Stock Market

By Jeremy J. Siegel

The price of a share of stock, like that of any other financial asset, equals the present value of the sum of the expected dividends or other cash payments to the shareholders, where future payments are discounted by the interest rate and risks involved. Most of the cash payments to stockholders arise from dividends, which are paid out of earnings and other distributions resulting from the sale or liquidation of assets.

The cash payments available to a shareholder are uncertain and subject to the earnings of the firm. This uncertainty contrasts sharply with cash payments to bondholders, the value of which is fixed by contractual obligation and is paid in a timely manner unless the firm encounters severe financial stress, such as bankruptcy. As a result, the price of stocks normally fluctuates more than the price of bonds.

Over time, most firms pay rising dividends. Dividends increase for two reasons. First, because firms rarely pay out all their earnings as dividends, the difference, called retained earnings, is available to the firm to invest or buy back its shares. This, in turn, often produces greater future earnings and, hence, higher prospective dividends. Second, a firm’s earnings will rise as the price of its output rises with inflation, as demand for its products grows, and as the firm operates more efficiently. Firms with steadily rising dividends are sought after by investors, who often pay premium prices to own such firms.

Cash payments to shareholders also result from the sale of some of the firm’s assets, outright liquidation, or a buyout. A firm may sell some of its operations, using the revenues from the sale to provide a lump-sum distribution to stockholders. When a firm sells all its operations and assets, this total liquidation results in a cash distribution after obligations to creditors are satisfied. Finally, if another firm or individual purchases the firm, existing shareholders are often eligible to receive cash distributions.

Stock Markets

In the United States, most stocks are traded either on the New York Stock Exchange (NYSE, or “Big Board”) or on NASDAQ, an electronic market that grew out of the “over-the-counter” market in 1970. The NYSE, founded in 1792, trades most of the large U.S. stocks through a series of specialists who are assigned stocks and facilitate trading on the floor of the exchange. In contrast, the NASDAQ has no specialists and no specific physical location since market makers and traders operate wholly through electronic systems.

In addition, there is a smaller exchange, also located in New York, called the American Stock Exchange (Amex), which trades in small stocks that are not large enough to qualify for trading on the NYSE. Many of the newly issued ETFs, or exchange-traded funds, that are designed to match the major stock market indexes are traded on the Amex.

Stock Indexes

The aggregate movement of individual stocks is measured by stock indexes. The world’s most famous stock index, and the one that has the longest continuous history, is the Dow Jones Industrial Average, which dates from 1897 and currently contains thirty large firms. The S&P (Standard and Poor’s) 500 Stock Index contains five hundred stocks and is a value-weighted price index that was founded in 1957. It is considered the benchmark index for large stocks traded and contains about 80 percent of the value of all U.S. stocks.

The Nasdaq index represents stocks traded on the NASDAQ market (see above). This index is also value-weighted and is heavily influenced by the large technology stocks (such as Microsoft and Intel) that trade on the NASDAQ market.

There are also indexes of smaller stocks and international stocks. The best known small-stock index is the Russell 2000, which contains the smallest two thousand of the top three thousand stocks traded. Standard and Poor’s also publishes mid-cap and small-stock indexes. Morgan Stanley has developed many indexes for international stock markets abroad, including the EAFE (Europe, Australasia, and Far East), which contains almost all non-U.S. stocks.

Returns on Stocks

The total return from owning stock arises from two sources: dividends and capital gains. A total return index for stocks can be computed by assuming that all dividends are reinvested by buying additional shares of the stock. A total return index would be akin to the accumulation of a pension plan that reinvested all dividends and capital gains back into the market, or to a mutual fund that reinvested all distributions back into the fund.

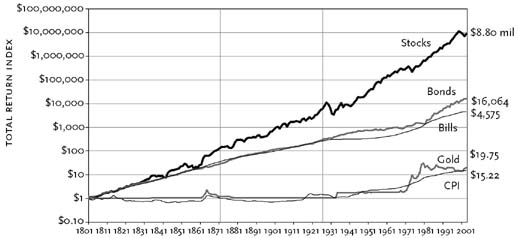

Over time, the total return on stocks has exceeded that of any other class of asset. This is shown in Figure 1, which compares the total returns to stocks, long- and short-term government bonds, gold, and commodities (measured by the Consumer Price Index, or CPI.). One dollar invested in stocks in 1802 would have grown to $8.8 million in 2003, in bonds to $16,064, in treasury bills to $4,575, and in gold to $19.75. The CPI has risen by a factor of 14.22, almost all of it after World War II.

The average compound after-inflation rate of return on stocks from 1802 through 2002 was 6.8 percent per year, and this number has remained remarkably steady over time. A 6.8 percent annual rate of return means that if all dividends are reinvested, the purchasing power of stocks has doubled, on average, every ten years over the past two centuries. This return far exceeds that of other financial assets. This evidence shows that, over long periods of time, the price of stocks fully compensates stockholders for any inflation, as the real return on stocks since World War II is virtually identical to that prior to that war.

Factors Affecting Stock Prices

Two major factors affect stock prices: earnings, which determine the dividends on the stocks; and interest rates, which “discount” future cash payments to the present.

As interest rates rise, all other things being equal, stock prices will fall. However, interest rates often rise in an environment of increasing economic activity and, hence, higher expected earnings. Therefore, stock prices may not fall and may actually rise when interest rates rise. Notwithstanding, low-interest-rate environments are usually deemed good for the stock market, and stocks usually respond favorably when the Federal Reserve lowers rates and unfavorably when it raises rates.

Stock prices are quite variable in the short run. The annual standard deviation of after-inflation returns has averaged about 18 percent, which means that about two-thirds of the time, stock returns will be in a range from −12 percent to +24 percent over a twelve-month period. However, the worst average annual real return for stocks over any twenty-year period has been 1.0 percent, and the worst return over all thirty-year periods is 2.6 percent per year after inflation.

Over twelve-month periods, stocks outperform bonds only about 60 percent of the time. But as the holding period becomes greater, the frequency of stock outperformance becomes very large. Over twenty-year periods, stocks outperform bonds about 95 percent of the time. We recently passed through a rare twenty-year period in which bonds outperformed stocks as recently as 2002. But since 1872, stocks have always outperformed bonds over thirty-year periods.

The stock market almost always falls before recessions. In fact, thirty-nine of the forty-two recessions the United States has experienced from 1802 through 1990 were preceded or accompanied by declines of at least 10 percent in the stock index. In the postwar period, the peak of the stock market preceded the peak of the business cycle by between six months and eight months, but this is quite variable. In 1990, stocks and the economy peaked in the same month, but in the 2001 recession, stocks peaked about one year earlier.

Stock prices can move dramatically even within a day. Over the past 120 years, there have been about 120 days when the Dow Jones Industrial Average changed by at least 5 percent. In only about one-quarter of these periods has there been an identifiable cause of such a change. On other occasions, stock movements were caused by accumulated optimism or pessimism of investors.

The largest one-day drop in stock-market history occurred on Monday, October 19, 1987, when the Dow Jones Industrial Average fell 508 points, or 22.6 percent. No significant news event explains the decline, although rising interest rates and a falling dollar began to weigh on a market that had become temporarily overvalued after a five-year bull run.

Because a recession did not follow this huge decline and stock prices subsequently recovered to new highs, many pointed to “Black Monday,” as that day was called, as a confirmation of the “irrationality” of the stock market.

Stock prices, however, are determined by expectations of the future, which must, by definition, be unknown. Shifts in sentiment and psychology can sometimes cause substantial changes in the valuation of the market. Despite occasional false alarms, the stock market is still considered an important indicator of future business conditions.

Further Reading