Bob Murphy has a new post discussing the similarities between the fiscal policy of 2013 (often called ‘austerity’) and the fiscal policy of 1937, which some Keynesians believe helped cause the 1937-38 depression (which was relatively deep).

In fact, there are lots of similarities that Bob missed. Consider the following discussion of tax policy in 1937.

On the revenue side, it is apparent that revenues increased sharply in the first quarter of 1937. There are two main factors. The most important one is the increase in income tax revenue, which grew by 66 percent from 1936 to 1937. This was due to a significant increase in income tax rates in the Revenue Act passed in June 1936. The rates previously ranged from 4 percent (starting at $4,000) to 59 percent (above $1 million). They remained unchanged for income brackets below $50,000, but were increased above that threshold, to reach 75 percent on the top earners. As a result, the average marginal tax rate for incomes above $4,000 almost doubled, from 6.4 percent to 11.6 percent.

The second factor, of lesser quantitative importance, is the beginning of Social Security taxation. The Social Security tax rate was 2 percent, with half paid by the employer, and the ceiling was $3,000. Collection began in January 1937, and represented 10.5 percent of total federal tax receipts for the year 1937.

So two major tax increases occurred on January 1, 1937; the payroll tax rate rose by 2 percentage points (from 0% to 2%) and the income tax was raised, but only on the wealthy. On January 1, 2013, the payroll tax rose by 2 percentage points, and income taxes were raised, but only on the upper middle class and wealthy. (Note, the 2013 increase affected people making over $200,000, but in real terms that was much less than $50,000 in 1937. Also note that the income tax was a far less important source of revenue back then.)

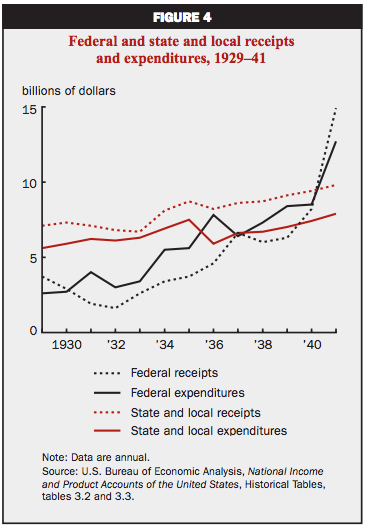

In a recent post Paul Krugman pointed out that the cuts in government spending (the “sequester”) were largely offset by increases in state and local spending (or more precisely, decreases in the rate at which spending was being cut.) Now look at this graph for the 1930s, from the same source:

One of the things that made the austerity of 1937 seem fairly dramatic is that in June 1936 Congress gave WWI veterans a large, one-time “bonus” payment, equal to about 2% of GDP. Because this was not repeated in later years, government spending fell off in 1937. But notice that the rise in Federal expenditure during 1936 is roughly offset by the fall in state and local expenditure, and then in 1937 these two factors reverse. It’s not a perfect offset, but it’s strikingly similar to the pattern that Krugman observed in 2013.

What can we make of all of this? Unfortunately we can’t get a clear answer, partly due to data limitations, and partly due to ambiguity in what the Keynesian model says is the right way to measure austerity. I’ll try to summarize the pros and cons for arguing that 1937 and 2013 are similar.

1. In 1936 the fiscal year ran July 1 to June 30, now it runs October 1 to September 30. That makes things tricky, given that in both cases much of the austerity begins on January 1. Bob Murphy quite reasonably responds by looking at two-year changes in the budget deficit. His figures actually show a bit more austerity in 1936-38 than my figures (which are from the St Louis Fred. He finds the deficit fell by 5.3% of GDP; the St. Louis Fred says it fell by a bit under 5%. Either way that’s a bit more contraction than in a two year period around 2013 (which is roughly 4.3% of GDP.)

2. There are additional factors, which cut either way. Many Keynesians would point to the change in the change in the deficit as determining the change in GDP growth rates. That is, it’s not whether you are running a big or small deficit that matters, or even whether it is rising or falling, but rather whether it is rising or falling faster than in recent years. That approach makes 1937 look more austere, although if you use calendar 2013 instead of fiscal 2013, the drop-off in 2013 is a bit more dramatic than using fiscal years. Growth really should have slowed in 2013.

3. Bringing in state and local spending (which is unjustified in my view) would be roughly a wash, as it affects both periods in about the same way.

4. Keynesians believe in looking at the cyclically-adjusted deficit. And this point is something that goes against 1937 having more austerity. Real GDP growth in 1935-37 was very high, with the first half of 1937 showing a real GDP nearly 25% higher than in the first half of 1935 (Balke and Gordon estimates). That means the cyclically adjusted deficit shrinkage in 1937 was significantly smaller than the actual deficit shrinkage. But I’m not certain how much. You might be surprised by the fact that RGDP growth in 1937 was so strong, as the recession began in mid-year. But the severe recession only began in Q4, and the level of GDP in late 1936 and the first half of 1937 was extremely strong—the only “boom-like” 12 months of the entire 1930s. Yes, the official unemployment rate was still high, but that’s partly because workers on government works projects were counted as unemployed. There’s a reason both the FDR administration and the Fed thought contractionary policies were needed. They were wrong, but the economy really did seem to be recovering quite rapidly at that moment, and (WPI) inflation was rising sharply.

In contrast, RGDP growth has been slow in recent years, and hence the cyclically-adjusted deficit is not dramatically different from the actual deficit.

I’ve probably made a few mistakes here, but I think it’s fair to say that the level of austerity in 1937 was probably a bit more than 2013 (due to the bonus phase-out), but in a qualitative sense the two fiscal austerity projects shared a number of striking similarities. If you take out the bonus payments then the fiscal contraction from 1935 to 1938 would have been fairly smooth, and very similar to 2011-14. One study estimated that the bonus payments boosted 1936 RGDP growth by 2 1/2% to 3%. But even without that boost, RGDP growth was very rapid brisk during the 1933-41 recovery (mostly 8% to 12%/year), and thus not repeating the bonus payments in 1937 obviously can’t explain one of the most severe depressions of the 20th century, one year later.

Of course there’s also the monetary offset problem. The Fed did some contractionary policies in late 1936 and early 1937 (reserve requirement increases, gold sterilization) precisely because inflation was rising sharply. Indeed there was perhaps even a sort of “fiscal offset”, as the bonus payments were enacted over FDR’s veto, and the administration immediately tightened fiscal policy. Nonetheless, I believe the bonus payments did provide a short-term boost to the economy in late 1936—the monetary offset kicked in a bit later.

None of this should be viewed as a critique of moderate Keynesianism. I recall that economic historians like Christina Romer argued that fiscal contraction played some role in the 1937 business cycle, but that monetary policy was the key driver of AD in the late 1930s. Rather I’m suggesting that people be careful drawing simple lessons from complex cases. Fiscal policy was probably modestly more contractionary in 1937 than 2013, but the differences were not large enough to draw radically different conclusions from the two episodes.

FWIW, in my research on the Depression I pointed to the big rise in real wages during 1937-38, which had two causes:

1. A big rise in nominal wages after a massive unionization drive, which doubled union membership between 1936 and 1938 (probably due to the Wagner Act.)

2. A sharp shift from gold dishoarding in 1936 and early 1937 (which was inflationary) to gold hoarding in late 1937 and early 1938 (which was deflationary.) The dollar was pegged to gold at $35/oz during the period, and the base tended to follow changes in the monetary gold stock. As prices fell sharply in late 1937 and early 1938, real wages soared.

It’s actually far more complicated than that, and I have a book coming out in December that explains it all in more detail.

READER COMMENTS

CA

Jun 26 2015 at 2:40pm

Good lord Scott, when is your Great Depression book gonna be published?

Luis Pedro Coelho

Jun 26 2015 at 3:29pm

One thing I never really understood is this “business cycle adjusted deficit” concept. I get a fuzzy idea, but I’ve never really seen it nailed down. How does this avoid just becoming a “get out of jail” card for failings of rude Keyenesianism?

If there is a deficit and the economy grows (or avoids a crash), then stimulus works (UK 2010). If it doesn’t grow, then the “business cycle-adjusted” deficit becomes smaller, ie, there was not enough stimulus (US 2009)

If there are cuts and the economy stalls, well then austerity kills (Greece, 2008-2050). If there are cuts and the economy grows, well then after “budget cycle adjustment” there were no cuts so the theory is intact (Britain 2012-14, US 2013, Iceland).

(An answer which mentions “potential GDP” is just replacing one fuzzy concept with another)

Scott Sumner

Jun 26 2015 at 3:43pm

CA, Hopefully before the 100th anniversary of the crash! Seriously, I’m told December, but there have already been lots of delays. I had no idea the publication process could be so frustrating.

Luis, I’ve had similar concerns, but I’m not a Keynesian, so I just go with the data that they seem to think is important.

bill

Jun 26 2015 at 5:56pm

From the post: “Many Keynesians would point to the change in the change in the deficit as determining the change in GDP growth rates.”

I noticed that Krugman really seemed to be saying that in his post on 2013 too, but it’s ridiculous. Leave aside that the deficit itself is already the first derivative of total debt…

The implication is this. If the deficit in year 1 is 8% of GDP and in year 2, it’s 6%, then it’s not austerity if the year 5 budget is balanced and by year 10 we’re running a surplus that is 10% of GDP. All because a 2% of GDP reduction is somehow a baseline? What about in 2 decades when we’re running a surplus that is 30% of GDP? (not possible since the entire debt would have been paid off around year 15!)

I can totally accept that a Keynesian can say that, for instance, a 6% deficit isn’t stimulus if the deficit has been 6% for a couple of years. But going one derivative further is ludicrous.

BC

Jun 26 2015 at 7:01pm

Interest rates are not a good indicator of monetary policy; one has to look at aggregates like NGDP. If one assumes certain monetary regimes, however, could one similarly define fiscal policy stance in terms of aggregates rather than deficits (or changes in deficits, or changes in changes in deficits, etc.)? For example, if the central bank committed to a Taylor Rule and promised no QE or forward guidance (other than the implicit guidance in the Taylor Rule) at the zero-rate bound, then would it be possible for the fiscal authorities to achieve any NGDP they want by adjusting the deficit, at least at the ZRB?

Maybe, fiscal austerity is best defined (1) relative to a given monetary regime rather than in isolation and (2) in terms of the effect on NGDP, if that particular monetary regime even allows fiscal policy to impact NGDP. So, there may be some monetary regimes like NGDPLT in which there is no such thing as austerity due to monetary offset, but there may be other regimes like Taylor Rule in which fiscal austerity may be a meaningful concept??

Scott Sumner

Jun 27 2015 at 10:13am

BC, You asked:

“For example, if the central bank committed to a Taylor Rule and promised no QE or forward guidance (other than the implicit guidance in the Taylor Rule) at the zero-rate bound, then would it be possible for the fiscal authorities to achieve any NGDP they want by adjusting the deficit, at least at the ZRB?”

Absolutely not. Only monetary policy can achieve hyperinflationary growth rates of NGDP.

E. Harding

Jun 27 2015 at 1:07pm

Neither of the two versions of the second link seem to work for me.

marcus nunes

Jun 27 2015 at 2:45pm

[Comment removed for policy violations. Please read our Comment Policies. Email the webmaster@econlib.org to request restoring your comment privileges. A valid email address is required to post comments on EconLog and EconTalk.–Econlib Ed.]

mico

Jun 28 2015 at 9:49am

file:///Users/micro2/Downloads/ep-4qtr2009-part2-velde-pdf.pdf

This is an internal link to something you have downloaded to a local PC.

Scott Sumner

Jun 28 2015 at 11:09am

E. Harding and mico, Sorry, the link is fixed.

Mr. Econotarian

Jun 29 2015 at 1:26am

Perhaps fiscal and monetary policy were not the cause of the late 1937 recession, but instead the “animal spirits.” There was a world stumbling into war.

In October 1937, FDR gave his “Quarantine Speech.” Ask yourself if you would be investing in a business after hearing this:

“If those things come to pass in other parts of the world, let no one imagine that America will escape, that America may expect mercy, that this Western Hemisphere will not be attacked and that it will continue tranquilly and peacefully to carry on the ethics and the arts of civilization.

If those days come “there will be no safety by arms, no help from authority, no answer in science. The storm will rage till every flower of culture is trampled and all human beings are leveled in a vast chaos.”

Comments are closed.