Paul Krugman has a new post on Japan, which makes some good points. He considers the possibility that Japan will never escape the zero rate trap. I don’t think that we have a good sense of what that scenario implies, but it does call into question one important transmission channel for fiscal policy—permanent monetary injections.

He also argues that the main problem in Japan today is not that deflation leads to high unemployment (it is currently 3.4%), rather that deflation leads to a high and rising ratio of public debt to GDP. I’ve frequently made the same argument.

But here I think Krugman goes off course:

And here’s the thing: under current conditions, with policy rates stuck at zero, Japan has no ability to offset the effects of fiscal retrenchment with monetary expansion.

I don’t understand that claim, as NGDP growth in Japan has accelerated since the beginning of 2013, despite:

1. Fiscal austerity (higher sales taxes)

2. Worsening demographics (compared to the late 1990s and early 2000s.)

And yet despite those headwinds the unemployment rate has fallen under Abenomics. If that’s not monetary offset, I don’t know what is.

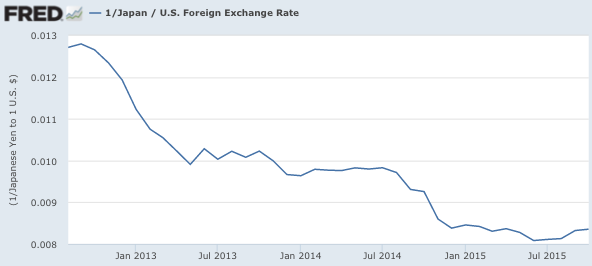

The Japanese should further increase the national sales tax and/or cut government spending, and offset the effect with further depreciation of the yen. The Keynesian model says the BOJ cannot depreciate the yen at the zero bound, but last time I looked they had depreciated it from 80 to 120/dollar.

Who are you going to believe: Keynesian liquidity trap theory or your lying eyes?

PS. A 2% or 3% NGDP target, level targeting, would also help.

READER COMMENTS

bill

Oct 21 2015 at 6:43pm

I believe my own lying eyes

I’d like to see them target 4% NGDPLT until they get off the ZLB. I say that because too large a portion of the people (American, Japanese, European…) can not wrap their minds around anything other than interest rates, so we need to get back to rates a good bit above zero again via NGDP growth. (ie, just raising rates for the heck of it like our Fed is considering is not what I mean)

Maurizio

Oct 22 2015 at 3:13am

The Japanese should … cut government spending, and offset the effect with further depreciation of the yen.

I don’t understand why you seem to talk interchangeably of monetary expansion and depreciation. Are they the same thing? Does monetary expansion always imply depreciation? If not, is it monetary expansion that matters, or is it depreciation? What if a country does monetary expansion in a recession, but this does not result in depreciation? Will this work or not?

Why is this important: countries cannot all depreciate at the same time, but they can all do monetary expansion at the same time.

ThomasH

Oct 22 2015 at 6:32am

The argument against “austerity” is that governments should not pass up opportunities to invest in positive NPV activities. If Japan’s opportunities all have negative NPV’s they should reduce spending. Since they have done a lot of public expenditure, that could be the case and they should shift buying power to the private sector so it can invest in positive NPV activities. If neither has any positive NPV opportunities, that’s Gordon style secular stagnation.

Garrett M

Oct 22 2015 at 9:01am

Maurizio, expansionary monetary policy involves either increasing the supply of money or reducing the demand for it. Depreciating the yen is one way to do expansionary policy, but it could either function through increasing the supply (buying dollars with yen) or decreasing the demand (targeting a $/Yen rate that’s lower than the current).

Monetary expansion doesn’t always imply currency depreciation. I suggest reading the wikipedia article on the Dornbusch Overshooting Model to learn more about this.

ThomasH, what if the NPV of crowded-out private projects is greater than the NPV of public projects? Obviously crowding out is theoretical, but so is NPV 🙂

LK Beland

Oct 22 2015 at 9:51am

Maurizio

“Why is this important: countries cannot all depreciate at the same time, but they can all do monetary expansion at the same time.”

There are different ways to define depreciation. If all countries decided to enact very aggressive monetary expansion, their currencies would depreciate, relative to a basket of products and services.

Prof. Sumner

I think you are completely right. 3% NGDP (i.e. 2-2.5% inflation) and a balanced budget would do wonders for their debt/gdp ratio.

However, will it be enough to get them off the ZBL? I understand the ZBL should not be a concern under NGDPLT, but it seems very important to finance types and central bankers, who will see NGDPLT as a failure if it does not get Japan off the ZBL.

Brandon Berg

Oct 23 2015 at 8:22am

If the Japanese government wants higher inflation and lower debt, why can’t it just print money and use that money to repay debt directly? Sooner or later it either gets inflation or pays off its debt, right?

The fact that people who know more about economics than I do see this as a difficult problem suggests to me that I’m missing something, but I have no idea what it is.

Scott Sumner

Oct 23 2015 at 9:16am

Maurizio, That’s a good point, the exchange rate is not the best way of thinking about monetary policy. But when discussing Japan I sometimes like to refer to the exchange rate to head of tiresome claims that the BOJ is out of ammo, and can’t do anything to stimulate NGDP growth. Other things equal, more monetary stimulus implies a weaker yen.

All countries can depreciate against a basket of commodity prices, at the same time.

LK, I’m not sure, but if 3% NGDP targeting did not get them off the zero bound, then it would be extremely effective in reducing the burden of the national debt. Over 24 years the debt ratio would fall in half, relative to existing policy.

Vincent Cate

Oct 23 2015 at 9:25am

Japan is spending about twice what they get in taxes. Calling this “fiscal austerity” or “fiscal retrenchment” is just wrong. When countries start funding their large deficits by printing money the risk is runaway inflation. The more people who want to get out of government bonds, the more the central bank must print money and buy government bonds. But the more they print money, the less people want to hold government bonds. You get a death spiral that kills the currency.

http://howfiatdies.blogspot.com/2014/08/positive-feedback-theory-of.html

Comments are closed.