Savings and Loan Crisis

By Bert Ely

Years later, the extraordinary cost of the 1980s S&L crisis still astounds many taxpayers, depositors, and policymakers. The cost of bailing out the Federal Savings and Loan Insurance Corporation (FSLIC), which insured the deposits in failed S&Ls, may eventually exceed $160 billion. At the end of 2004, the direct cost of the S&L crisis to taxpayers was $124 billion, according to financial statements published by the Federal Deposit Insurance Corporation (FDIC), the successor to the FSLIC. Additionally, healthy S&Ls as well as commercial banks have been taxed approximately another $30 billion to pay for S&L cleanup costs. Finally, the federal courts are still resolving the so-called goodwill cases stemming from regulatorily inspired mergers of failing S&Ls into healthy S&Ls in the early 1980s (discussed below). Resolving these cases will probably cost taxpayers another $5–$10 billion.

The bankruptcy of the FSLIC did not occur overnight; the FSLIC was a disaster waiting to happen for many years. Numerous public policies, some dating back to the 1930s, created the disaster. Some policies were well intended but misguided. Others had lost whatever historical justification they might once have had. Yet others were desperate attempts to postpone addressing a rapidly worsening situation. All of these policies, however, greatly compounded the S&L problem and made its eventual resolution more difficult and much more expensive. When disaster finally hit the S&L industry in 1980, the federal government managed it very badly.

Fifteen public policies that contributed to the S&L debacle are summarized below.

Public Policy Causes with Roots Before 1980

Federal deposit insurance, which was extended to S&Ls in 1934, was the root cause of the S&L crisis. Deposit insurance was actuarially unsound from its inception, primarily because all S&Ls were charged the same Insurance premium rate regardless of how safe or risky they were. That is, deposit insurance provided by the federal government tolerated the unsound financial structure of S&Ls for decades. No sound insurance program would have done that. Congress tried to rectify this problem in 1991 when it directed the FDIC to begin charging risk-sensitive deposit-insurance premiums. However, because those who should pay the most would scream the loudest to Congress, the FDIC’s premium structure still does not charge the riskiest banks and S&Ls enough. Much of the time, the “drunk drivers” of the S&L and banking world pay no more for their deposit insurance than do their sober siblings. Those who do pay more still do not pay enough.

Borrowing short to lend long was the financial structure that federal policy effectively forced S&Ls to follow in the aftermath of the Great Depression. S&Ls used short-term passbook savings to fund long-term, fixed-rate home mortgages. Although the long-term, fixed-rate mortgage may have been an admirable public-policy objective, the federal government picked the wrong horse—the S&L industry—to do this type of lending because S&Ls funded themselves primarily with short-term deposits. The dangers inherent in this “maturity mismatching” became evident every time short-term interest rates rose. S&Ls, stuck with long-term loans at fixed rates, often had to pay more to their depositors than they were making on their mortgages. In 1981 and 1982 the interest rate spreads for S&Ls (the difference between the average interest rate on their mortgage portfolios and their average cost of funds) were −1.0 percent and −0.7 percent, respectively.

Regulation Q, under which the Federal Reserve since 1933 had limited the interest rates banks could pay on their deposits, was extended to S&Ls in 1966. Regulation Q was price fixing, and like most efforts to fix prices (see price controls), Regulation Q caused distortions far more costly than any benefits it may have delivered. Regulation Q created a cross subsidy, passed from saver to home buyer, that allowed S&Ls to hold down their interest costs and thereby continue to earn, for a few more years, an apparently adequate interest margin on the fixed-rate mortgages they had made ten or twenty years earlier. Thus, the extension of Regulation Q to S&Ls was a watershed event in the S&L crisis: it perpetuated S&L maturity mismatching for another fifteen years, until it was phased out after disaster struck the industry in 1980. A remnant of Regulation Q remains—banks are still barred from paying interest on business checking accounts.

Interest rate restrictions locked S&Ls into below-market rates on many mortgages whenever interest rates rose. State-imposed usury laws limited the rate lenders could charge on home mortgages until Congress banned states from imposing this ceiling in 1980. In addition to interest rate ceilings on mortgages, the due-on-sale clause in mortgage contracts was not uniformly enforceable until 1982. Before, borrowers could transfer their lower-interest-rate mortgages to new homeowners when property was sold.

A federal ban on adjustable-rate mortgages until 1981 further magnified the problem of S&L maturity mismatching by not allowing S&Ls to issue mortgages on which interest rates could be adjusted during times of rising interest rates. As mentioned above, during periods of high interest rates, S&Ls, limited to making long-term, fixed-rate mortgages, earned less interest on their loans than they paid on their deposits.

Restrictions on setting up branches and a restriction on nationwide banking prevented S&Ls, and banks as well, from expanding across state lines. S&Ls, unable to diversify their credit risks geographically, became badly exposed to regional economic downturns that reduced the value of their real estate collateral. In the 1980s, S&Ls began branching across state lines; in 1994, Congress authorized interstate branching for banks.

The dual chartering system permitted state-regulated S&Ls to be protected by federal deposit insurance. Therefore, state chartering and supervision could impose losses on the federal taxpayer if the state regulations became too permissive or if state regulators were too lax.

The secondary mortgage market agencies created by the federal government—Fannie Mae and Freddie Mac—undercut S&L profits by using their taxpayer backing to effectively lower interest rates on all mortgages. This helped home buyers, but the resulting lower rates made S&L maturity mismatching even more dangerous, especially as interest rates became more volatile after 1966.

Public Policy Causes That Began in the 1980s

Disaster struck after Paul Volcker, then chairman of the Federal Reserve Board, decided in October 1979 to restrict the growth of the money supply, which in turn caused interest rates to skyrocket. Between June 1979 and March 1980 short-term interest rates rose by more than six percentage points, from 9.06 percent to 15.2 percent. In 1981 and 1982 combined, the S&L industry collectively reported almost $9 billion in losses. Worse, in mid-1982 all S&Ls combined had a negative net worth, valuing their mortgages on a market-value basis, of $100 billion, an amount equal to 15 percent of the industry’s liabilities. Specific policy failures during the 1980s are examined below.

An incomplete and bungled deregulation of S&Ls in 1980 and 1982 lifted restrictions on the kinds of investments S&Ls could make. In 1980 and again in 1982, Congress and the regulators granted S&Ls the power to invest directly in service corporations, permitted them to make real estate loans without regard to the geographical location of the loan, and authorized them to hold up to 40 percent of their assets as commercial real estate loans. Congress and the Reagan administration naïvely hoped that if S&Ls made higher-yielding, but riskier, investments, they would make more money to offset the long-term damage caused by fixed-rate mortgages. However, the 1980 and 1982 legislation did not change how premiums were set for federal deposit insurance. Riskier S&Ls still were not charged higher rates for deposit insurance than their prudent siblings. As a result, deregulation encouraged increased risk taking by S&Ls.

Capital standards were debased in the early 1980s in an extremely unwise attempt to hide the economic insolvency of many S&Ls. The Federal Home Loan Bank Board (FHLBB), the now-defunct regulator of S&Ls, authorized accounting gimmicks that violated generally accepted accounting principles. In one of the most flagrant gimmicks, firms that acquired S&Ls were allowed to count as goodwill the difference between the market value of assets acquired and the value of liabilities assumed. If a firm acquired an S&L with assets whose market value was five billion dollars and whose liabilities were six billion, for example, the one-billion-dollar difference was counted as goodwill, and the goodwill was then counted as capital. This “push-down” accounting—losses were pushed down the balance sheet into the category of goodwill—and other accounting gimmicks permitted S&Ls to operate with less and less real capital. Thus just as S&Ls, encouraged by deregulation, took on more risk, they had a smaller capital cushion to fall back on and, therefore, less to lose by making bad decisions.

Inept supervision and the permissive attitude of the FHLBB during the 1980s allowed badly managed and insolvent S&Ls to continue operating. In particular, the FHLBB eliminated maximum limits on loan-to-value ratios for S&Ls in 1983. Thus, where an S&L had been limited to lending no more than 75 percent of the appraised value of a home, after 1983 it could lend as much as 100 percent of the appraised value. The FHLBB also permitted excessive lending to any one borrower. These powers encouraged unscrupulous real estate developers and others who were unfamiliar with the banking business to acquire and then rapidly grow their S&Ls into insolvency. When the borrower and the lender are the same person, a conflict of interest develops. Also, because developers, by nature, are optimists, they lack the necessary counterbalancing conservatism of bankers.

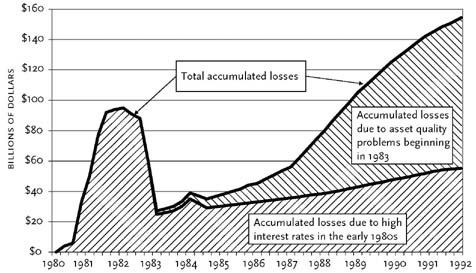

Delayed closure of insolvent S&Ls greatly compounded the FSLIC’s losses by postponing the burial of already dead S&Ls. Figure 1 shows how losses in insolvent S&Ls grew during the 1980s as the closure of insolvent S&Ls was delayed. Mid-1983 would have been the optimum time to close hopelessly insolvent S&Ls. Instead, Congress chose to put off the eventual day of reckoning, which only compounded the problem. Over half of these losses reflect the pure cost of delayed closures—compound interest on already incurred losses. The rest of the cost, except for the part that went to owners of S&Ls, represents the waste of real resources—building unneeded shopping centers and office buildings and keeping open S&L branches that should have been closed. However, there would have been little, if any, of this real waste if all of the then-insolvent S&Ls had been closed by mid-1983; they would not have been around to make all the bad loans they made after 1983 or to incur wasteful operating expenses.

Lack of truthfulness in quantifying the FSLIC’s problems hid from the general public the size of the FSLIC’s losses. Neither the FHLBB nor the General Accounting Office (GAO), now called the Government Accountability Office, provided realistic cost estimates of the problem as it was growing. On May 19, 1988, for example, Frederick Wolf of the GAO testified that the FSLIC bailout would cost thirty to thirty-five billion dollars. Over the next eight months, the GAO increased its estimate by forty-six billion dollars.

Congressional and administration delay and inaction, due to an unwillingness to confront the true size of the S&L mess and anger politically influential S&Ls, prevented appropriate action from being taken once the S&L problem was identified. The 1987 FSLIC recapitalization bill provided just $10.8 billion for the cleanup, even though it was clear at the time that much more—possibly as much as $40 billion—was needed. The first serious attempt at cleaning up the FSLIC mess did not come until Congress enacted the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA). Even FIRREA, however, did not provide sufficient funds to completely clean up the S&L mess. Eventually, in fits and starts, Congress did appropriate sufficient funds to finish the job.

Flip-flops on real estate taxation first stimulated an overbuilding of commercial real estate in the early 1980s and then accentuated the real estate bust when depreciation and “passive loss” rules were tightened in 1986. The flip-flop had a double whammy effect: the 1981 tax law caused too much real estate to be built, and the 1986 act then hurt the value of much of what had been built.

What Did Not Cause the S&L Disaster

Some highly publicized factors in the S&L debacle—criminality, a higher deposit-insurance limit, brokered deposits, and faulty audits of S&Ls—did not cause the mess. Instead, these factors are symptoms or consequences of it.

Crooks certainly stole money from many insolvent S&Ls. However, criminality costs the taxpayer money only when it occurs in an already insolvent S&L that the regulators had failed to close when it became insolvent. Delayed closure is the cause of the problem, and criminality is a consequence. In any event, criminality accounted for only five billion dollars, or 3 percent, of the cost of the FSLIC bailout.

Raising the deposit-insurance limit in 1980 from $40,000 to $100,000 did not cause S&Ls to go haywire, but it did make it slightly easier to funnel money into insolvent S&Ls. Put another way, had the deposit-insurance limit been kept at $40,000, a depositor intent on putting $200,000 of insured funds into insolvent S&Ls paying high interest rates would have had to deposit his money, in $40,000 chunks, into five different S&Ls. Because of the higher limit, two $100,000 deposits would keep the $200,000 fully insured.

Brokered deposits became an important source of deposits for many S&Ls in the 1980s. Brokered deposits allowed brokerage houses and deposit brokers to divide billions of dollars in customers’ funds into $100,000 pieces, search the country for the highest rates being paid by S&Ls, and deposit those pieces into different S&Ls. Brokered deposits, though, were the regulators’ best friend because this “hot money,” always chasing high interest rates, kept insolvent S&Ls liquid, enabling regulators to delay closing these S&Ls. Regulators, therefore, were the true abusers of brokered deposits. Only in this regard did brokered deposits contribute to the S&L crisis. In the years since then, brokered deposits have become an acceptable funding source for banks and S&Ls since only sound institutions can now accept brokered deposits.

Certified public accountants (CPAs) have been blamed for not detecting failing S&Ls and reporting them to the regulators. However, CPAs were hired by S&Ls to audit their financial statements, not to backstop the regulators. Federal and state S&L examiners, working for the taxpayer, were supposed to be fully capable of detecting problems, and often did. Interestingly, CPA audit reports often disclosed financial problems in S&Ls, including regulatory accounting practices that were at odds with generally accepted accounting principles. The regulators, however, usually failed to act on those findings. The CPAs were scapegoats for known problems the regulators should have quickly acted on.

Junk-bond investments by S&Ls were often cited in the press and by politicians as a major contributor to the industry’s problems. In fact, junk bonds played a trivial role. (junk bonds are securities issued by companies whose credit rating is below “investment grade.”) A GAO report issued just five months before the passage of FIRREA cited a study by a reputable research group that showed junk bonds to be the second most profitable asset (after credit cards) that S&Ls held in the 1980s. The report also pointed out that only 5 percent of S&Ls owned any junk bonds at all. Total junk-bond holdings of all S&Ls amounted to only 1.2 percent of their total financial assets. Even so, Congress mandated in FIRREA that all S&Ls sell their junk-bond investments—which they did, often at a significant loss.

The Future of S&Ls

In 1989, Congress started knocking down the barriers separating commercial banks from S&Ls. Since then, much of the S&L industry has been absorbed into the broader banking industry, through outright mergers as well as bank holding company acquisitions of S&Ls. Statutory and regulatory changes have largely, but not completely, eliminated differences between bank and S&L charters. For all practical purposes, both types of institutions operate today under the same regulatory regime. Yet at the end of 2004, 886 S&Ls remained, with total assets of $1.35 trillion. While many of the largest S&Ls are now owned by bank holding companies, two independent S&Ls—Washington Mutual Bank and World Savings Bank—each had more than $100 billion of assets while numerous other independent S&Ls had assets exceeding $1 billion. The number of S&Ls most likely will continue to decline, but it may be many years before they disappear completely. Whether or not S&Ls do disappear is no longer a public-policy concern because they now are so similar to banks.

About the Author

Bert Ely is head of Ely and Company, a financial institutions and monetary policy consulting firm in Alexandria, Virginia. He was one of the first people to publicly predict FSLIC’s bankruptcy.

Further Reading