforcement Actions, Insider Trading Cases.

Henry G. Manne, Insider Trading and the Stock Market, The Free Press, New York, 1966.

U.S. Securities and Exchange Commission, SEC Enforcement Actions, Insider Trading Cases.

Making Great Decisions in Business and Life, by David R. Henderson and Charles L. Hooper.

Wikiquote, Talk: Warren Buffett.

Friedrich A. Hayek, “The Use of Knowledge in Society,” III, H.9, AER, 1945. Library of Economics and Liberty.

“Stock Superstar Who Beat the Street,” Wharton, University of Pennsylvania, Peter S. Lynch, WG ’68.

David D. Haddock, “Insider Trading,”The Concise Encyclopedia of Economics, 1st Edition.

Stanislav Dolgopolov, “Insider Trading,”The Concise Encyclopedia of Economics, 2nd Edition.

Dolgopolov, “Insider Trading.”

Henry G. Manne, The Wall Street Journal, “Busting Insider Trading: As Pointless as Prohibition,” 28 April 2014.

Dolgopolov, “Insider Trading.”

Dolgopolov, “Insider Trading.”

Henry G. Manne, The Wall Street Journal, “Busting Insider Trading: As Pointless as Prohibition,” 28 April 2014.