Noah Smith has an article in Bloomberg discussing a new paper by David Autor, David Dorn and Gordon Hanson (ADH):

In his recent book “Economics Rules,” Harvard economist Dani Rodrik laments how economists often portray a public consensus while disagreeing strongly in private. In effect, economists behave like scientists behind closed doors, but as preachers when dealing with the public.

Nowhere is this evangelism clearer than on the issue of trade. Ask any economist what issue they agree on, and the first answer you’re likely to hear is “free trade is good.” The general public disagrees vehemently, but economists are almost unanimous on this point.

But look at actual economics research, and you will find a very different picture. The most recent example is a paper by celebrated labor economists David Autor, David Dorn and Gordon Hanson, titled “The China Shock: Learning from Labor Market Adjustment to Large Changes in Trade.” The study shows that increased trade with China caused severe and permanent harm to many American workers:

Adjustment in local labor markets is remarkably slow, with wages and labor-force participation rates remaining depressed and unemployment rates remaining elevated for at least a full decade after the China trade shock commences. Exposed workers experience greater job churning and reduced lifetime income. At the national level, employment has fallen in U.S. industries more exposed to import competition…but offsetting employment gains in other industries have yet to materialize.

Autor, et al. show powerful evidence that industries and regions that have been more exposed to Chinese import competition since 2000 — the year China joined the World Trade Organization — have been hit hard and have not recovered. Workers in these industries and regions don’t go on to better jobs, or even similar jobs in different industries. Instead, they shuffle from low-paid job to low-paid job, never recovering the prosperity they had before Chinese competition hit. Many of them end up on welfare. This is very different from earlier decades, when workers who lost their jobs to import competition usually went into higher-productivity industries, to the benefit of almost everyone.

I have a lot of problems with this claim. First, even if China trade was bad for the US, it was almost certainly extremely good for China, which was a vastly poorer country in 1990. So I’m quite confident that economists are justified in supporting free trade. Whether they are justified in suggesting that Chinese trade is beneficial to the US is another question.

Second, this is just one study, and as we’ll see it’s far from convincing. We don’t abandon views held for 200 years, and supported by hundreds of studies, just because of a single study. I can’t speak for other economists, but I very much doubt whether economists are holding back some sort of “secret” information that free trade is actually bad.

The ADH paper does show a nice job of showing that Chinese exports have depressed some local labor markets. But unless I’m mistaken the paper doesn’t tell us anything about the macro effects of Chinese exports, which would require a macro model. Here are three possible ways that Chinese exports might hurt the aggregate economy:

1. It might depress aggregate demand

2. It might depress aggregate supply by reducing the long-term productivity of the US economy.

3. It might reduce aggregate supply by causing medium-term structural “reallocation” problems, as labor had trouble migrating to new jobs.

I’ll call these the AD shock, the AS/efficiency shock and the AS/reallocation shock channels. Even after reading the ADH paper, I am having trouble understanding which channel is relevant.

The easiest shock to address is the AD shock. EC101 students are sometimes confused by the GDP equation:

GDP = C + I + G + (Ex – Im)

This equation makes it look like a current account deficit would reduce GDP. However the CA deficit is exactly equal to the capital account surplus, which is I – S. So if we import more than we export, we also invest more than we save. Thus a CA deficit might boost investment, or if it reduces saving it might boost consumption. There is no “accounting argument” for the claim that trade deficits reduce aggregate demand.

There is a more sophisticated argument that CA deficits reduce AD, but only at the zero bound. Paul Krugman has suggested that when interest rates are zero, a CA deficit may depress the equilibrium interest rate, making monetary policy effectively tighter. Because we are at the zero bound, the Fed may not offset this shock and total AD may decline.

There is one big problem with this theory; it doesn’t apply to the 1990-2007 period considered in the ADH study. Interest rates were never at zero, and thus monetary offset clearly applied. Try to imagine a policy counterfactual involving a ban on Chinese imports. Unemployment was only 5.2% in June 1990, near the peak of the Reagan boom. By June 2000 it had fallen to 4.0%, near the peak of the Clinton boom. In the subsequent recession it never got higher than 6.3%, and then fell back to 4.6% in June 2007. Whatever you think about this data, the Fed clearly thought AD was adequate, or they would have eased policy further. Thus if a ban on Chinese imports did somehow boost AD, its effects obviously would have been offset by the Fed. I’m pretty sure that even Keynesians like Paul Krugman would agree with that claim. So I think it’s safe to assume that whatever the channel was by which China trade hurt the US economy, it was certainly not the AD shock channel.

The long run AS/efficiency channel also seems unlikely. Basic economic theory suggests that productivity and efficiency are highest when a country concentrates on producing those goods for which it has a comparative advantage. Thus the most likely channel would be the reallocation channel; something prevents workers who lost their jobs in one sector from quickly finding jobs in other booming sectors. And indeed ADH do frequently discuss the problem in exactly those terms, workers don’t seem to be able to easily reallocate out of areas hit by the China trade shock.

However there are also lots of puzzling observations that seemed to conflict with this interpretation:

In the German case, the impact of rising Chinese import competition between 1988 and 2008 was compounded by an even more rapid growth of imports from Eastern Europe following the fall of the Iron Curtain. Distinct from the U.S. case, German manufacturers sharply increased exports to these lower-wage countries, resulting in a more modest trade deficit with China and a trade surplus with the Eastern Europe. The unemployment gains related to these export opportunities roughly offset the job losses from import competition in the case of China, while actually raising German employment in the case of trade with Eastern Europe.

This makes no sense to me. Unless I’m misreading them, they seem to be suggesting that, unlike the US, the German labor market has not been hurt by recent trade patterns, because Germany runs a trade surplus. Thus job losses due to imports were offset by job gains due to exports. But that only make sense if the AD shock channel was operative, and as we’ve already seen the AD channel cannot possibly explain why China trade would hurt the US, on either theoretical or empirical grounds. I would add that German labor market data was far worse than US data during the 1990-2007 period, with unemployment rising from 5.6% in 1991 to 7.7% in 2000 to 8.6% in 2007. (I could not find 1990 data for Germany.)

The Economist also thought the ADH paper implied that trade deficits might be a transmission channel:

The costs of Chinese trade seem to have been exacerbated by China’s large current-account surpluses: China’s imports from other countries did not grow by nearly as much as its exports to other countries. China’s trade with America was especially unbalanced. Between 1992 and 2008, trade with China accounted for 20-40% of America’s massive current-account deficit; China imported many fewer goods from America than vice versa.

And the ADH paper says something similar:

The impact of China’s recent growth on the global economy is not just about the country’s long-run comparative advantage. Also important for the near-term labor market consequences of its trade expansion is that China’s trade surplus widened substantially.

But the Keynesian theory that trade surpluses overseas can cost jobs in the US (which only applies at the zero bound) also implies that the (roughly equal) German trade surplus was just as harmful as the Chinese surplus, even though Germany exports less to the US than China. The AD shock theory implies that overseas trade surpluses hurt us by increasing global saving and reducing velocity, thus bilateral trade patterns don’t matter. In that case the problem isn’t China, it’s everyone with trade surpluses.

If the AHD model were based on the AS/reallocation channel (which is the only channel that makes sense to me), then the German trade surplus would be irrelevant. It’s not obvious why it would be harder to reallocate German workers from import competing to export industries, than it would be to reallocate American workers from import competing to Boeing exports plus housing investment plus manufacturing aimed at the domestic market, as long as total AD was on target.

This also confuses me:

Two additional sources of linkages between sectors operate through changes in aggregate demand and the broader reallocation of labor. When manufacturing contracts, workers who have lost their jobs or suffered declines in their earnings reduce their spending on goods and services. The contraction in demand is multiplied throughout the economy, depressing consumption and investment. Helping offset these negative aggregate demand effects, workers who exit manufacturing may take up jobs in the service sector or elsewhere in the economy, replacing some of the earnings lost in trade exposed industries. Because aggregate demand and reallocation effects work in opposing directions, we can only detect their net impact on aggregate employment.

Again, unless I’m missing something, ADH seem to be suggesting an AD shock channel, which makes no sense.

They also don’t discuss all the jobs created in places like Seattle and Silicon Valley, as a result of China trade. Without exports, how would China be able to buy all those Boeing jetliners? In fairness, ADH do admit that their study may miss important linkages in high tech and business services, but this admission occurs only in a footnote:

A further issue is that measured input-output linkages may miss some positive demand effects from U.S. exports. Consider the iPhone, whose back panel states, “Designed by Apple in California. Assembled in China.” From its U.S. headquarters, Apple offshores production to Foxconn, which employs 300,000 workers in its iPhone operations in China. If productivity in Foxconn rises, iPhone sales may expand, thereby increasing demand for design services among Apple’s 50,000 US employees. However not all of Apple’s design exports to China may appear in U.S. trade data. For tax purposes, Apple may attribute some iPhone revenues to overseas subsidiaries. These revenues would not appear in the US current account until the earnings are repatriated, possibly far in the future. A similar logic applies to U.S. business services that may expand as a result of increased trade with China.

Elsewhere the anecdotes they use don’t even fit their hypothesis:

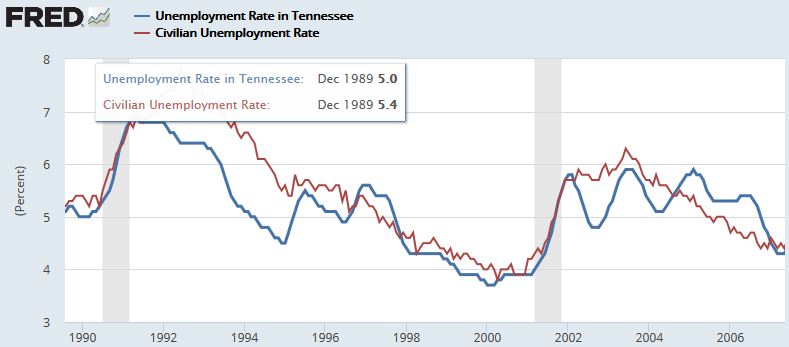

When looking within manufacturing, Tennessee, owing largely to its concentration of furniture producers, is far more exposed to trade with China than his Alabama, which has agglomeration’s of relatively insulated heavy industry.

The Atlantic interpreted ADH this way:

But that didn’t really happen. In Tennessee, few workers within the commuting zone of struggling plants moved away after their work prospects declined. Instead, unemployment rose both among manufacturing and nonmanufacturing workers, suggesting that the ill effects of increased trade had a spillover impact on the larger local economy. On top of that, average weekly wages declined. In general, places like Tennessee were very slow to adapt to the new economic reality–their elevated unemployment rates and diminished wages persisted for a decade, the paper’s authors estimate. The workers there are also saw a lower lifetime income.

That makes it sound like Tennessee’s economy really sucked during this period. In fact, the average unemployment rate was slightly below the national average:

Indeed the booming Tennessee economy has done far better than Alabama since 1990, drawing in workers from many other states. Population growth from 1990 to 2010 was 18.3% in Alabama, 24.1% in the USA and 30.1% in Tennessee. Why not choose Detroit as an anecdote? Perhaps because China doesn’t export many cars to the US. Indeed total Chinese exports were only 2.2% of US GDP in 2007. If Detroit has been hurt by trade, it’s been from Japan, Korea, Germany, Mexico and Canada, not China. (Although auto parts makers have been hit by China.)

Although Chinese exports are a small share of GDP, they are very important to the sort of low and middle-income workers who shop at places like Walmart. Trade with China has improved living standards for millions of Americans. These media reports seem way too pessimistic to me, unless I’ve completely misread the ADH paper. Tyler Cowen suggested:

This is some of the most important work done by economists in the last twenty years.

Maybe I’m missing something, but I don’t see that. We’ve always known that local labor markets can be hit hard by import competition, and thus ADH don’t really change our understanding of trade in any major way.

Interestingly, the Economist seemed to have a different interpretation from Noah Smith, arguing the ADH paper merely reduced the estimated net gains from trade, which remain positive:

But those benefits are only visible after decades. In the short run, the same study found, America’s gains from trade with China are minuscule. The heavy costs to those dependent on industries exposed to Chinese imports offset most of the benefits to consumers and to firms in less vulnerable industries.

On the other hand, there are also many good features in the ADH paper, as when they discuss how government benefit programs may slow the adjustment to trade shocks:

Workers eligible for TAA receive extended unemployment benefits of up to 18 months, as long as they remain enrolled in a training program, and may obtain allowances towards relocation, job search, and healthcare.

Overall, I had a lot of trouble making sense of this paper. To draw macro implications, you’d need a macro model, including assumptions about monetary offset to evaluate a counterfactual with no China trade. But I couldn’t find this model.

And who is the intended audience? The sort of economist who is most likely to be receptive to this message is not a free market supporter like me, but rather a left of center pragmatist. But people like Krugman and Summers were extremely skeptical of the claim that structural/reallocation theories explained high unemployment after 2008, and insisted that an AD shortfall was the real problem. I agree that AD was the real problem after 2008, which is one reason I am skeptical of this paper. But if you did dismiss the claims of people like Arnold Kling, that much of the unemployment was due to the difficulty workers had reallocating out of residential real estate construction, then why would you be receptive to the ADH paper?

I don’t want to sound too negative here. While I don’t buy the argument that trade is harmful in a macro sense, I do think ADH have done a good job of showing that labor reallocation may be harder than we assumed. This has lots of policy implications. We should be more skeptical of policies that slow reallocation, such as zoning restrictions on development and rent controls (both of which Steve Waldman recently defended), and extended unemployment compensation programs.

One of the things I liked most about the ADH paper was that they recognized the massive gains from trade to China. Thus even if the effects of trade on the US were slightly negative in net terms (which I doubt) the case for free trade would remain overwhelmingly powerful, at least unless you were a nationalist who opposed any sort of foreign aid, even aid that hugely boosted world efficiency.

The thing I liked least is the ambiguity about the model they were using. If they are right about the costs of reallocation, does it suggest that all “creative destruction” is bad, including technological progress? That would seem to be the implication, but I doubt they’d want to go that far. So why focus on jobs lost by the China shock, but not German exports or robots replacing workers? Early in the paper they suggest that China is special, as it was a once in a lifetime massive shock from a huge country, which hit us rapidly, but also that wages in China are now rising fast, so much of the adjustment is over. So even if they are right about China during 1990-2007, it probably has no policy implications going forward, as other types of creative destruction like rising German exports and robots tend to occur more gradually over time. And if I am too complacent about robots, then the policy implication of the paper is not anti-China (it’s too late to prevent that shock), but rather anti-robot, as robots might be the next massively disruptive shock.

Sorry to be so long winded, but I’m not seeing anyone seriously grapple with the implications of their research, if it is correct. I would appreciate any comments you might have.

READER COMMENTS

Swami

Feb 26 2016 at 6:29pm

“Early in the paper they suggest that China is special, as it was a once in a lifetime massive shock from a huge country, which hit us rapidly, but also that wages in China are now rising fast, so much of the adjustment is over. So even if they are right about China during 1990-2007, it probably has no policy implications going forward.”

Exactly. I was not impressed with Noah’s spin on the issue. I am not an economist, but I am familiar with Stolper/Samuelson and that economists have known for decades that increasing trade can increase the pace of creative destruction and create relative winners and losers. This doesn’t negate the benefits overall, long term of increasing free trade.

Effem

Feb 26 2016 at 8:28pm

People are looking in the wrong place for a trade “villain” as a link to inequality. It’s not trade that hurts, it’s protectionism. The gains of trade exist, but they have accrued to a narrow slice of “protected industries” that don’t have to compete with Chinese wages (services, housing, healthcare, IP).

If “trade” in IP or services were as free as most goods the wealth distribution would look very different. It’s pretty simple: those who compete with low-cost countries have lost, the rest have won.

Lorenzo from Oz

Feb 26 2016 at 9:57pm

The Autor, Dorn and Hanson paper did not work very well in making macro claims. This partly because economics has continuing difficulties connecting markets and institutions. In a way, the difficulties you are pointing to are cousins to economics’ failure to provide a robust explanation of long term economic growth which incorporates the dramatically different patterns we see historically and in the contemporary world.

The bit I liked about the paper seemed to me what you also liked; that there are gains from trade does not mean that particular localities and sectors did not suffer disproportionate costs from the massive expansion in trade with China. It undermines the tendency to glibly say “trade is good, why are you people complaining?”

Though the implicit and explicit trade deficit arguments are not sensible. I can remember when Japan was the trade bogey: Australia ran a major trade surplus with Japan (one Japanese trade minister told us to feel free to make it bigger), which ran a trade surplus with the US, which ran a trade surplus with Australia. Clearly, we were all better off, but it did not stop people pointing and complaining.

Japan also bought lots of American assets (the Rockefeller Centre was a great symbol). It typically paid way too much for them and the net result was one the largest peacetime wealth transfers in history–from Japan to the US. (Part of that being that Wall St saw the Japanese financial firms, used to a BoJ/Treasury Ministry “managed” financial market, coming and ate them alive.) I saw an estimate that, over about a decade, Japan managed to lose the equivalent of 1 year’s UK GDP on its foreign investments.

Personally, the US selling lots of printed pictures of dead Presidents for useful goods strikes me as a great deal. (The US using its comparative advantage in legally secure financial/saving options.) Just as the previous Americas-dominant global super power (the Spanish Empire) used its advantage in production of reliable silver coins to purchase lots of useful Chinese goods–its reason to colonise the Philippines.

But, to return to the paper, that does not mean that particular segments of the US economy are not suffering a negative trade shock.

TravisV

Feb 26 2016 at 11:18pm

Prof. Sumner, thank you for grappling, I’ve always supported free trade, glad to see Noah Smith had some questionable interpretations in this case.

Mark

Feb 27 2016 at 1:57am

Effem: “People are looking in the wrong place for a trade “villain” as a link to inequality. It’s not trade that hurts, it’s protectionism. The gains of trade exist, but they have accrued to a narrow slice of “protected industries” that don’t have to compete with Chinese wages (services, housing, healthcare, IP).”

Or protected ‘slices’ within industries. Many US manufacturing industries are burdened with ‘pro-labor’ policies and unions that make hiring as difficult as firing. I would be interested to see if the industries whose workers Smith claims are least able to find comparable jobs also happen to be industries with the most constricted labor markets.

Lorenzo from Oz:”It undermines the tendency to glibly say “trade is good, why are you people complaining?”

I actually still feel justified in making that glib proclamation. Sure, some people suffer; when I buy Sierra Mist instead of Sprite, Sprite’s poor employees suffer. I think the argument for free trade, like free choice of lemon-lime soda brand, is not that no one suffers, but that there is less net suffering than if trade were restricted. I don’t think Noah Smith even tried to argue that point. I think he and other protectionism sympathizers are just perpetuating the logical (or perhaps I should say ethical) fallacy that the suffering of unspecified faceless consumers paying higher prices or unspecified faceless employees of erstwhile exporting firms as a result of trade restriction is not worth as much as the suffering of known, specified workers at a plant in Dearborn whose jobs we can directly observe being lost due to competition with China.

Dustin

Feb 27 2016 at 9:31am

Lorenzo, “The bit I liked about the paper seemed to me what you also liked; that there are gains from trade does not mean that particular localities and sectors did not suffer disproportionate costs from the massive expansion in trade with China. It undermines the tendency to glibly say “trade is good, why are you people complaining?””

I completely agree with this, but it also seems quite obvious. My understanding of the relative impact of free trade are, summarily:

– The net exporter (China): positive

– The net importer (U.S.): positive, perhaps less so than the net exporter

– Disrupted worker (U.S. worker in industry exposed to the net exporter): negative

The referenced paper doesn’t seem to provide any new insight.

Swami

Feb 27 2016 at 12:19pm

Mark,

Adding on to your comment…

I see the market controversy as similar to defecting at a prisoners dilemma game. Everyone alive in the US is the beneficiary of a system of 250 years of creative destruction with median living standards thirty to one hundred times higher than those not taking the creative destruction path.

But, everyone can do even better if they defect and privilege themselves (always for really good reasons) to not be subject to competition. Thus the Sprite employee finds a great reason to prevent us from buying Sierra Mist. And so on.

Of course if we all defect, we go back to three dollars a day and life spans half of what they are now and a planet with six billion fewer people.

Michael Rulle

Feb 27 2016 at 12:22pm

Maybe ADH are trying out to be Trump’s economic advisors.

Lower prices for all has to be beneficial in some way. Perhaps you mentioned this, but if certain areas have been hurt by competitive imports, isn’t there likely to be migration to other areas? ADH claim they factored that into their study. I know you need to take what they say seriously, which is your job, but guys like me don’t have too.

The auto industry in the US was so bad in the 1970s, that within 10 years the Japanese and Germans blew it up. Now American and foreign companies make great cars on a price adjusted basis and real prices have lowered. I read that even nominal prices have lowered—-not sure how it was calculated. Would we have been better off had we put high tariffs on auto imports? No.

Plus, ADH implicitly use correlations to make their point, but more is happening than trade deficits with China. I suppose it is interesting to try and challenge an accepted theory, so I give them credit for that, I guess. But to me it is obviously wrong headed—-and worse, very irritating.

Charlie

Feb 27 2016 at 12:34pm

Dustin,

You have the signs right, but the magnitudes are quite important as well. Previous studies had found the transitional cost of workers much less.

ThomasH

Feb 27 2016 at 3:02pm

Scott,

I don’t think the point of ADH is all that difficult to ferret out. The benefits from movements toward freer trade are not uniformly distributed and indeed can be negative for some people. (Benefits are less if the Fed fails to maintain constant NGDP growth, of course.) Trade is not different from technological change, which can also have some looses as well as winners. The question is do we try to prevent the trade/technological change or do we try to have a system that incurs that those who “loose” still benefit from aggregated gains through general redistributive measures like subsidized health insurance, publicly finance education, EITC, retraining, child care credits, etc.

Dustin

Feb 27 2016 at 3:37pm

ThomasH

That’s what I thought as well. I haven’t read the paper ($5 pay wall) found the following excerpt in the abstract:

“At the national level, employment has fallen in U.S. industries more exposed to import competition, as expected, but offsetting employment gains in other industries have yet to materialize.”

This suggests, as I read it, that free trade with China is a to date a net negative for the U.S.

Dustin

Feb 27 2016 at 3:38pm

FWIW The long-windedness was totally worth it. Demanding post (for me) to parse, but one the kicks the tires on the ADH claim to test for coherency.

David R. Henderson

Feb 27 2016 at 5:19pm

@Scott Sumner,

OUTSTANDING post. Like Dustin above, I did not find it too long-winded at all. It flows beautifully.

Scott Sumner

Feb 27 2016 at 5:53pm

Thomas, You said:

“I don’t think the point of ADH is all that difficult to ferret out. The benefits from movements toward freer trade are not uniformly distributed and indeed can be negative for some people.”

I don’t think so. But if you are correct then the paper is basically worthless, as we knew that already. Why are people saying it’s such an important paper? Why do people like Noah Smith have a completely different interpretation than you have? (BTW, I don’t think the paper is worthless, but then I think there is much more to it than you suggest.)

Everyone (including Thomas), thanks for all the comments. I mostly agree so I won’t reply to each one individually. I’m not at all certain that I am correct, but I hope to get some pushback, because if I am correct then it’s an important post.

Lorenzo from Oz

Feb 27 2016 at 9:22pm

Mark: I think you are slightly missing the point I was trying to make. It was not an argument against free trade, it was an argument against not paying attention to folk hurt in the process.

Dustin: no new (useful) insight, just some useful identification and quantification.

Prakash

Feb 28 2016 at 1:02am

I’m with Henry George on this.

Have free trade and ensure that idle land value gain is kept to a minimum with a decent land value tax. When people are subject to lowering wages and high land value, that’s just nasty. Ideally, the gain in rents are transferred to the public via a citizens dividend or a wage subsidy. If that happened, the average person has a much higher chance of appreciating free trade.

ThomasH

Feb 28 2016 at 8:11am

@Lorenzo

Are ADH even attempting to draw macroeconomic conclusions?

@Mark

To point out that Group X has been harmed by policy Z that increases trade in a particular way does not imply that increasing trade or even that policy Z is mistaken. Noah Smith did not draw that conclusion. He just argued against conflating the idea that trade is beneficial in the aggregate and at the relevant margin with the idea that everyone benefits. If some people benefit from Policy Z and others do not (and particularly if the one who do not have lower consumption), it implies that there might be a policy Z’ or a combination of policy Z + Policy Q that ensures that more of the aggregate gains from Z are more widely distributed, e.g., to those with lower consumption.

@ Dustin

That trade with China has reduced employment in certain industries that has not been compensated by other “industries” does not mean that the US consumers as a group have not benefited. Moreover, any effects that depend on less than total employment of resources would have to be made contingent on Fed policies.

@ Scott

Let me have another look at Noah’s interpretation. I sometimes (mis)interpret people as being more sensible that they are.

Dustin

Feb 28 2016 at 9:29am

ThomasH,

The benefit of trade for the U.S. (the country as a whole, not just consumers) arises from comparative advantage. If U.S. employment hasn’t shifted to compensate industry decay, then the benefits of trade haven’t accrued. This is what the ADH paper claims.

Shifting a segment of your population to the unemployment book in exchange for marginally cheaper prices for the remaining employed population is, at very best, a wash.

ThomasH

Feb 28 2016 at 9:36am

@Scott

After re-reading Smith.

Smith: It is expensive and time-consuming for workers to train for new jobs and to move to new locations. It also takes time and money for businesses to figure out how to change their business models in response to the new landscape presented by a global economy with China in it. These adjustment costs might overwhelm the gains from trade.

Sumner: I do think ADH have done a good job of showing that labor reallocation may be harder than we assumed.

I don’t think these are two statements are so very different. I do agree that Smith should have mentioned that that the adjustment costs were made greater by failure of the Fed’s monetary policy and government’s fiscal policies (departure from the NPV rule).

But the real issue is what policy conclusion to draw? Does it mean that we should start restricting trade or other forces of “creative destruction?” Or should we try to make the economy more resilient to minimize adjustment costs (better regulation of urban land use, etc, governments investing according to an NPV rule, Fed targeting of NGDP) and redistribution policies to make sure that gains from economic change are widely dispersed (a more robust safety net, replacement of wage and business taxes with a progressive consumption tax), realizing that in the real world of politics, sometimes there are trade-offs between those goals.

Mark

Feb 28 2016 at 1:32pm

@Dustin: How can one conclude from this that the benefits trade with China has conferred to Americans as consumers by increasing our purchasing power don’t outweigh these supposed losses in employment? Employment isn’t the only factor to be considered when assessing the net impact of trade.

I will also reiterate my earlier point about constraints imposed on labor markets. Some say the main take-away from this paper should be that some domestic industries inevitable suffer from free trade, with the implication that some social insurance system is the only remedy; instead, we might ask the question, why are these industries so effected by trade with China?

In cases like the auto industry, (though competition there isn’t specifically with China, more with Japan), policies (and unions) intended to help workers have driven up labor costs and rendered those industries less competitive with other countries.

I wouldn’t be surprised to see the same problem behind this situation here. Policies, either state policies or union policies, make it difficult or impossible to reduce worker compensation in order to stay competitive in a global economy, so employment falls instead. And since what manufacturing jobs remain in the US are pretty well-compensating, I’d say they could afford pay cuts to boost employment. So perhaps the answer is to actually let domestic employers reduce wages or compensation so they can actually compete with China and afford to employ more workers. And of course it wouldn’t hurt to eliminate barriers to entry into such industries to increase competition on the employers’ side.

Dustin

Feb 28 2016 at 4:14pm

Mark,

I think of it this way: if aggregate demand remains stable after enacting free trade, which is a reasonable assumption, then the benefits enjoyed by consumers directly offsets the loss paid by disrupted workers. In other words, the cumulative incremental benefit of cheaper prices to U.S. consumers is equal to the aggregate loss of wages for displaced U.S. workers. While this scenario may be a net zero in terms of GDP, I would argue that the increased inequality would be strongly negative.

The only way that cheaper prices alone could equate to a net benefit is if trade results in an increase in aggregate demand, which I don’t think can be assumed. I agree with the rest of your comment.

All that said, I’m not an economist or trade economist and could be way off 🙂

Mark

Feb 28 2016 at 7:04pm

Dustin,

Wouldn’t the effect free trade has on inequality depend at least in part on which industries are subject to international competition? So, if the average disemployed worker has a significantly higher income than the ‘average consumer’ of the goods he use to produce (which are now more cheaply produced in China), then wouldn’t this be a transfer of wealth from the higher-income worker to the lower-income consumer? If we’re talking about manufacturing, in older times it might have been safe to assume the average worker was poorer than the average consumer, but I don’t think it is a safe assumption in the US today.

But I guess I’m saying that whether free trade in this case would worsen or alleviate inequality would depend on whether (or how much) wealthier or poorer the laborers producing the good whose production is being outsourced are than the American consumers of that good are.

I too am not an economist. I just assume that’s why Scott’s here, to correct us if we’re way off.

Scott Sumner

Feb 29 2016 at 9:31am

Thomas, Sorry, but you need to reread Noah Smith again. The whole point of his article was that economists were wrong about free trade being good. Not to a subset of workers, but for the US as a whole. His post is very critical of the standard economist position that free trade is good.

But ADH present no solid macro evidence to support that position. Are some workers hurt by imports? Obviously, but that fact is already in every single EC101 textbook.

It is misleading for you to single one one thing Smith said that agrees with one thing I said. The thrust of his Bloomberg article is almost the opposite of mine.

Dustin, You said:

“I think of it this way: if aggregate demand remains stable after enacting free trade, which is a reasonable assumption, then the benefits enjoyed by consumers directly offsets the loss paid by disrupted workers. In other words, the cumulative incremental benefit of cheaper prices to U.S. consumers is equal to the aggregate loss of wages for displaced U.S. workers. While this scenario may be a net zero in terms of GDP, I would argue that the increased inequality would be strongly negative.”

This is wrong. If you hold AD constant, and prices fall, then by necessity real GDP must rise.

I do find your claim of increased inequality to be possible (but not certain). But ADH seem to be assuming that real GDP falls, as there are no employment gains to offset the job losses to imports.

pyroseed13

Feb 29 2016 at 9:41am

How much of this employment disruption could be alleviated with labor market and land use deregulation? Furthermore, and admittedly I haven’t read the paper yet, why are people only comparing the benefits of consumers to those workers subjected to import competition? There are benefits to investment as well. China has and currently is undertaking massive investments in the U.S., particularly as their economy appears to be sputtering.

That being said, I think economists need to find a better way to communicate the benefits of trade. As someone else noted in the comments, glib responses aren’t likely to win you many fans.

Dustin

Feb 29 2016 at 1:48pm

Thanks for the response, Scott. You said: “This is wrong. If you hold AD constant, and prices fall, then by necessity real GDP must rise.”

That makes perfect sense to me and actually was the basis of my belief/hunch. I viewed the rise in RGDP as a result of increased Consumption by the remaining employed. So basically, the remaining employed enjoy greater real consumption, given lower prices and thusly holding AD constant, at the expense of lower real and nominal Consumption by the disrupted and unemployed.

In any case, this is a bit out of my league, so I don’t want to linger on too much. I’ll reread your post and see if it clarifies some of the logic.

Lorenzo from Oz

Feb 29 2016 at 6:55pm

“@Lorenzo

Are ADH even attempting to draw macroeconomic conclusions?”

I meant “macro” simply in the sense of “big” or “aggregate”.

Pyrmonter

Mar 1 2016 at 2:32am

A few thoughts and questions re ADH, but which raise issues in what might grandly be called “open economy market monetarism”.

Like Lorenzo, I see this from an Australian perspective; for what its worth Australia has had a long history of protectionism which has seen a lot of ink spilt in the cause of arguing against trade: sometimes by economists, more often by those on the fringe of the profession making the very arguments of insincerity Noah Smith makes. I think I perceive some of those ideas having jumped the Pacific.

1 Why focus on the bilateral trade with China, rather than the overall US trade position? The US trade deficit is not the same as the US-China trade deficit; surely the comparison should be with an economy in which the growth in the US-China deficit was offset by increased US exports to third countries through a lower real exchange rate, achieved by tighter fiscal and somewhat looser monetary policy. If that’s the nub of the ADH macro point, it’s not terribly profound; nor is it novel.

2 The US-China trade growth is not the only instance in history of a explosive growth in trade: due to the interruptions of shipping, the two great wars of the twentieth century present alternative natural experiments; albeit ones that had somewhat less impact on the US (the traded sector of which was comparatively smaller than those of the other advanced economies). What, if any, evidence is there of, for example, the impact of EU expansion?

3 ADH seem to assume comparative labour immobility – behaviour more akin to Europe than the US. They don’t observe any trend; yet there are factors relevant to labour mobility: welfare availability, housing cost – that have changed in time: do they posit that these are irrelevant to adjustment?

Jacob Aaron Geller

Mar 1 2016 at 11:23am

Scott,

My best guess is that ADH has (briefly) caught on because a) it’s topical and b) the evidence that trade has heterogeneous effects is old enough that even very fine (but intellectually omnivorous) economists like Noah and Tyler sort of like forgot about it, so ADH feels new.

Re: point a, have you seen the “Donald Trump saying China” supercut on YouTube? I don’t think anything like that existed, or would have been funny, even 1 year ago.

Re: point b, Winters et al did a literature review in 2004 on trade and poverty pointing to the evidence of heterogeneous impacts of trade. I haven’t seen it discussed much since then.

Assaf

Mar 1 2016 at 8:40pm

You focus, correctly I think, on the theoretical problems with concluding from the results of the paper to the macro level. But there’s also a major empirical issue: at heart, the empirical results of this research agenda are fancy dif-in-dif. ADH compare parts of the U.S. that were very exposed to trade with China, to parts that were not. It is therefore a key empirical assumption for ADH that areas not directly exposed to trade are what all of the U.S. would have looked like if it wasn’t for the increase in trade with China. You gave a whole bunch of reasons why that’s a bad assumption.

The empirical specification is designed so that it cannot be used as a basis of macro statements. the whole point of the empirics is comparing areas in the US to one another. When You are measuring a difference, you cannot argue that this difference is entirely a negative effect on the areas exposed to trade. It is equally valid, in a technical sense, to argue that this is the positive effect on other areas.

Eric Rasmusen

Mar 1 2016 at 10:25pm

That workers whose wages fall because of imports don’t recover isn’t surprising at all. Their wages *should* fall in equilibrium. The gains from trade are to other factors of production and to consumers.

Scott Sumner

Mar 2 2016 at 4:26pm

Thanks everyone–have been traveling the last few days, will respond tomorrow

Scott Sumner

Mar 3 2016 at 11:46am

Everyone, Thanks for the comments, I’m going to do a brief follow up post, to hopefully clarify things.

Jacob, Good point, although It’s hard to believe Tyler forgot this, does he ever forget anything?

Yup, I saw the China clip. I recall reading that the Chinese people tended to favor Trump, until his actual views were explained.

David Stinson

Mar 10 2016 at 10:21am

Well, a couple of things. First, there is no reason to think this situation suddenly righted itself in 2008 as the financial crisis hit.

Secondly, what matters is not just the zero bound, but expectations thereof. It’s harder to get out of a liquidity trap when expectations are that the central bank will fail in creating positive inflation. And markets will be on edge when a longer/more severe collapse is a possible.

That sort of debt/deflation cycle is what can happen when there is more debt backed by less economic activity. So going through the counterfactual, the issue is currency manipulation. China buys up US debt, and it is unlikely to have an offsetting effect elsewhere unless policy makers are careful not to pay attention to market signals. At the same time, the RMB goes lower, so fewer US exports and jobs generated through exports. So it’s a roundabout effect, largely psychological, but very important.

Alan Patterson

Mar 27 2016 at 5:39am

I wonder how many of the authors of comments have lost their jobs or businesses because of increased competition brought about by lowering trade barriers.

Let’s assume that there have been losses but there is, globally, a net benefit. The question arises as to whether there should be compensation. In other words, should the beneficiary of the losses receive the gross benefit or merely the net benefit?

Comments are closed.