Who Is Harmed by Insider Trading?

By Charles L. Hooper

“Uninformed Buyer has no legitimate gripe with anyone. Insider merely nabbed the dumb-luck windfall from Uninformed Buyer.”

In December 2014, the Second U.S. Circuit Court of Appeals in New York reached an important decision on insider trading.1 Specifically, the judges, in a 3-0 decision, stated the following:

We agree that the jury instruction was erroneous because we conclude that, in order to sustain a conviction for insider trading, the Government must prove beyond a reasonable doubt that the tippee knew that an insider disclosed confidential information and that he did so in exchange for a personal benefit. Moreover, we hold that the evidence was insufficient to sustain a guilty verdict against Newman and Chiasson for two reasons. First, the Government’s evidence of any personal benefit received by the alleged insiders was insufficient to establish the tipper liability from which defendants’ purported tippee liability would derive. Second, even assuming that the scant evidence offered on the issue of personal benefit was sufficient, which we conclude it was not, the Government presented no evidence that Newman and Chiasson knew that they were trading on information obtained from insiders in violation of those insiders’ fiduciary duties. (italics in original)

Their decision is widely expected to make prosecutions for insider trading more difficult for the federal government. Indeed, in late January, in response to the December decision, federal prosecutors announced their plan to drop charges against five men whom they had accused of insider trading.2

See also Charles L. Hooper’s previous article, “Insider Trading Turned Inside Out”. Library of Economics and Liberty, June 2, 2014.

How should economists think about insider trading?

Economists have long known about the beneficial effects of insider trading. Up-to-date information is crucial for the proper functioning of a stock market, and insiders trade when stock prices, reflecting stale information, have diverged from reality. Insiders trade on newer information, nudging share prices toward reality and improving stock market efficiency. Still, it raises a thorny question: If insider trading is beneficial, where does the insider’s newfound wealth come from? Doesn’t it come from other investors who have been harmed? Why is it economically and morally acceptable for the insider to pocket the returns that would have enriched others?

Those are good questions, but careful analysis shows that, contrary to the popular view, investors who lose when insiders trade are even less deserving of the windfall profits than the insiders themselves. Insider-trading laws can be seen for what they truly are: governments pushing mistaken notions of fairness and punishing victimless “crimes.”

For our specimen, we will examine the December 2014 acquisition of Cubist Pharmaceuticals by Merck & Co. for $9.5 billion, or $102 per share. Before the deal was announced, Cubist shares closed at $74.36. The next day, shares closed at $100.60.3 Insiders who traded on this information—and I know of no suspected insider trades—could have made a 35-percent return in a matter of days. Trading in options would have been even more lucrative. The appeal of insider trading is obvious.

The share price of all publicly traded stocks varies throughout the day and across days. For the sake of this example, however, consider a stock—here, Cubist—with a steady price of $74.36 for days, with no bid/ask spread. In other words, all transactions take place at exactly $74.36, with buyers and sellers meeting at that exact price and trading shares.

Assume, further, that all relevant information about Cubist was widely known before the acquisition. What can we infer? All buyers at $74.36 liked the prospects of the company and preferred to own Cubist shares over cash, bonds, or the shares of other companies. Sellers either did not like the prospects of Cubist or preferred their assets to be in cash or other investments, while some sellers simply needed cash for living expenses or large purchases.

The key point is that each transaction had a buyer on one side who preferred shares to cash and a seller on the other side who preferred cash to shares. Because investors were presumed informed and all key information was public, let’s call these investors Informed Buyer and Informed Seller. Why would one sell while the other was buying, even though they had the same information? They must have faced different situations, had different preferences, and/or, perhaps, had different assessments of the future. Because of their differences, each transaction benefited both investors. One avenue by which the stock market makes buyers and sellers wealthier is through the simple facilitation of trades that improve the circumstances of each party.

Interestingly, Informed Buyer and Informed Seller ceased to exist when Merck entered closed-door negotiations with Cubist, as these investors were suddenly deprived of important information as the actual and “true” share prices diverged and Cubist shares were temporarily mispriced. With the negotiations progressing, shares in Cubist continued to be traded at $74.36 per share—no new information was available to drive the share price higher or lower—and, hence, all subsequent investors must be labeled Uninformed Buyer and Uninformed Seller. Had they possessed that material information, they might not have bought or sold; and if they had chosen to buy or sell, they might have done so at a different price. In our example, they do trade, and Uninformed Buyer purchases Cubist shares from Uninformed Seller at $74.36 per share.

We need to introduce another investor, called Insider—a corporate insider employed by either Merck or Cubist, who is in the process of buying Cubist shares at $74.36, hoping to sell them later at a profit.

First, consider the case in which Insider buys a miniscule proportion of Cubist’s average daily volume. The daily volume of Cubist was approximately 600,000 shares before the deal, which, at $74.36 per share, was $44.6 million per day. Assume that Insider purchases $100,000 of Cubist stock.

Remember that most employees are not millionaires, and even millionaires might have a hard time coming up with $100,000 on short notice. Some actual insider-trading prosecutions involve relatively small amounts of money. In August 2012, for example, the U.S. Securities and Exchange Commission (SEC) charged eight people with making half a million dollars via insider trading on Chattem stock.4 That’s less than $65,000 per person, and the total amount was only 0.03 percent of the $1.9 billion acquisition of Chattem by Sanofi-Aventis.5 Admittedly, many cases do involve larger sums; Mathew Martoma was convicted in February 2014 of illegal trading in two pharmaceutical companies for a total value of $275 million.6

In our example, Insider’s purchases will be only 0.2 percent of Cubist’s volume for one single day. It’s hard to imagine Insider’s actions affecting the share price of Cubist more than infinitesimally. In this case, Insider will end up buying the shares from Uninformed Seller—shares that would have gone to Uninformed Buyer. Later, after the news becomes known and the share price jumps to $100.60, Uninformed Seller will kick himself or herself for selling at $74.36. But Uniformed Seller was going to sell at $74.36 anyway, to Uninformed Buyer, to Insider, or to someone else. Insider did not harm Uninformed Seller in any way whatsoever. Uninformed Seller wanted to sell and someone—in this case, Insider—obliged.

If Uninformed Seller has a beef with anyone, other than with Insider for not purchasing more shares, it is Cubist and Merck, who knew this material information but chose not to disclose it until later. These two companies created the situation in which the true value of Cubist was higher than the market price. However, both Cubist and Merck acted within their rights. Why would companies choose to disclose information later rather than sooner? There are many reasons, two of which are the possibility of the deal falling through and the administrative matters that must be handled before such news is announced.

The true “loser” is Uninformed Buyer, who would have purchased these shares had Insider not stepped in. But notice two things. First, Uninformed Buyer could have persisted and purchased other shares at $74.36, or very close to it—say, at $74.37 or $74.38. If Uninformed Buyer really wanted those shares, he or she could have easily purchased them. Second, consider Uninformed Buyer’s name—Uninformed. Uninformed Buyer was acting on old information. Had he or she bought at $74.36 and sold shortly thereafter at $100.60, Uninformed Buyer’s profit would have been due to pure dumb luck. It would be hard to argue that Uniformed Buyer earned or deserved that windfall. Someone was going to get that windfall, but what claim did Uninformed Buyer have to it? Also, we are considering the case in which the price of Cubist rose. Had the new information been bad, Uninformed Buyer would have lost money due to bad luck. Either way, Uninformed Buyer was relying on luck, plain and simple, and was not performing any valuable service—was not helping others more than some random buyer would have—by buying those Cubist shares.

Uninformed Buyer has no beef with Cubist or Merck. If the companies had released information about the acquisition before Uninformed Buyer tried to purchase shares, the share price would have jumped so quickly that it’s doubtful that Uninformed Buyer could have acted swiftly enough to profit.

In the case of small insider-trading amounts, Insider does not hurt Cubist, Merck, or Uninformed Seller. Insider does hurt Uninformed Buyer, but only to the extent that Uninformed Buyer didn’t persist and buy the shares anyway, and Insider snatched Uninformed Buyer’s dumb-luck windfall.

What happens if the amounts are larger? What if, instead of $100,000, the insider buys, say, $15 million in Cubist stock? That $15 million purchase would be a third of Cubist’s daily trading volume (about 200,000 of 600,000 shares), which sounds like a lot, but 31,715,300 shares traded hands on December 8 when the price jumped from $74.36 to $100.6. If the effect of the $15 million purchase is proportional,7 the share price of Cubist would have climbed 17 cents to $74.53. What would happen then?

Uninformed Seller was happy selling at $74.36 to Uninformed Buyer. Uninformed Seller, upon seeing the price of Cubist jump 17 cents, might become suspicious, refrain from selling and, instead, hold on to those Cubist shares. However, let’s assume that Uninformed Seller sells at $74.53, happy to make 17 cents per share more than expected. Uninformed Seller is clearly better off.

Uninformed Buyer, who decided not to buy at $74.36, clearly won’t buy at $74.53. Again, Uninformed Buyer could have persisted and purchased at $74.53 but chose not to, missing a windfall.

Uninformed Seller’s only gripe is with the two companies for not disclosing the information earlier and with Insider for not purchasing more shares. Uninformed Buyer has no legitimate gripe with anyone. Insider merely nabbed the dumb-luck windfall from Uninformed Buyer. And Insider has performed a valuable function by making the share price of Cubist closer ($74.53 instead of $74.36) to the ultimate value of $100.60 and by disseminating information in the process.

The more Insider buys—perhaps Insider purchases $100 million or $1 billion of Cubist stock—the sooner Cubist’s share price reaches its ultimate value of $100.60. Insider’s actions foreshadow the ultimate market event: Cubist’s and Merck’s announcements of the acquisition. Insider’s actions are, in essence, a pre-press release and, if the market benefits from the official press release, it also benefits from the pre-press release.

Insider “hurt” Uninformed Buyer by nabbing Uninformed Buyer’s unexpected and unearned windfall. How can Insider be less deserving than someone who isn’t deserving at all? Insider, after all, is making the stock market more efficient by disseminating important information, while Uninformed Buyer’s actions are equivalent to background noise.

Insider does not harm Cubist or Merck unless Insider makes a big purchase before the $102 price is fixed. In this case, Insider would help Cubist and hurt Merck in equal measure. If Cubist and Merck felt harmed, they could release the information earlier, effectively taking away Insider’s power. In addition, Merck and Cubist have it within their power to control such disclosures through contracts with their employees—through the common law.

Companies can enact their own prohibitions against insider trading, but, as it turns out, few have. If businesses don’t care, the government should care far less. It is possible that companies have neglected to actively enforce insider-trading rules because the government already does so vigorously. Note, however, that the government’s enforcement zeal has crystalized only in the last few decades, years after the SEC used Rule 10b-5, a catch-all provision against securities fraud, in its famous 1960s Texas Gulf Sulphur case.8 It is revealing that in Texas Gulf Sulphur the inside trader, Charles Fogarty, was later promoted to chief executive officer.9 Clearly, the board of directors did not consider Fogarty’s actions detrimental to the company. Some might argue that it would be difficult for Merck or Cubist to police insider trading by their employees, but that’s another way of saying that the costs of trying to prohibit insider trading might not be worth the benefits. Moreover, if the SEC ceased leading insider-trading cases, it could still assume a supporting role by helping companies develop cases against employees.

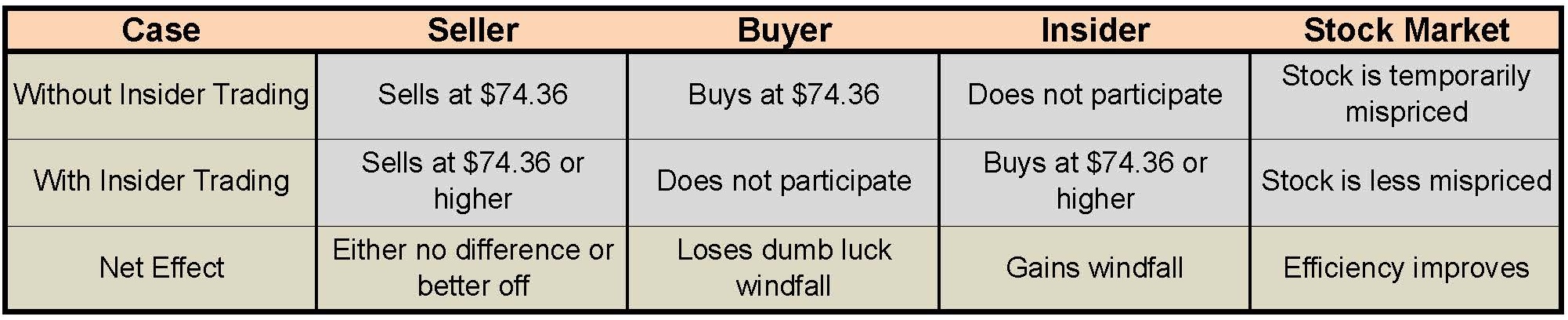

The following table summarizes the effect of insider trading on the stock market and other market participants. Insider nabbed the windfall that was headed Uninformed Buyer’s way. It was bound to land in someone’s lap, and since Uninformed Buyer did nothing to earn or deserve this windfall, why not direct it to toward someone making the stock market more efficient?

Does my reasoning mean that no one is ever hurt by insider trading? That issue is in dispute. In “Insider Trading,”10 David Haddock points to the valuable role of specialists, people that “the stock exchange appoints to ensure that a buyer of a particular security listed by the exchange can readily find a seller, and vice versa.” These specialists charge a bid-ask spread to cover their costs, and it is conceivable that “specialists will insist on larger bid-ask spreads if insider trading is widespread.” That bid-ask spread is a trading cost to investors.

However, “econometric attempts to find a relationship between the bid-ask spread and the risk of insider trading have been inconsistent and unreliable.”11 A specialist’s job, after all, is bringing together buyers and sellers. Insiders can be buyers or sellers, but they look like regular buyers and sellers to the specialist: they simply want to be connected to other buyers or sellers to conduct their trades.

There is another group that is conceivably hurt by insider trading: the quasi-insiders known as stock market professionals—investment bankers, stock analysts, arbitrageurs, hedge fund managers, portfolio managers—who acquire public and nonpublic corporate information in the course of their work. They trade either as quasi-insiders or, like the rest of us, as regular sellers and buyers. We have already discussed the regular cases above. Regarding their quasi-insider trading, surely the law was not intended to protect some insiders from others. Or was it? Daniel Goelzer, former general counsel of the SEC, stated that the ban on insider trading is justified because insider trading “threatens the orderliness and stability of markets by exposing market professionals to substantial losses.”12

Indeed, market professions do benefit from the SEC’s enforcement focus on true insiders because it takes them out of the crosshairs. Haddock and Jonathan Macey write:

For the first time at least one interested group, market professionals, had an incentive to replace their request for regulatory forbearance with a demand for a greatly enhanced enforcement effort. This was because the Supreme Court for the first time had made it clear that although true insiders would be barred from trading on the basis of information they acquired in the course of their official duties, those who acquired nonpublic information through the traditional financial investigations by investment bankers would not be subject to liability for violating the rules against insider trading. Investment bankers and other professional information processors began demanding a greater enforcement effort by the SEC, and they got it.13

Insider trading laws are yet another example of government’s desire to capture and exercise political, regulatory and legal power, gain huge monetary awards, and garner favorable PR, all for the sake of prosecuting victimless “crimes” and promoting misplaced notions of fairness. Insider trading should be embraced for its beneficial effects on market efficiency and left as a private matter for those companies interested in preventing it. Consequently, the SEC should not have a leading role in insider-trading cases, especially if the purpose is to benefit one group of insiders at the expense of another.

United States v. Todd Newman, Anthony Chiasson, decided December 10, 2014, at: https://s3.amazonaws.com/s3.documentcloud.org/documents/1377408/insider-trading-convictions-overturned.pdf

Christopher M. Matthews, “Insider Charges Are Being Dropped,” Wall Street Journal, January 30, 2015, C1, at: http://www.wsj.com/articles/justice-department-drops-insider-trading-charges-1422571552

Yahoo! Finance, search: Cubist Pharmaceuticals (CBST) daily prices from Oct. 25, 1996-present: http://finance.yahoo.com/q/hp?s=CBST+Historical+Prices

“SEC Charges Eight in Georgia-Based Insider Trading Ring,” SEC website, August 28, 2012, at: http://www.sec.gov/News/PressRelease/Detail/PressRelease/1365171484100

“Sanofi-aventis to Acquire Chattem Inc., Creating a Strong U.S. Consumer Healthcare Platform,” PR Newswire, December 21, 2009, at: http://www.prnewswire.com/news-releases/sanofi-aventis-to-acquire-chattem-inc-creating-a-strong-us-consumer-healthcare-platform-79790802.html

Nate Raymond, “SAC Capital’s Martoma found guilty of insider trading,” Reuters, February 6, 2014, at: http://www.reuters.com/article/2014/02/06/us-sac-martoma-idUSBREA131TL20140206

$15 million at $74.36 per share is equal to 201,721 shares. 31,715,300 shares traded hands on December 8 when the deal was announced, lifting the share price from $74.36 to $100.60. 201,721 shares is 0.64% of 31,715,300 shares. If the price rise is proportional—a big assumption—the $15 million purchase would raise the share price by 17 cents. Regardless, the magnitude of the price change does not change the argument.

Stanislav Dolgopolov, “Insider Trading,” in David R. Henderson, ed., The Concise Encyclopedia of Economics, 2nd Edition, 2008 http://www.econlib.org/library/Enc/InsiderTrading.html

David D. Haddock, “Insider Trading,” in David R. Henderson, ed., The Concise Encyclopedia of Economics, 1st Edition, 1993 http://www.econlib.org/library/Enc1/InsiderTrading.html

Haddock, “Insider Trading.”

Dolgopolov, “Insider Trading.”

David Haddock and Jonathan Macey, “Regulation on Demand: A Private Interest Model, with an Application to Insider Trading Regulation,” Journal of Law and Economics 30 (1987).

Haddock and Macey, “Regulation on Demand.”

*Charles L. Hooper is president of Objective Insights, a company that consults for pharmaceutical and biotech companies.

Disclosure: I worked at Merck two decades ago, and both Merck and Cubist have been clients of my company, Objective Insights. I owned shares in both Merck and Cubist until recently, when I sold my Cubist shares to Merck for $102 per share. I knew nothing of the acquisition beforehand and have never traded as an insider.