Tyler Cowen recently linked to an interesting post by Edward Hugh. Hugh argues that much of the recent uptick in Japanese inflation is due to the recent depreciation of the yen. That may be true in an accounting sense, but it leads Hugh to misinterpret the situation in Japan:

Even the 0.7% annual rise in core-core inflation isn’t all it seems to be, since some 40% of the increase is accounted for by a one-off rise last year in charges for accident insurance and public services. The key point to grasp in all this is that the rise is due to what we could call “cost push” rather than “demand pull”. As Takeshi Minami, chief economist at the Norinchukin Research Institute put it,”Those increases had little to do with demand and supply.”

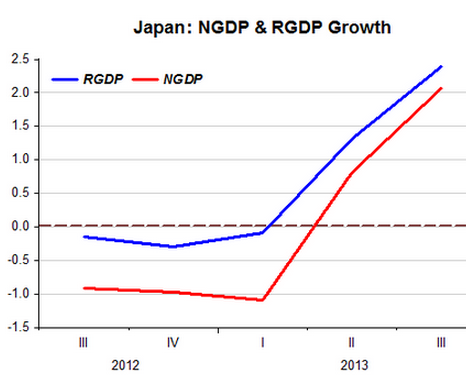

If that were true, then we’d see Japanese inflation rising at the same time that RGDP growth was falling. That’s what cost push inflation does, it shifts the AS curve to the left. Now look at this graph from a recent Marcus Nunes post.

This is precisely what a demand shock looks like. When monetary policy causes a currency depreciation, and both NGDP and RGDP rise, then you have experienced a demand shock. It’s not even a debatable point, the data is crystal clear.

Suppose the recent gains were merely due to the currency depreciation, and not an underlying boost to domestic spending. In that case the trade balance would obviously “improve.” Here’s what Hugh says actually happened:

But it’s worse, the monetary expansion has driven down the value of the yen but in the context of the second arrow – a double digit fiscal deficit – this drop in value is leading to a growing not a declining trade deficit.

Actually this is a good sign, as faster economic growth will often worsen a trade deficit. The US trade surplus shrank immediately after the sharp devaluation of 1933.

If Shirakawa is right all the ongoing attempts to reflate the Japanese economy may be simply working against history, with the central bank governors sitting there, like modern Canutes, trying to order back the waves. Maybe the theoretical debate is far from over, but the evidence is mounting that Abenomics may lead Japan’s economy to shipwreck, tossed between the Charybdis of a growing external imbalance and the Scylla of a deflation driven monetary black hole.

As an aside, I’m not sure Shirakawa is the person you want to cite here, as he is merely trying to explain away his failed monetary policy when he ran the BOJ. I certainly agree that Abenomics is likely to lead Japan to a shipwreck, however it will probably be on a soft sandy beach, rather than sharp rocks. As things stand today, Abenomics has clearly improved the situation in Japan, but just as clearly the improvement has not been sufficient. Japan still faces a fiscal crisis. Things are still likely to end badly. They are unlikely to hit the 2% inflation target in a sustained way, nor are they likely to hit the much more important milestone of 3% trend NGDP growth. They need to do so in order to reduce the extreme fiscal imbalances.

On the other hand, when compared to pre-Abe policies, Abenomics has been a smashing success. Things are finally moving forward.

There is much in the Hugh piece that I agree with. For instance, I agree that the amount of slack in the Japanese economy is much less than many assume. Don’t expect (RGDP growth) miracles from Abenomics. Yes, the policy has helped already, and further depreciation of the yen would help even more. However I see no sign that the Japanese government plans on further yen depreciation. And if they begin to allow yen appreciation for a sustained period then they will slide back into deflation.

The most discouraging aspect of the situation is that neither the Japanese government nor the American economics profession seems to understand the real issues facing the Japanese. They face a trade-off between NGDP trend growth rates and size of central bank balance sheets. If they want a low NGDP growth rate, they must accept an exceedingly large balance sheet, and vice versa. Prior to 2013 they seemed to want low NGDP growth but not a big balance sheet, and their policy predictably failed. But even today I don’t see much evidence that they understand that this is a choice they must make. Nor do I see any signs that American economists understand this dilemma.

Abe is also trying to pressure Japanese firms to raise nominal hourly wages, thus repeating the very worst mistake of the Roosevelt administration. Japan is still far from being out of the woods.

Update: In a comment section Mark Sadowski comments on a different part of the Hugh post. First he quotes Hugh:

“In the words of former Bank of Japan governor Masaaki Shirakawa, “Seemingly, there would be no linkage between demography and deflation. But it may not be the case. A cross-country comparison among advanced economies reveals intriguing evidence: Over the decade of the 2000s, the population growth rate and inflation correlate positively across 24 advanced economies.”

And then he responds:

This claim comes from the following paper (Chart 14)

https://www.boj.or.jp/en/announcements/press/koen_2012/data/ko120530a1.pdf

The paper finds no significant correlation for the same group of nations in the 1990s. Moreover the paper points out in a footnote that:

“Another cross-country inspection based on a broader sample, including developing countries, does not detect positive correlation between inflation and population growth in the 2000s and in earlier periods likewise.”

Mark’s comment has much more empirical evidence on this assertion.

READER COMMENTS

tom

Mar 3 2014 at 10:08am

I guess this just shows that basically everyone will cherry pick data to support their argument. If you extend your graph backwards to the early 90s you would see real GDP growth was above 2% in Japan 6 different times since 1995 link

Concluding that Abenomics is a smashing success compared to pre Abenomics based on 3 quarters of growth is very self serving. If those quarters turn into multiple years yo might well have some supporting data but basically all sides have been crowing about deflation in Japan over a period where there has been almost no deflation or inflation.

Scott Sumner

Mar 3 2014 at 10:11am

Tom, I agree that the GDP growth is no basis to claim success. There is lots of other data suggesting success.

Morgan Warstler

Mar 3 2014 at 11:10am

First off, even when “negative” when RDGP is above NGDP, how is that not “growth”?

Hugh puts forward a weak alternative theory: Demography.

Instead let’s look at a more compelling one: Digital

As the society goes digital vs atomic, we’re going to see far more “natural” price level deflation, it is a once in human history monsoon of natural price deflation.

My Q is isn’t the best of both worlds following a trend from Q4 2012 to Q12013: where RDGP grows slowly up and NGDP grows slowly down?

If digital can and wants to give us this, isn’t the point of MP (NGDPLT) to provide it?

Andrew_FL

Mar 3 2014 at 12:14pm

The heck is “core-core inflation?”

Gabriel Puliatti

Mar 3 2014 at 12:18pm

@Andrew_FL, if you read the article, you’d have found out.

Japanese core inflation includes energy. Core-core excludes it.

Andrew_FL

Mar 3 2014 at 12:25pm

Also:

How do you distinguish this from the effects of trade policy at the time, both that of the US, and other countries in the world?

Andrew_FL

Mar 3 2014 at 12:27pm

@Gabriel Puliatti-Thank you, even if you can barely contain your annoyance with my dumb question. Sorry.

Jeff O

Mar 3 2014 at 1:21pm

This post from David Andolfatto provides good perspective on this story.

http://andolfatto.blogspot.com/2014/02/monitoring-japan.html#comment-form

lxdr1f7

Mar 3 2014 at 8:23pm

” They face a trade-off between NGDP trend growth rates and size of central bank balance sheets.”

All the CB needs to do is recognize money as equity on its balance sheet and then it can expand all it needs to increase NGDP without worrying about the balance sheet. The CB can also create the mechanism to directly interact with the public and conduct heli drops.

Scott Sumner

Mar 3 2014 at 9:12pm

Andrew, The timing suggests it was the devaluation, but I can’t be sure. The same pattern seems to have occurred again with the Japanese case.

Jeff, Good link, I think David is right that the evidence for nominal success is much stronger than the evidence for real success.

lxdr, Given the size of the public debt, a helicopter drop would be a big mistake. They very much need to buy back debt.

lxdr1f7

Mar 3 2014 at 9:20pm

“lxdr, Given the size of the public debt, a helicopter drop would be a big mistake. They very much need to buy back debt.”

Is that because heli crops are funded by public debt issuance? Why do they need to buy back debt?

What if the heli drops arent conducted through the treasury (directly by the CB) and the CB accounts for newly created money as equity instead of debt on it’s balance sheet?

lxdr1f7

Mar 3 2014 at 9:56pm

“lxdr, Given the size of the public debt, a helicopter drop would be a big mistake. They very much need to buy back debt.”

Is that because heli crops are funded by public debt issuance? Why do they need to buy back debt?

What if the heli drops arent conducted through the treasury (directly by the CB) and the CB accounts for newly created money as equity instead of debt on it’s balance sheet?

Boonton

Mar 4 2014 at 6:18am

They face a trade-off between NGDP trend growth rates and size of central bank balance sheets. If they want a low NGDP growth rate, they must accept an exceedingly large balance sheet, and vice versa

This seems backwards to me. If they want a high NGDP growth rate, doesn’t that mean a large balance sheet as the central bank will create money to buy assets with, which increases its balance sheet? Likewise a low NGDP rate would entail buying fewer assets or even selling them off.

‘Trade-off’ implies having to take something bad for something good. I can understand why a higher NGDP growth rate is desired but I’m not clear why anyone cares about a high or low central bank balance sheet.

Scott Sumner

Mar 4 2014 at 10:07pm

lxdr, It doesn’t matter how helicopter drops are funded. It’s costly to give money away when you could spend it buying back your debt. Think of it as an individual. Who’s more likely to go bankrupt, someone who buys back their mortgage, or gives the money away to strangers?

Boonton, Faster NGDP growth leads to higher nominal interest rates which leads the public to hold a smaller share of base money to GDP. Compare Australia (4% of GDP) to Japan (30% of GDP.)

Comments are closed.