International Capital Flows

By Mack Ott

International capital flows are the financial side of international trade.1 When someone imports a good or service, the buyer (the importer) gives the seller (the exporter) a monetary payment, just as in domestic transactions. If total exports were equal to total imports, these monetary transactions would balance at net zero: people in the country would receive as much in financial flows as they paid out in financial flows. But generally the trade balance is not zero. The most general description of a country’s balance of trade, covering its trade in goods and services, income receipts, and transfers, is called its current account balance. If the country has a surplus or deficit on its current account, there is an offsetting net financial flow consisting of currency, securities, or other real property ownership claims. This net financial flow is called its capital account balance.

When a country’s imports exceed its exports, it has a current account deficit. Its foreign trading partners who hold net monetary claims can continue to hold their claims as monetary deposits or currency, or they can use the money to buy other financial assets, real property, or equities (stocks) in the trade-deficit country. Net capital flows comprise the sum of these monetary, financial, real property, and equity claims. Capital flows move in the opposite direction to the goods and services trade claims that give rise to them. Thus, a country with a current account deficit necessarily has a capital account surplus. In balance-of-payments accounting terms, the current-account balance, which is the total balance of internationally traded goods and services, is just offset by the capital-account balance, which is the total balance of claims that domestic investors and foreign investors have acquired in newly invested financial, real property, and equity assets in each others’ countries. While all the above statements are true by definition of the accounting terms, the data on international trade and financial flows are generally riddled with errors, generally because of undercounting. Therefore, the international capital and trade data contain a balancing error term called “net errors and omissions.”

Because the capital account is the mirror image of the current account, one might expect total recorded world trade—exports plus imports summed over all countries—to equal financial flows—payments plus receipts. But in fact, during 1996–2001, the former was $17.3 trillion, more than three times the latter, at $5.0 trillion.2 There are three explanations for this. First, many financial transactions between international financial institutions are cleared by netting daily offsetting transactions. For example, if on a particular day, U.S. banks have claims on French banks for $10 million and French banks have claims on U.S. banks for $12 million, the transactions will be cleared through their central banks with a recorded net flow of only $2 million from the United States to France even though $22 million of exports was financed. Second, since the 1970s, there have been sustained and unexplained balance-of-payments discrepancies in both trade and financial flows; part of these balance-of-payments anomalies is almost certainly due to unrecorded capital flows. Third, a huge share of export and import trade is intrafirm transactions; that is, flows of goods, material, or semifinished parts (especially automobiles and other nonelectronic machinery) between parent companies and their subsidiaries. Compensation for such trade is accomplished with accounting debits and credits within the firms’ books and does not require actual financial flows. Although data on such intrafirm transactions are not generally available for all industrial countries, intrafirm trade for the United States in recent years accounts for 30–40 percent of exports and 35–45 percent of imports.3

The bulk of capital flows are transactions between the richest nations. In 2003, of the more than $6.4 trillion in gross financial transactions, about $5.4 trillion (84 percent) involved the 24 industrial countries and almost $1.0 trillion (15 percent) involved the 162 less-developed countries (LDCs) or economic territories, with the rest, less than 1 percent, accounted for by international organizations.4 The shares of both industrial nations and the international organizations have been receding from their highs in 1998: 90 percent for industrial nations and 5 percent for the international organizations. In that year the combination of the Russian debt default and ruble devaluation, the south Asia financial crisis, and the lingering uncertainty about financial consequences of the return of Hong Kong to Chinese sovereignty in July 1997 drove the LDC share down to 5 percent of world capital flows.5 In the more tranquil five years following these crises, 1999–2003, LDC financial transactions involving mainland China and Hong Kong averaged 28 percent of the LDC total, and adding Taiwan, Singapore, and Korea brings the share to 53 percent of the developing-country transactions. Of the remaining forty-seven percentage points of developing-country transactions, Europe (primarily Russia, Turkey, Poland, and the Czech Republic) and the Western Hemisphere (primarily Mexico, Brazil, and Chile) each accounted for about sixteen percentage points, with the Middle East and Africa combining for the remaining sixteen percentage points.

Financing Trade in Goods, Services, and Assets

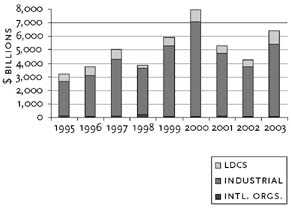

Figure 1 shows that most financial flows involve industrial countries whose gross flows (credits plus debits) during 1995–2003 averaged $4.9 trillion per year. Capital flows involving industrial countries comprised about 90 percent of total transactions, with LDCs and international organizations accounting for the remainder. Perhaps more significant, these gross flows were about ten times the net capital flows, reflecting the netting out of the vast majority of financial flows.

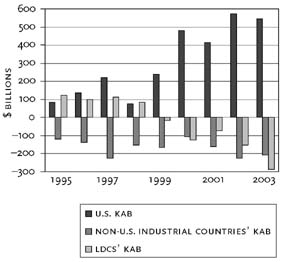

While much international trade is financed by offsetting trade flows, ultimately net trade balances must be financed by net financial flows. As Figure 2 shows, the United States has had large current-account deficits, primarily due to its deficit on merchandise trade; the non-U.S. industrial countries have had large trade surpluses; and LDCs, in aggregate, shifted from trade deficits to growing trade surpluses at the end of the twentieth century.

Net capital and financial flows finance these net trade imbalances, which, while primarily between industrial counties in gross terms, increasingly flowed, on net, from both developing and non-U.S. industrial countries to the United States. Reflecting their shift from trade deficits to trade surpluses at the end of the twentieth century, LDCs became net suppliers of capital in 1999 (Figure 3).

Figures 2 and 3 contain two glaring anomalies. First, Figure 2 shows that the U.S. current account deficit is far larger than the sum of the current account surpluses of the other industrial countries and the LDCs. This implies that the world has been running a current account deficit with itself, something that is logically impossible because the sum of all transactions across all countries—with exports positive and imports negative—must be zero. That is, an export from China to France is an import by France from China. Because the world is a closed system (no country trades with Mars), if trade data were accurate, the sum of world trade in goods and services (including income and transfers) would be zero. Yet, according to the recorded data, the world ran a current account deficit averaging more than $95 billion annually during 1995–2003. Combined with estimated errors and omissions, these missing data constitute omitted exports and financial flows well in excess of $100 billion per year.6 Second, Figure 3 shows that the sum of capital outflows from the non-U.S. industrial countries and LDCs is far smaller than the reported inflow of capital to the United States. Thus, the world ran a substantial capital surplus—again, a logical impossibility (no borrowing from Mars). Although there is no agreed-upon explanation for these discrepancies, there are two possible reasons, depending on whether or not U.S. data on earnings from foreign direct investment are accurate.

First, if the U.S. data are correct, then, because the sum of the U.S. current account deficit in Figure 2 and its capital account surplus in Figure 3 is close to zero, there must be underreported exports to the United States from the non-U.S. industrial countries and the LDCs, balanced by unreported financial flows from them to the United States.

Alternatively, suppose that the U.S. data on foreign direct investment earnings are not accurate, in particular that U.S. net income from its direct investments has been underreported.7 Reporting these earnings at their higher actual level would result in a reduction of the U.S. current account deficit (due to the increased income from “renting” capital to foreigners) and an equal reduction of the U.S. capital-account surplus.8

The available evidence makes the second explanation more likely than the first.

Composition of Capital and Financial Flows

Trade imbalances are financed by offsetting capital and financial flows, which generate changes in net foreign assets. These payments can be any combination of the following:

•

capital investments

•

portfolio investments in either debt or equity securities

•

direct investment in domestic firms (FDI) including start-ups

•

changes in international reserves9

As Table 1 shows, industrial countries financed their current account balances primarily with financial flows other than direct investment or reserve flows. Indeed, while the industrial countries were importing capital in the form of other financial flows, they were at the same time exporting capital as investors in the form of foreign direct investment (outflow of capital indicated by minus sign). The flow of net direct investment from industrial countries averaged −$115 billion during the nine years shown in Table 1 and was directed primarily to developing countries. These capital outflows were an important component of financing investment in the LDCs, where the foreign direct investment inflows averaged $154 billion, positive numbers indicating an inflow.

The difference between the industrial country outflow and the developing country inflow was primarily due to foreign direct investment in the United States, which averaged −$36 billion; that is, investors in LDCs were making substantial investments in the United States, much of it reflecting capital flight from insecure financial markets in LDCs to the greater security of property rights in industrial countries. Because financial claims may be short term or long term, real or financial, the key to development is to raise long-term investments as a percentage of capital inflows into LDCs.10 Foreign direct investment—distinguished from portfolio investment by the investor’s substantial ownership share (>10 percent)—implies a greater commitment to a long-term interest in the investment project and an active interest in managing the project. While the United States has been, along with developing countries, the major recipient of direct investment inflows, it is also a major supplier of foreign direct investment.

As Table 1 shows, flows of net investment from industrial countries to LDCs were substantial and were a major impulse to their growth; however, much of industrial and developing country investment was funneled to the United States. Of these capital flows from LDCs to the United States, a substantial share has been purchases of U.S. government debt taken up by LDCs as reserve assets; LDCs’ central banks buy and hold a great amount of U.S. debt as international reserves to back their domestic currencies. Purchases of such reserve assets, primarily short-term U.S. Treasury bills, amounted to more than $1 trillion during 1997–2003, with $340 billion in 2003 alone.

The non-U.S. industrial countries—particularly France, Japan, the Netherlands, Switzerland, and the United Kingdom—have been the primary net investors; these five countries supplied the largest part of direct investment during the period 1995–2003, equivalent to 76 percent of the annual net direct investment of all LDCs over this period.11 The distribution of this net foreign direct investment (inflows) was not uniform across LDCs. Almost half of total net direct investment in developing countries was invested in three LDCs: China with 26 percent, Brazil with 13 percent, and Mexico with 8 percent. At the other end of the spectrum, the countries of sub-Saharan Africa accounted, in total, for only 5 percent of total direct investment in LDCs.

|

|

|||||||||

| 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | |

|

|

|||||||||

| Industrial Countries | |||||||||

| Current Account Balance Financing | 42 | 33 | 73 | −41 | −186 | −292 | −249 | −276 | −314 |

| Net foreign direct investment | −106 | −115 | −133 | −153 | −172 | 18 | −100 | −77 | −202 |

| Reserves | −78 | −77 | −23 | 7 | −40 | −45 | −27 | −66 | −166 |

| Other financial and capital flows | 162 | 205 | 168 | 73 | 282 | 413 | 394 | 496 | 714 |

| Net errors and omissions | −20 | −47 | −84 | 114 | 116 | −93 | −18 | −77 | −32 |

|

|

|||||||||

| LDCs | |||||||||

| Current Account Balance Financing | −104 | −88 | −81 | −51 | 52 | 136 | 94 | 148 | 245 |

| Net foreign direct investment | 103 | 120 | 155 | 165 | 191 | 169 | 179 | 136 | 141 |

| Reserves | −112 | −112 | −83 | −48 | −110 | −127 | −129 | −204 | −340 |

| Other financial and capital flows | 140 | 100 | 50 | −29 | −94 | −149 | −122 | −86 | −85 |

| Net errors and omissions | −28 | −20 | −41 | −37 | −38 | −30 | −22 | 5 | 39 |

|

|

|||||||||

| Notes: Capital flows indicate investments and borrowings of all terms, ranging from currency holdings and short-term lending to long-term bonds or equity investments. Capital inflows (borrowings and investments) are indicated by positive numbers while capital outflows (lending and investments) are indicated by negative numbers. | |||||||||

Contemporary Versus Historical Capital and Financial Flows

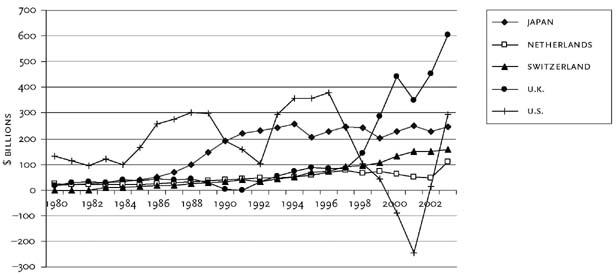

Over the past two hundred years, the world’s dominant international investors have been the Western European nations, particularly the United Kingdom, the Netherlands, and Switzerland. Capital from these countries was invested in their own and other European colonies and in other developing nations, first in the Western Hemisphere and, more recently, worldwide, particularly in China and Brazil. During the nineteenth century, the British financed the transcontinental railroads in the United States and Canada and built vast agricultural plantations in Africa and Asia. Today, Great Britain and the Netherlands remain, as they have from colonial times, among the largest direct investors in the United States: Britain is largest, followed by Japan, Germany, the Netherlands, and France. After World War I, the United States emerged as the world’s predominant direct investor and, in gross terms, remains so. As of 2003, U.S. foreign direct assets were more than twice those of the United Kingdom, the next largest asset holder at $2.7 trillion, while U.S. foreign direct investment liabilities were $2.4 trillion, implying a net FDI position of $300 billion. During the past two decades, the United Kingdom again became the world’s largest net foreign direct investor, with about $600 billion in net holdings at exchange rates prevailing in 2003. Following the United Kingdom in order are the United States, Japan, Switzerland, and the Netherlands. As Figure 4 shows, foreign direct investment flows have cumulated to huge international holdings by these five principal investors.12

About the Author

Mack Ott is an international economic consultant whose major assignments have been in the former Soviet Union countries, the Balkans, and Egypt. During 2003 and 2004 he was macroeconomic adviser to the chief economist of Nigeria and to the West African Monetary Institute. He has also been a U.S. Treasury adviser to the Ministry of Finance of Saudi Arabia.

Further Reading

Footnotes

Technically, the sum of capital account, financial account, and reserve flows finances the current account. The financial account—portfolio investment and direct investment—accounts for 90 percent of the financing while the capital account—payments for buildings and nonproduced fixed assets such as land—constitutes a minor part of the financing of the current account, typically less than 10 percent; a miniscule residual amount is accounted for by flows of currencies between central banks. It is traditional to refer to the financial side of the balance of payments as the capital account, and, except where it is necessary to maintain the distinction, “capital account” and “financial account” are used here interchangeably. Further analyses of capital flows, their accounting, and their relation to trade and international investment are contained in the NBER volume edited by Martin Feldstein (1999).

Note that these are financial transactions entailing a purchase/sale of a security or real asset, not currency exchanges. The Bank of International Settlements estimated the daily volume in currency transactions to be $1.2 trillion in 2001. Thus, the daily flow through currency markets is nearly one-third of the annual volume in financial flows. Unless otherwise noted, these and other data cited in this article are drawn from the International Monetary Fund’s Balance of Payments Statistics for May 2005. For nearly all international or regional data, the most recent observations are for 2002 or 2003.

William J. Zeile, “U.S. Affiliates of Foreign Companies: Operations in 2001,” Survey of Current Business 83 (August 2003): 50.

These international organizations are primarily the International Monetary Fund, the World Bank, other regional development banks, and the United Nations. The use of “involved” rather than “between” is important as many transactions involving LDCs were between an LDC and an industrial country. Still, the overall magnitudes clearly imply that the overwhelming majority of financial transactions involve industrial countries rather than LDCs.

In 1998, capital flows of Hong Kong amounted to more than 7 percent of the world total as inflows to Hong Kong financial assets and outflows from its liabilities each amounted to fifteen times their levels in succeeding years.

This is not a recent problem: the first IMF report on this issue, appearing in 1987 (Report on the World Current Account Discrepancy), observed that a substantial discrepancy had existed since the 1970s.

In 1984 former Federal Reserve Board governor H. Robert Heller testified to Congress that “there is some reason to believe that the bulk of unrecorded transactions is due to an underreporting of receipts of service items such as reinvested earnings abroad, investment income and fees. Consequently, the U.S. current account deficit, if measured properly, is likely to have been substantially smaller than indicated by the officially reported data” (Heller 1984, p. 67). Correspondingly, U.S. merchandise trade data have long been suspect in underreporting both merchandise exports and interest income (see Ott 1987).

There would be corresponding reductions in industrial country and LDC balances reducing their current account balance and increasing their capital account balance.

International reserve assets consist of foreign exchange holdings (currency and short-term assets) that are held by public (central bank and government) or private individuals and firms.

See Chuhan et al. 1996 for a discussion of the importance of long-term capital investment flows to LDC development.

Germany was a major supplier of direct investment funds in the first half of this period, but from 2000 forward it became, like the United States, a beneficiary of net direct investment inflows—during 2000–2003, net inflows of foreign direct investment to Germany totaled $171 billion.