Capital Gains Taxes

By Stephen Moore

What Is Capital?

The term “capital” refers to produced goods used to produce future goods. Even a corner lemonade stand could not exist without capital; the lemons and the stand are the essential capital that makes the enterprise operate. A recent study by Dale Jorgenson of Harvard University discovered that almost half of the growth of the American economy between 1948 and 1980 was directly attributable to the increase in U.S. capital formation (with most of the rest a result of increases and improvements in the labor force).1

Capital can also refer to technological improvements or even the spark of an idea that leads to the creation of a new business or product. In 1975, when Bill Gates decided to form a computer software company and then brought MS-DOS to market, he created capital. Investors who had the foresight to take the risk of investing in Bill Gates’s idea made fabulous amounts of money. A twenty-thousand-dollar investment in Microsoft in 1986 was worth about two million dollars in 2004.

Between 1900 and 2000, real wages in the United States quintupled from around fifteen cents an hour (worth three dollars in 2000 dollars) to more than fifteen dollars an hour. In other words, a worker in 2000 earned as much, adjusted for inflation, in twelve minutes as a worker in 1900 earned in an hour. That surge in the living standard of the American worker is explained, in part, by the increase in capital over that period. The main reason U.S. farmers and manufacturing workers are more productive, and their real wages higher, than those of most other industrial nations is that America has one of the highest ratios of capital to worker in the world. Even Americans working in the service sector are highly paid relative to workers in other nations as a result of the capital they work with. In their textbook, Nobel laureate Paul Samuelson and William D. Nordhaus noted: “Because each worker has more capital to work with, his or her marginal product rises. Therefore, the competitive real wage rises as workers become worth more to capitalists and meet with spirited bidding up of their market wage rates.”2 The capital-to-labor ratio explains roughly 95 percent of the fluctuation in wages over the past forty years. When the ratio rises, wages rise; when the ratio stays constant, wages stagnate.

What Is the Capital Gains Tax?

A capital gain is the difference between the price received from selling an asset and the price paid for it. An asset can be a home, a farm, a ranch, a family business, or a work of art, for instance.3 In most years, slightly less than half of the capital gains that the U.S. government taxes are on the sale of corporate stock. For all the controversy surrounding the tax treatment of capital gains, that tax brings in surprisingly little revenue for the federal government. From 1990 to 1995, capital gains tax collections were between $25 billion and $40 billion a year, less than 3 percent of federal tax revenues. During the Internet boom, when stock gains were huge, capital gains tax collections peaked at $119 billion in 2000 before rapidly falling back below $50 billion (see Table 1 for a breakdown of the sources of federal revenue).

The capital gains tax is different from almost all other forms of federal taxation in that it is relatively easy to avoid. Because people pay the tax only when they sell an asset, they can legally avoid payment by holding on to their assets—a phenomenon known as the “lock-in effect.”

The tax treatment of capital gains has other unique features. One is that capital gains are not indexed for inflation: the seller pays tax not only on the real gain in purchasing power, but also on the illusory gain attributable to inflation. The inflation penalty is one reason that, historically, capital gains have been taxed at lower rates than ordinary income. In fact, Alan Blinder, a former member of the Federal Reserve Board, noted in 1980 that, up until that time, “most capital gains were not gains of real purchasing power at all, but simply represented the maintenance of principal in an inflationary world.”4

|

|

|

| Capital gains tax | 45 |

| Corporate income tax | 132 |

| Individual income tax | 794 |

| Social Security taxes | 713 |

| Total revenues | 1,782 |

|

|

|

| Source: Historical Tables: Budget of the United States Government, Fiscal Year 2005 (Washington, D.C: Government Printing Office, 2004), Table 2.1, p. 22. Capital Gains from CBO. |

|

| Note: Columns do not add because not all sources of federal revenue are shown. | |

Another strange feature of the tax is that individuals are permitted to deduct only a portion of the capital losses they incur, whereas they must pay taxes on all of the gains. When taxpayers undertake risky investments, the government taxes fully any gain they realize if the investment has a positive return. But the government allows only partial tax deduction (of up to three thousand dollars per year) if the venture results in a loss. That introduces a bias in the tax code against risk-taking.5

One other peculiar aspect of the capital gains tax has made many economists conclude that it is economically inefficient: it is a form of double taxation on capital formation. Economists Victor Canto and Harvey Hirschorn explained:

A government can choose to tax either the value of an asset or its yield, but it should not tax both. Capital gains are literally the appreciation in the value of an existing asset. Any appreciation reflects merely an increase in the after-tax rate of return on the asset. The taxes implicit in the asset’s after-tax earnings are already fully reflected in the asset’s price or change in price. Any additional tax is strictly double taxation.6

Take, for example, the capital gains tax paid on a pharmaceutical stock. The value of that stock equals the discounted present value of all of the company’s future proceeds. If the company is expected to earn $100,000 a year for the next twenty years, the sales price of the stock will reflect those returns. The “gain” the seller realizes from the sale of the stock will reflect those future returns, and thus the seller will pay capital gains tax on the future stream of income. But the company’s future $100,000 annual returns will also be taxed when they are earned. So the $100,000 in profits is taxed twice—when the owners sell their shares of stock and when the company actually earns the income. That is why many tax analysts argue that the most equitable rate of tax on capital gains is zero.7

The Impact of Recent Capital Gains Tax Changes

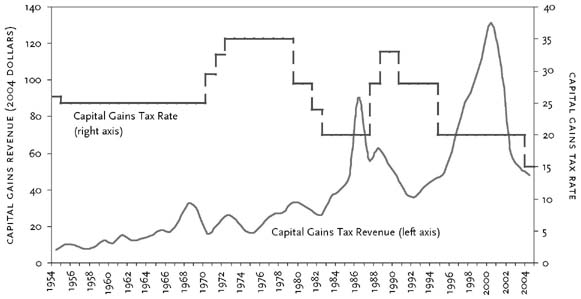

The historical evidence suggests that when the capital gains tax is reduced, locked-in capital is liberated and, at least temporarily, the revenues from the tax rise. For example, after the 1981 capital gains tax was cut from 28 to 20 percent, real (all figures in this section are 2004 dollars) federal capital gains tax revenues leapt from $29.4 billion in 1981 to $36.6 billion by 1983—a 24 percent increase. After the capital gains tax was cut in 1997, the receipts from capital gains taxes rose from $66.9 billion in 1996 to $114.7 billion by 1999, an increase of more than 71 percent. Preliminary data suggest that the capital gains tax cut of 2003 to a rate of 15 percent has also caused tax revenues to increase, at least in the first year (see Figure 1).

Conversely, total asset sales of taxable capital gains fell from $575 billion in 1986, the year before the capital gains rate was raised (from 20 back to 28 percent), to $246 billion in 1989. Investors were unwilling to sell stock and other taxable assets at the new higher tax rate.

Reducing the capital gains tax rate appears also to lead to higher stock prices. The stock market boomed in the 1980s after the 1981 capital gains tax cut; it boomed to new heights in the late 1990s after the Clinton capital gains rate cut, and then again in 2003 after George W. Bush signed his capital gains tax cut into law.

It may seem a paradox that a lower capital gains tax typically leads to more tax revenues collected from the tax. But, really, there is no mystery here. As mentioned, the capital gains tax is an easily avoided tax. When the tax rate is high, investors simply delay selling their assets—stocks, properties, businesses, and so on—to keep the tax collector away from their door. When the capital gains tax is cut, asset holders are more likely to sell. Moreover, because a lower capital gains tax substantially lowers the cost of capital, it encourages risk-taking and causes the economy to grow faster, thus raising all government receipts in the long term.

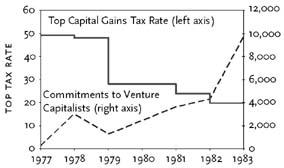

Capital Gains Tax Cuts and Business Creation

Past reductions in the capital gains tax rates (e.g., in 1978, 1981, and 1997) stimulated the financing and start-up of new businesses, while new business activity stalled after increases in capital gains taxes (1969 and 1986). Table 2 compares three measures of new business generation— the number of initial public stock offerings (IPOs), the dollars raised from those IPOs, and the dollars committed to venture capital firms—with fluctuations in the capital gains tax rate between 1969 and 2004.8 New commitments to venture capital firms (in 2004 dollars) increased from $220 million in 1977, when the top marginal tax rate on capital gains was 49 percent, to $9.7 billion by 1983, when the rate had been dropped to 20 percent and the U.S. economy had started pulling out of the recession (Figure 2). That was a 4,300 percent increase in capital raised for new firms.

Venture capital funds are the economic lifeblood of high-technology companies in industries that are critical to U.S. international competitiveness: computer software, biotechnology, computer engineering, electronics, aerospace, pharmaceuticals, and so forth. The high capital gains tax rate appears to have contributed to the drying up of funding sources for those promising new frontier firms following the 1986 tax hike.9 Significantly, the massive technology boom of the late 1990s came immediately after the 1997 capital gains tax cut, unleashing another period of venture activity (Figure 3).

| *. Estimated based on $11,249 through third quarter. | ||||

|

|

||||

| Year | Top Capital Gains Rate(%) | Initial Public Offerings | Dollars Raised (millions) | Commitments to Venture Capitalists (millions) |

|

|

||||

| 1969 | 27 | 780 | 2605 | 506 |

| 1970 | 32 | 358 | 780 | 272 |

| 1971 | 39 | 391 | 1665 | 252 |

| 1972 | 45 | 562 | 2724 | 157 |

| 1973 | 45 | 105 | 330 | 133 |

| 1974 | 45 | 9 | 51 | 124 |

| 1975 | 45 | 14 | 264 | 20 |

| 1976 | 49 | 34 | 237 | 93 |

| 1977 | 49 | 40 | 151 | 68 |

| 1978 | 48 | 42 | 247 | 980 |

| 1979 | 28 | 103 | 429 | 449 |

| 1980 | 28 | 259 | 1404 | 961 |

| 1981 | 24 | 438 | 3200 | 1628 |

| 1982 | 20 | 198 | 1334 | 2119 |

| 1983 | 20 | 848 | 13168 | 5098 |

| 1984 | 20 | 516 | 3934 | 4590 |

| 1985 | 20 | 507 | 10450 | 3502 |

| 1986 | 20 | 953 | 19260 | 4650 |

| 1987 | 28 | 630 | 16380 | 4900 |

| 1988 | 33 | 435 | 5750 | 2100 |

| 1989 | 33 | 371 | 6068 | 2200 |

| 1990 | 28 | 276 | 4519 | 2000 |

| 1991 | 28 | 367 | 16420 | 2511 |

| 1992 | 28 | 509 | 23990 | 5178 |

| 1993 | 28 | 605 | 37000 | 4963 |

| 1994 | 28 | 500 | 25000 | 5351 |

| 1995 | 28 | 500 | 28000 | 5608 |

| 1996 | 28 | 775 | 50000 | 11278 |

| 1997 | 20 | 575 | 40000 | 17207 |

| 1998 | 20 | 350 | 33000 | 22576 |

| 1999 | 20 | 492 | 63000 | 59164 |

| 2000 | 20 | 422 | 97000 | 106,028 |

| 2001 | 20 | 91 | 37134.1 | 38,064 |

| 2002 | 20 | 81 | 19232.4 | 3,661 |

| 2003 | 15 | 81 | 13571.9 | 10,528 |

| 2004 | 15 | 242 | 34240.5 | 15,000* |

|

|

||||

Who Gains from Cuts in the Capital Gains Tax?

Any discussion of the capital gains tax inevitably leads to a discussion of which income groups will benefit most from a change in the tax policy. For example, in the 1997 debate over the capital gains tax, opponents of a rate cut maintained that almost all of the benefits would go to high-income earners. That is true of the direct effects because high-income earners also earn most of the capital gains. It is also true, however, that cuts in capital gains tax rates benefit people at all levels, mainly because of the economic growth they engender. Moreover, the gains to non-high-income families should be noted. Internal Revenue Service data indicate that in 2003, the most recent year for which these data are available, 42 percent of all returns reporting capital gains were from households with incomes below $50,000. Seventy-two percent, or 6.4 million returns, were for households with incomes below $100,000.10 Despite this fact, overall gains are concentrated among high-income individuals, with 87 percent of overall gains going to filers with income above $100,000, and 74 percent to filers with income above $200,000. It is worth noting, however, that these numbers are misleading because they include the entire amount of the gain itself, which often represents the unlocking of value accumulated over many years. Finally, it should be noted that cuts in capital gains taxes particularly benefit the elderly. The elderly are two and a half times as likely to realize capital gains in a given year as are tax filers under the age of sixty-five. The elderly are also likely to derive a larger share of their income from capital gains than are younger workers. A study by the National Center for Policy Analysis examining IRS data from 1986 found that the average elderly tax filer had an income of $31,865, 23 percent of which was capital gains. The average nonelderly filer had an income of $26,199, 9 percent of which was from capital gains.11

Conclusion

On balance, the evidence supports the economic case for a low rate of tax on capital gains. Recent actual experience suggests that a low rate of tax on capital gains increases capital investment and new business formation. Tax revenues have surged when the capital gains rate has been cut as trillions of dollars of locked-in capital are released to be put to more productive uses.

Further Reading

Footnotes