Karl Smith of Modeled Behavior has moved to DC, and yesterday he honored the GMU lunch with what will hopefully be the first of many visits. During lunch, I asked Karl about a puzzling-to-me line from his latest post:

Social Security never was that big of deal. Lots of people get this and I’ll just refer you to them.

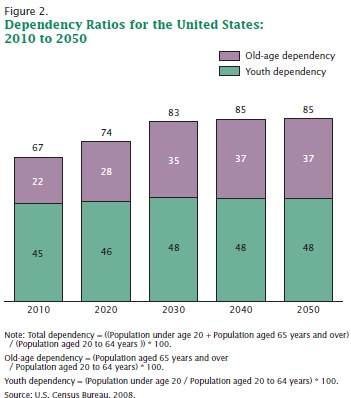

The issue, of course, is not whether the government can make Social Security solvent: lower benefits, higher taxes, or means-testing would all do the trick. The issue, rather, is how big these adjustments would have to be. And that, in turn, depends on how much the Aged Dependency Ratio will rise – the ratio of retirees to the working-age population. From the standard Census projection:

To my eyes, the basic numbers show that Social Security is, contrary to Karl, an enormous deal. Between 2010 and 2030, the Aged Dependency Ratio will rise 59%. Then it roughly stabilizes for the next two decades. Social Security has been in deficit since 2010, so without extremely unpopular cuts – or means-testing – fiscal balance will require combined Social Security tax rates to rise from 12.4% to about 20%. And that’s heroically assuming no disincentive effects of the tax hike.

Needless to say, such a tax hike wouldn’t make our heads explode. We’d live. But without major changes (by American standards), there will be a major fiscal crisis. The longer the U.S. delays, the worse the crisis will be when it arrives. And there is every reason to think that the U.S. political system will delay, delay, and delay again.

READER COMMENTS

John Thacker

Dec 18 2013 at 10:26am

Similarly, I’ve seen people argue that Social Security isn’t a big deal because all we have to do is cut benefits by 20% or so, as if that would be easy and painless.

It’s true that Social Security cannot go bankrupt in the sense that taxes can always be raised or benefits cut, but it’s still worth noting how far off our current promises are from reality.

David R. Henderson

Dec 18 2013 at 10:37am

Did Karl Smith take a new job? If so, what? The link doesn’t say.

Bostonian

Dec 18 2013 at 11:21am

Many conservatives and libertarians oppose direct increases in marginal tax rates on income and savings but fail to acknowledge the means-testing is an indirect way of doing the same thing. There is a conflict between transparency and incentivizing work and savings. If in 2030 the government suddenly announces that new applicants for Social Security benefits would be rejected if they had earned more than X during their lifetime, their lifetime earnings would not have been diminished by the means-testing tax, but they would be outraged. If the government announces means-testing long in advance, there will be less (but earlier) outrage, but people will adjust their behavior accordingly.

John Thacker

Dec 18 2013 at 11:59am

@Bostonian:

“Means-testing” is usually used differently from decreasing Social Security based on lifetime earnings. (The Social Security formula does a little bit of the latter already.)

Usually means-testing is used to refer to reducing Social Security benefits based on the income that someone has in retirement from other sources. So when someone uses the phrase “means-testing,” I like to verify what they mean. It has a profound difference in the effect on savers.

Means-testing based on income in retirement explicitly punishes savers. I find it quite unfair as well as being a bad idea. If A and B earned the same amount of income over their career, but A saved more while B spent more on nicer cars, clothes, trips, etc., why should A get less Social Security?

Overall, I prefer looking at lifetime earnings, because it makes up for the problem that progressive income taxes don’t really seem “fair” when someone people have income that varies much more widely from year to year.

Like any of these changes, they should indeed be announced ahead of time to let people plan. That’s the primary problem with the “there’s no problem” approach of Karl and others; there’s no problem so long as we start planning now and make sure people know what’s coming. I think that there will be a problem if we suddenly cut benefits by 20%, as under some scenarios.

Steve Roth

Dec 18 2013 at 1:02pm

The trustees say that if we devoted an extra .6% of GDP to SS, it would be solvent way beyond the predictable future (75 years).

Purely coincidentally, that is exactly the amount of revenue they say we’d raise if we scrapped the cap on SS contributions, so all earned income was subject to that “tax.”

Personally I’d much rather the see the program funded by taxes more efficient and progressive than labor taxes. But if liberals insist on maintaining the charade that this is a pension program (understandably so: it’s politically/rhetorically necessary to protect the program), this would at least make things more progressive than they are under the current system.

Andrew_FL

Dec 18 2013 at 2:42pm

Or we could. You know. End the dang thing.

Notorious B.O.B.

Dec 18 2013 at 2:44pm

Actually, the real issue with SS is NOT the technicalities of funding and taxation. The real issue is massive intergenerational unfairness arising from the historical political need to create a Ponzi scheme benefit payments mechanism. Simply put, current recipients receive an enormous real economic return on their past “contributions” — which paid for an even LARGER return for the earlier recipients who received the current recipients’ contributions.

And so on, and so on…..The first recipient, Ida Mae Fuller, paid $23 in “contributions” and received $22 THOUSAND in benefits…for all practical purposes every subsequent recipient has done worse.

It’s a rotten deal for anyone born after about 1960. Young workers today would literally be better off burying their SS “contributions” in the backyard.

The arguments based on productivity/growth assume a tree that grows to the sky — unsustainable economic growth and/or population growth. That is just to manage the program on a cash flow basis. But, as noted, that misses the point. The point being that SS is and always was a Ponzi scheme and as such inexorably has to be unfair to latecomers.

And when the music stops an almost intractable political problem arises. For existing beneficiaries to be protected without exacerbating the drag of regressive payroll taxes even further the underlying myths, lies and frauds of the unfunded, non means tested entitlements regime must be exposed with incalculable consequences for political elites running the show.

John Thacker

Dec 18 2013 at 3:03pm

Well, only if we scrapped the cap but also tweaked the formula to enter in an extra “bend point” so that people didn’t earn any more SS benefits for that extra tax that they were paying. If we scrapped the cap but extended the existing contributions to benefit formula (which already has three rates, then it wouldn’t raise enough revenue. For the formula, and the CBO has done a lot of analyses.

Right now people get benefits at marginal rates of 90%, then 32%, then 15% of average indexed monthly earnings. The scenario where it’s “exactly enough revenue” would be having a new 0% bracket, not extending the 15% band.

I would assume that having a new 0% bracket would bring in absolute howls from people to count unearned income as well. After all, it’s one thing to be taxed on income that at least increases your benefits by some amount, but being taxed while not getting anything more out of it? So politically I find the idea of raising the cap on only earned income while not increasing benefits thereby to be unlikely.

Arthur_500

Dec 18 2013 at 4:26pm

I believe that Social Security may have been less of a factor when people had retirement programs available. In this age of 401K and SIMPLE plans it is becoming ever more important.

SS does not invest the funds or give an individual what they earn. Pretty much everyone can get the same amount and many get much more than they put in.

Now Politicians use this as their little cash box so they can appear to run a solvent gubment and continue to make unsustainable promises.

Fact 1: Teachers Retirement requires a minimum of 18% investment and yet Social Security remains at 12.4%. Obviously the investment is too small.

Fact 2: Politicians have used SS to give away benefits that this fund was never intended for.

What if the SSA administered the collection and dissemination of the funds BUT each individual had their own account – much like an IRA, 401K or other retirement savings. The individual could pick and choose their own bank(s) but they could not touch the funds until SSA allowed it. SSA would collect the funds from the employer and funnel it to the individual account. Gubment would not have their hands in the candy jar, more money would be available for the markets, and individuals could get an actual retirement with a real return that could be passed on to their heirs.

MingoV

Dec 18 2013 at 5:11pm

Ditto. I’m collecting Social Security benefits, but I would give up those benefits to save my children (and possible grandchildren) from being at the bottom of the Social Security Ponzi pyramid.

Randy

Dec 18 2013 at 6:54pm

I think the ACA is the fix. Every generation since the 30s has faced a few percentage points payroll tax hike to pay for these programs, and that is effectively what the ACA is – about a 5% payroll tax hike. It may also represent a reduction in benefits to boomers as much of the cost of the ACA was “designed” to come out of Medicare, but it remains to be seen whether that will actually happen.

Floccina

Dec 19 2013 at 10:44am

The way that I see it is you can only tax people so much or they will start to work for cash or for in family consumption. So FICA is just part of total tax intake and cannot be separated from the incoem tax or other Fed taxes (BTW most people I know treat it as a pure tax not as retirement insurance purchases.) So the fact that FICA can or cannot cover the benefit is irreverent.

IMO SS is much more costly than it should be. SS should pay every retiree about $700/month no matter how much FICA taxes where extracted from their pay.

ThomasH

Dec 19 2013 at 2:03pm

The “disincentive effect” could be avoided by financing the needed increas in SS revenews and repeal of other payroll taxes by part of the revenues from taxes on carbon emissions.

libertarian jerry

Dec 19 2013 at 11:16pm

First of all Social Security is legally a tax. Second,the money dispersed is basically a benefit. When you “go on Social Security” you are basically going on welfare. Social Security recipients have no legal right to any so called “Trust Funds.” The taxes and the benefits can be ended tomorrow by Congress and Social Security recipients would be left with nothing. With that said,taxation (contributions)are needed but as long as the Federal Government,through the Federal Reserve System,can “create” as much money out of thin air as they want Social Security,as with most Federal programs,can be sustained indefinitely. The only problem is that fiat currency eventually destroys itself in an orgy of inflation. In essence,Social Security recipients will continue to receive their benefits but the benefit checks won’t even buy them a can of dog food.

Mark Bahner

Dec 23 2013 at 12:57am

Those numbers are obtained by comparing human retirees to human workers. The comparison between human retirees and human-plus-robot workers will be far different.

Dave Tufte

Dec 26 2013 at 4:53pm

It’s worse than you think Bryan.

Look at the purple bars and the numbers. In order for that to level off by 2030, it’s got to be assuming that there will be no increase in life expectancy.

That’s bizarre on the face of it.

Having said that, the reason it’s shown this way is that life expectancy is so poorly forecastable that no one forecasts it more than a few years out into the future. So the 2030 leveling no doubt indicates a lack of forecasts, rather than favorable ones.

Comments are closed.