Bonds

By Clifford W. Smith

Bond markets are important components of capital markets. Bonds are fixed-income financial assets—essentially IOUs that promise the holder a specified set of payments. The value of a bond, like the value of any other asset, is the present value of the income stream one expects to receive from holding the bond. This has several implications:

1- Bond prices vary inversely with market interest rates. Because the stream of promised payments usually is fixed no matter what subsequently happens to interest rates, higher rates reduce the present value of these promised payments, and thus the bond price.

2- The value of bonds falls when people come to expect higher inflation. The reason is that higher expected inflation raises market interest rates, and therefore reduces the present value of the fixed stream of promised payments.

3- The greater the uncertainty about whether the promised payments will be made (the risk that the issuer will default on the promised payments), the lower the expected payments to bondholders and the lower the value of the bond.

4- Bonds whose payments are subjected to lower taxation provide investors with higher expected after-tax payments. Because investors are interested in after-tax income, such bonds sell for higher prices.

The major classes of bond issuers are the U.S. government, corporations, and municipal governments. The default risk and tax status differ from one kind of bond to another.

U.S. Government Bonds

The U.S. government is highly unlikely to default on promised payments to its bondholders because the government has the right to tax as well as the authority to print money. Thus, virtually all of the variation in the value of its bonds is due to changes in market interest rates. That is why most securities analysts use prices of U.S. government bonds to compute market interest rates.

Because the U.S. government’s tax revenues rarely cover expenditures, it relies on debt financing for the balance. Moreover, on the occasions when the government does not have a budget deficit, it still sells new debt to refinance the old debt as it matures. Most of the debt sold by the U.S. government is marketable, meaning that it can be resold by its original purchaser. Marketable issues include treasury bills, treasury notes, and treasury bonds. The major nonmarketable federal debt sold to individuals is U.S. savings bonds.

Treasury bills have maturities of up to one year and are generally issued in denominations of $10,000. They do not have a stated coupon; that is, the government does not write a separate interest check to the owner. Instead, the U.S. Treasury sells these bills at a discount to their redemption value. The size of the discount determines the effective interest rate on the bill. For instance, a dealer might offer a bill with 120 days left until maturity at a yield of 7.48 percent. To translate this quoted yield into the price, one must “undo” this discount computation. Multiply the 7.48 by 120/360 (the fraction of the conventional 360-day year employed in this market) to obtain 2.493, and subtract that from 100 to get 97.506. The dealer is offering to sell the bond for $97.507 per $100 of face value.

Treasury notes and treasury bonds differ from treasury bills in several ways. First, their maturities generally are greater than one year. Notes have maturities of one to seven years, while bonds can be sold with any maturity, but their maturities at issue typically exceed five years. Second, bonds and notes specify periodic interest (coupon) payments as well as a principal repayment. Third, they normally are registered, meaning that the government records the name and address of the current owner. When treasury notes or bonds are sold initially, their coupon rate is typically set so that they will sell at close to their face (par) value.

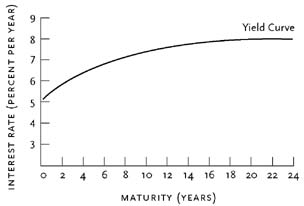

Yields on bills, notes, or bonds of different maturities usually differ. (The array of rates associated with bonds of different maturities is referred to as the term structure of interest rates.) Because investors can invest either in a long-term note or in a sequence of short-term bills, expectations about future short-term rates affect current long-term rates. Thus, if the market expects future short-term rates to exceed current short-term rates, then current long-term rates would exceed current short-term rates—the term structure would have a positive slope (see Figure 1).

If, for example, the current short-term rate for a one-year T-bill is 5 percent, and the market expects the rate on a one-year T-bill sold one year from now to be 6 percent, then the current two-year rate must exceed 5 percent. If it did not, investors would expect to do better by buying one-year bills today and rolling them over into new one-year bills a year from now.

Savings bonds are offered only to individuals. Two types have been offered, both registered. Series E bonds are essentially discount bonds; investors receive no interest until the bonds are redeemed. Series H bonds pay interest semiannually. Unlike marketable government bonds, which have fixed interest rates, rates received by savings bond holders normally are revised when market rates change. Some bonds—for instance, U.S. Treasury Inflation-Protected Securities (TIPS)—are indexed for inflation. If, for example, inflation were 10 percent per year, then the value of the bond would be adjusted to compensate for this inflation. If indexation were perfect, the change in expected payments due to inflation would exactly offset the inflation-caused change in market interest rates.

Corporate Bonds

Corporate bonds promise specified payments at specified dates. In general, the interest the bondholder receives is taxed as ordinary income. An issue of corporate bonds generally is covered by a trust indenture, a contract that promises a trustee (typically a bank or trust company) that it will comply with the indenture’s provisions (or covenants). These include a promise of payment of principal and interest at stated dates, as well as other provisions such as limitations of the firm’s right to sell pledged property, limitations on future financing activities, and limitations on dividend payments.

Potential lenders forecast the likelihood of default on a bond and require higher promised interest rates for higher forecasted default rates. (This difference in promised interest rates between low- and high-risk bonds of the same maturity is called a credit spread.) Bond-rating agencies (Moody’s and Standard and Poor’s, for example) provide an indication of the relative default risk of bonds with ratings that range from Aaa (the best quality) to C (the lowest). Bonds rated Baa and above typically are referred to as “investment grade.” Below-investment-grade bonds are sometimes referred to as “junk bonds.” Junk bonds can carry promised yields that are three to six percentage points higher than those of Aaa bonds. They have a credit spread of three hundred to six hundred basis points, a basis point being one one-hundredth of a percentage point.

One way that corporate borrowers can influence the forecasted default rate is to agree to restrictive provisions or covenants that limit the firm’s future financing, dividend, and investment activities—making it more certain that cash will be available to pay interest and principal. With a lower anticipated probability of default, buyers are willing to offer higher prices for the bonds. Corporate officers, thus, must weigh the costs of the reduced flexibility from including the covenants against the benefits of lower interest rates.

Describing all the types of corporate bonds that have been issued would be difficult. Sometimes different names are employed to describe the same type of bond, and, infrequently, the same name will be applied to two quite different bonds. Standard types include the following:

•Mortgage bonds are secured by the pledge of specific property. If default occurs, the bondholders are entitled to sell the pledged property to satisfy their claims. If the sale proceeds are insufficient to cover their claims, they have an unsecured claim on the corporation’s other assets.

•Debentures are unsecured general obligations of the issuing corporation. The indenture will regularly limit issuance of additional secured and unsecured debt.

•Collateral trust bonds are backed by other securities (typically held by a trustee). Such bonds are frequently issued by a parent corporation pledging securities owned by a subsidiary.

•Equipment obligations (or equipment trust certificates) are backed by specific pieces of equipment (railroad rolling stock, aircraft, etc.).

•Subordinated debentures have a lower priority in bankruptcy than ordinary (unsubordinated) debentures. Junior claims are generally paid only after senior claims have been satisfied but rank ahead of preferred and common stock.

•Convertible bonds give the owner the option either to be repaid in cash or to exchange the bonds for a specified number of shares in the corporation.

Municipal Bonds

Historically, interest paid on bonds issued by state and local governments has been exempt from federal income taxes. Such interest may be exempt from state income taxes as well. For instance, the New York tax code exempts interest from bonds issued by New York and Puerto Rico municipalities. Because investors are interested in returns net of tax, municipal bonds generally have promised lower interest rates than other government bonds that have similar risk but that lack this attractive tax treatment. In 2003, the percentage difference (not the percentage point difference) between the yield on long-term U.S. government bonds and the yield on long-term municipals was about 10 percent. Thus, if an individual’s marginal tax rate were higher than 10 percent, the after-tax promised return would be higher from municipal bonds than from taxable government bonds. (Although this difference might appear small, there is a credit spread in municipals just as in corporates.)

Municipal bonds typically are designated as either general obligation bonds or revenue bonds. General obligation bonds are backed by the “full faith and credit” (and thus the taxing authority) of the issuing entity. Revenue bonds are backed by a specifically designated revenue stream, such as the revenues from a designated project, authority, or agency, or by the proceeds from a specific tax.

Frequently, such bonds are issued by agencies that plan to sell their services at prices that cover their expenses, including the promised payments on the debt. In such cases, the bonds are only as good as the enterprise that backs them. In 1983, for example, the Washington Public Power Supply System (WPPSS), which Wall Street quickly nicknamed “Whoops,” defaulted on $2.25 billion on its number four and number five nuclear power plants, leaving bondholders with much less than they had been promised. Industrial development bonds are used to finance the purchase or construction of facilities to be leased to private firms. Municipalities have used such bonds to subsidize businesses choosing to locate in their area by, in effect, giving them the benefit of loans at tax-exempt rates.

Some municipal bonds are still sold in bearer form; that is, possession of the bond itself constitutes proof of ownership. Historically in the United States, most public bonds (government, corporate, and municipal) were bearer bonds. Now, the Internal Revenue Service requires bonds that pay taxable interest to be sold in registered form.

Further Reading

Related Links

Robert P. Murphy, Government Debt and Future Generations. June 2015.

From the Web: