Most people find the NGDP shock/sticky wage theory of the business cycle to be at least slightly plausible. However I’m often asked why wages have not adjusted yet. Surely it doesn’t take 7 years for full adjustment to a negative demand shock?

A Bentley student named Daniel Reeves sent me a very interesting San Francisco Fed study of downward wage inflexibility and the business cycle, by Mary Daly and Bart Hobijn. Daniel immediately saw many places in the paper where the NGDP targeting approach would fit beautifully. (Ironically I don’t recall the study mentioning NGDP.) I think he’s right, but first I’d like to discuss why this is such a great study.

The authors create a mathematical model of the labor market, where they assume a given fraction of workers each year are resistant to wage cuts. The theoretical model predicts this sort of wage increase distribution:

There are several things to note here. The distribution is asymmetric, as far fewer workers get pay cuts than you’d expect if there were bell-shaped distribution. Many of the workers that would normally get pay cuts are bunched together at the zero wage change level, due to the assumed downward wage inflexibility. Second, the light grey line shows the wage distribution in the steady state (normal times) and the darker line shows the wage distribution 12 quarters after a severe negative demand shock. Notice that the negative shock compresses more wage gains close to zero.

The next graph shows the actual distribution of wage gains in 2006 (assumed to represent the steady state) and 2011 (a few years after a major negative demand shock:

It’s pretty clear that there is downward wage stickiness at zero. Indeed after this study (and earlier ones that reached similar conclusions) there really can’t be any doubt. There is no theoretical explanation for the spike at zero other than money illusion, and there is no explanation for the increase in the spike after a negative demand shock that doesn’t imply short-run non-neutrality of money.

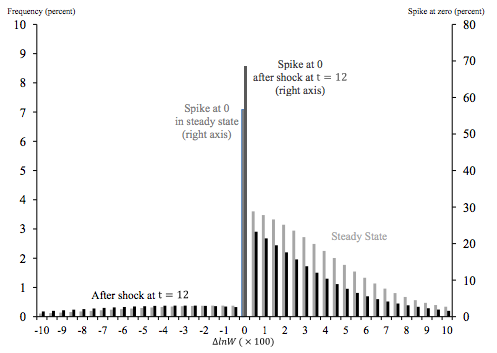

The model also predicts that the frequency of zero wage changes will be highly correlated with the unemployment rate, peaking slightly after the unemployment rate peaks. See what you think:

But can it explain the slow recovery from the 2008-09 demand shock? Yes it can, indeed that’s exactly what the model predicts:

That’s because after a negative demand shock there are many years of “pent-up wage deflation.” It takes many years for the labor market to adjust and the economy to heal. On the preceding graph 30 quarters corresponds to 7 1/2 years. I should add that the model is calibrated for the current level of wage stickiness (indeed it assumes a bit less that the current level.) But in other periods wages may have been more or less downward sticky than today. For example, wages had soared during and immediately after WWI, and it was fairly widely understood that under a gold standard they might have to return to normalcy at some point. Thus wage cuts in 1921 were quite common.

To some extent this paper repeats work done by others, but they also go well beyond previous research. For instance, they have a very nice explanation for why the Phillips Curve bends at low inflation rates. I should add that although they use inflation as their nominal scale variable, Daniel’s probably right that it fits the NGDP story even better. Consider the following:

Note that productivity growth has the same “greasing effect” on the labor market as inflation. When productivity growth is high wages have the tendency to rise anyway, which makes downward nominal wage rigidities less binding.

Consider China, which has extremely rapid productivity growth, and hence very rapid nominal wage growth, despite an inflation rate that’s fairly similar to the US. Because the trend growth in nominal wages is so high in China, you’d expect downward wage inflexibility to be much less of a problem in China than in the US. I frequently argue that NGDP growth is often the best proxy for the welfare costs and benefits of inflation, better than inflation itself. This is one more such example, as NGDP growth is strongly correlated with productivity growth plus inflation.

Just as rapid NGDP growth can keep a country above the zero interest rate bound, even if they have low inflation, rapid nominal wage growth can keep a country away from the zero lower bound of wage increases, even if they have low inflation. But the good news is that NGDP growth need not be all that rapid; moving from 2% inflation to 10% inflation has little addition benefit in their model (which assumes 2.7% productivity growth.) They also point out that a combination of a negative productivity shock and negative demand shock is especially harmful in their model. Which pretty much explains the past 7 years.

To summarize, their model nicely fits the stylized facts of nominal wage stickiness, especially at the zero rate change level, and it explains all the key attributes of the severe recessions that hit the US and Europe in 2008, which were accompanied by a slowdown in productivity growth. I’ve often been critical of modern macro research, but this paper is a near perfect example of how to creatively combine theory and empirical work, in a fashion that actually explains the world we live in. Highly recommended.

READER COMMENTS

Kevin Donoghue

Apr 12 2015 at 11:51am

“There is no theoretical explanation for the spike at zero other than money illusion….”

Isn’t money illusion usually described as an ad hoc device for generating non-neutrality of money, rather than a theory?

Mike Sproul

Apr 12 2015 at 12:44pm

Why are people so puzzled by sticky wages and unemployment? A hotel room sits empty (unemployed) because its price is sticky. A shirt hangs unsold (unemployed) on a rack because its price is sticky. A worker sits unemployed because his wage is sticky. In every case, the seller is making a rational choice not to sell, in the hope of a better price to come.

Levi Russell

Apr 12 2015 at 12:48pm

What strikes me is how much different Figure 1 is from the theoretical distribution. Wages seem to be significantly less downwardly-sticky than their theoretical graph indicates.

Jason Smith

Apr 12 2015 at 12:55pm

If you look at the relative fraction of people in the zero wage change state, it’s still only involves 8-16% of people not being chosen by the Calvo fairy; that means 84-92% of people do not have ‘sticky wages’ … their wages are changing by upwards of 20%!

There’s another piece to this story — the wage changes are for those that are still employed. The shock to NGDP manifests itself as a combination of a rise at zero wage change and the people thrown out of the distribution entirely

http://informationtransfereconomics.blogspot.com/2014/10/coordination-costs-money-causes.html

The biggest issue is that the peak just under 5% in the data doesn’t move between 2006 and 2011. Wages are sticky in aggregate (the distribution doesn’t move), but individual wages change by 10, even 20%.

Don Geddis

Apr 12 2015 at 2:40pm

@Mike Sproul: A rise in the macroeconomic rate of overall unemployment (such as the jump from ~5% to ~10% around 2008 in the US) is not due to workers making the “rational choice not to sell” their labor.

Nominal shocks plus sticky wages (& debts) cause economy-wide recessions, in a way somewhat more complex than a specific hotel room not being rented “in the hope of a better price to come”.

Jim Rose

Apr 12 2015 at 6:32pm

There is plenty of evidence of downward wage flexibility in both existing jobs and in new job matches.

See What can wages and employment tell us about the UK’s productivity puzzle? by Richard Blundell, Claire Crawford and Wenchao Jin showing that in the recent UK recession 12% of employees in the same job as 12 months ago experienced wage freezes and 21% of workers in the same job as 12 months ago experienced wage cuts. Their data covered 80% of workers in the New Earnings Survey Panel Dataset. Larger firms lay off workers; smaller firms tended to reduce wages.

This British data showing widespread wage cuts dates back to the 1980s. Recent Irish data also shows extensive wage cuts among job stayers.

See too Chris Pissarides (2009), The Unemployment Volatility Puzzle: Is Wage Stickiness the Answer? arguing the wage stickiness is not the answer since wages in new job matches are highly flexible:

1. wages of job changers are always substantially more procyclical than the wages of job stayers.

2. the wages of job stayers, and even of those who remain in the same job with the same employer are still mildly procyclical.

3. there is more procyclicality in the wages of stayers in Europe than in the United States.

4. The procyclicality of job stayers’ wages is sometimes due to bonuses, and overtime pay but it still reflects a rise in the hourly cost of labour to the firm in cyclical peaks

How do existing firms who will not cut wages survive in competition with new firms who can start workers on lower wages? Industries with many short term jobs and seasonal jobs would suffer less from wage inflexibility.

see more at http://utopiayouarestandinginit.com/2014/06/27/is-unemployment-voluntary-or-involuntary/

Scott Sumner

Apr 12 2015 at 7:50pm

Kevin, You asked:

“Isn’t money illusion usually described as an ad hoc device for generating non-neutrality of money, rather than a theory?”

Why can’t it be both? Think of it this way. They did the proper test to see if money illusion exists, and they found it does exist. That means they tested the theory, and it held up.

Mike, Sticky wages may be rational at the individual level (ignoring external effects), but I would argue that money illusion is not.

Levi, Most of the wage cuts are probably people switching jobs. But the spike at zero is even higher than in the theoretical model. The authors report that they found even more downward stickiness than their model predicts.

Jason, You said:

“If you look at the relative fraction of people in the zero wage change state, it’s still only involves 8-16% of people not being chosen by the Calvo fairy; that means 84-92% of people do not have ‘sticky wages’ … their wages are changing by upwards of 20%!”

This is incorrect. In their model they assume 90% have downward sticky wages, but that still allows for wage increases. Also, the distribution of wage changes shifted left, from about 3.5% wage inflation to about 2% wage inflation on average. The model actually fits the data quite well.

Jim, Good points.

Bill Conerly

Apr 12 2015 at 8:54pm

I saw this post just after seeing Greg Mankiw point to Noah Smith’s paean to sticky wages: http://www.bloombergview.com/articles/2015-04-10/how-sticky-prices-might-be-the-cause-of-recessions

I don’t understand why we don’t try policy to unstick wages. Policy certainly cannot totally unstick wages, but we might think about reducing stickness.

Government could mandate prompt adjustment of government employee wages to labor market conditions; could require the same of government contractors; and could ban union contracts that have no downward adjustment clause. None of these ideas are on the table.

Why not?

David Andolfatto

Apr 13 2015 at 12:23am

I’d be interested to know what people think of this rebut:

http://andolfatto.blogspot.com/2010/07/sticky-price-hypothesis-critique.html

Kevin

Apr 13 2015 at 3:14am

Because the politicians who might pass such a law want to be reelected. What’s such a candidate’s response when their opponents points out they voted to cut the electorate’s wages?

Miguel Madeira

Apr 13 2015 at 6:56am

“There is no theoretical explanation for the spike at zero other than money illusion”

Could not be also because of the difficulty of renegotiating an existent contract?

Scott Sumner

Apr 13 2015 at 9:41am

Bill, The government could and should reduce wage stickiness, but it wouldn’t solve the problem, or even reduce it by 20%. You’d still need sound monetary policy.

David, I’ll take a look.

Miguel. But why should existing contracts specify a 0% wage gain, and not some other number?

Scott Sumner

Apr 13 2015 at 10:03am

David, I have several comments:

1. I’m not convinced that price stickiness is an important macro problem. But I do think wage stickiness is.

2. I agree that when an individual worker becomes unemployed, it rarely seems like wage stickiness is the cause. And that’s because (in my view) it is rarely the stickiness of individual wages that explain individual layoffs, rather individual workers are laid off in larger numbers during recessions due to macro wage stickiness. In other words, there are big external effects from the stickiness of individual wages.

3. I agree that many relationships between workers and employees are not best described as perfect competition. In some of these cases (such as my tenured job at Bentley) wage stickiness is unrelated to allocative efficiency, as you suggest. But there are lots of jobs where companies are free to lay off workers, and the large external effects I referred to imply that if aggregate wage levels are highly inertial (as they are), and NGDP is highly variable, then employment will be strongly correlated with NGDP shocks.

4. I would add that I don’t see your critique of wage stickiness addressing the specifics in the paper I discussed. Some of their empirical work seems pretty persuasive to me, but perhaps I am missing an alternative explanation for the evidence.

5. You mention skepticism about popular views of the liquidity trap. My own views are probably intermediate between you and someone like Krugman. Unlike Krugman, I believe that much of the divergence between say Greece and Switzerland (which are both experiencing deflation) is supply-side, with Greece being the far less free market economy. I am a “supply and demand-sider.” Krugman thinks that it’s almost all demand-side, and that free market policies don’t help.

Maurizio

Apr 13 2015 at 10:50am

Prof. Sumner, what is the answer to this question in plain words? As a noneconomist, I am struggling to see how this article provides an answer. Thank you

David Andolfatto

Apr 13 2015 at 8:49pm

Scott, let me reply to your comments point wise.

[1] If I had to argue for a nominal rigidity, I’d place it on nominal debt arrangements. And because wage obligations are usually a form of nominal debt, I could be persuaded.

[2] We have to be careful how we define “stickiness.” In our models, it is defined as something that cannot move for exogenous reasons. In fact, wages could be highly flexible in principle, but not in equilibrium. If lowering the way of a worker makes that worker adopt a bad attitude that reduces the productivity of his/her colleagues, it may make sense just to let that worker go, rather than cut their wages, for example. I wonder if the the source of the stickiness matters for policy questions.

[3] Freedom to lay off workers does not mean that relationships are not important, anymore than the freedom to leave your spouse does. The question is how resources within the relationship are allocated and whether this division has anything to do with empirical wage/price measures.

[4] Agreed.

[5] OK. Thanks for your responses!

Scott Sumner

Apr 14 2015 at 10:31am

Maurizio, Suppose the recession causes wages to be 10% above equilibrium. Workers accept a zero pay increase, and now they are 8% above equilibrium. Workers accept another zero pay increase and they are now 6% above equilibrium. That adjustment process takes some time to play out. It’s what they mean when they talk about pent up wage deflation.

David, All good points. Here’s the relevant counterfactual in my view. Wages had been rising 3% to 4% a year before the Great Recession. Then NGDP suddenly plunges 8% below trend. When I talk to some new classical economists, they tell me that in the counterfactual where the Fed aggressively stimulates, and keeps NGDP growing at trend, the path of nominal wages is 8% higher than what we actually saw, and hence the Great Recession is just as bad as the one we actually experienced. Inflation is also very bad, as RGDP plunged while NGDP keeps rising at its pre-recession 5% rate.

In my view the counterfactual is that wages are very inertial, and continue to grow about 3% or 4%, and we have a very mild recession with a modest uptick in inflation.

So you are right that the inertial behavior of wages doesn’t prove anything by itself. It’s a question of how wages would behave under alternative monetary policies

BTW, if the Fed got moving and created the NGDP and RGDP macro futures markets that we need for research purposes, these questions would be fairly easy to answer.

One other point, I view the distinction between real and nominal wage stickiness as being crucial. Both may exist, but nominal stickiness is the sine qua non of sticky wage/AD shock theories of the business cycle.

Levi Russell

Apr 14 2015 at 9:03pm

I see your point. However, are there not a much higher proportion of people experiencing falling wages than predicted? Am I missing something in the first two charts?

David Andolfatto

Apr 14 2015 at 9:53pm

Scott,

Does it fall within the Fed’s present Congressional mandate to create markets in the instruments you want? (I honestly don’t know. If we do, I’ll do everything I can to help.)

David

Scott Sumner

Apr 15 2015 at 10:55am

Levi, The data shows one year changes, whereas the model shows quarterly changes. Perhaps that explains some of the difference.

To be honest, I wasn’t 100% sure I fully understood the way they handled their data, so I am partly taking them at their word. I hope others will take a closer look and see if their claims are justified.

David, Thanks. I am not certain exactly what the Fed is allowed to do, but I will say this:

1. The cost would be very low relative to the Fed’s budget. For one or two million dollars per year you could create a couple of very liquid prediction markets. Indeed a pilot project could be done for a tenth of that amount.

I just created a NGDP prediction market for $10,000, and I am in the process of setting up a NGDP futures market for $26,000.

2. I would think the expenditure could be justified as a part of the Fed’s economic research mandate. The biggest obstacle would be if it somehow generated controversy. The Federal government ran into a Congressional buzz saw with its terrorism prediction market, but obviously NGDP is far, far less controversial a topic than terrorism.

I have met some of the Congressional staffers in recent years, and would be glad to testify in favor if that would help. You could also get bigger names like Justin Wolfers.

3. We do have some market indicators of inflation (TIPS spreads, etc) but not NGDP. Given that inflation expectations can reflect either “demand shocks” such as more nominal spending (as in the 1960s) or “supply shocks” like an energy embargo (1974), and given that the Fed has said that it is important to distinguish between the two types of inflation, I’d think NGDP futures would be really useful. The Fed creates lots of natural experiments, any time the policy announcement is strongly unexpected (as when tapering was delayed in late 2013.) It would be useful to observe real time market reactions for expected NGDP and RGDP growth in response to those shocks.

4. It would also be interesting to observe how expected US growth is (or isn’t) impacted by monetary stimulus at the ECB or BOJ.

Lorenzo from Oz

Apr 19 2015 at 3:43am

Since wage stickiness has increased over time, does that not make money illusion a poor explanation, unless we have some reason why it might have increased over time?

Comments are closed.