Progressive Taxes

By Joel Slemrod

Judged by the top income tax rates alone, tax progressivity in the United States declined markedly in the eighties. In 1980 the highest tax rate stood at 70 percent. The Economic Recovery Tax Act of 1981 reduced that rate to 50 percent, and the Tax Reform Act of 1986 further reduced it to 33 percent. Although the highest rate has since been nudged back up to around 34 percent, it is still less than half what it was in 1980. Other developed countries have emulated the United States in reducing their top rates, although usually by less.

Does the precipitous fall in the top tax rate represent a sea change in how the tax burden is distributed? No. The statutory tax rates misrepresent true progressivity for three reasons.

First, the tax base—the income that is taxed—is generally much less than total income due to a bewildering array of adjustments, deductions, omissions, and mismeasurements. Since the erosion of the tax base was more pronounced for upper-income taxpayers prior to the 1986 tax act, the tax system was much less progressive than the old tax rates implied, and possibly not progressive at all. Although the 1986 act lowered the top rate from 50 percent to 33 percent, it also eliminated the ability to exclude from taxable income 60 percent of long-term capital gains. Because capital gains comprise a large fraction of the taxable income of the most affluent taxpayers, the expansion of their tax base offset, on average, the decline in the tax rate applied to the base.

Second, the tax burden—the hurt caused by taxes—is not borne entirely by the people who write the checks to the Internal Revenue Service. To some extent many taxes are “shifted” to other members of society. For example, because highly progressive taxes discourage people from entering high-paying professions, salaries in these professions will be higher than otherwise. Therefore, the taxes paid by the upper-income taxpayers who do enter these professions overstate the true burden of taxation on them. Also burdened by these high taxes are the people who pay higher prices for the goods and services provided by the people with higher salaries.

To take another example, taxes paid by high-income people who take advantage of the federal tax exemption for interest on state and local government bonds understate their true burden. The reason is that the yield on these securities is already lower to reflect their tax-preferred status—7.25 percent for tax-exempts (according to the Bond Buyer municipal index) in mid-1991 compared to 9.10 percent for taxable bonds (according to the Merrill Lynch corporate bond index). The main beneficiaries of this tax exemption are not those who hold the securities, but the state and local governments that get to pay lower interest rates on the funds they borrow. Because interest from state and local government bonds was tax exempt before 1986 and still is, the tax burden for the well-to-do who hold these bonds was, and is, understated.

Third, the progressivity of the tax structure cannot be judged by looking at only one component of taxes. Federal income taxes are only about 25 percent of total revenues collected by all levels of government. In recent years the fastest-growing component of federal taxes has been the payroll tax, which is regressive (the opposite of progressive) in its impact, because it taxes at a flat rate only on wages below $63,400 (in 1991). The Social Security system, however, is progressive because it pays higher benefits—relative to taxes paid in—to lower-income workers.

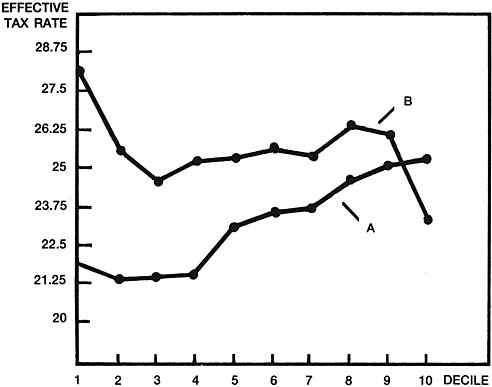

Chart 1 illustrates the progressivity of the overall U.S. tax system in 1985 (the latest year for which this information is available), according to two different assumptions about the shifting of taxes. Under assumption A the average tax rate generally increased with income, suggesting a generally progressive tax. Under assumption B the average tax rate actually is lowest for families in the highest income decile. The key difference between the two results is that B assumes that half of the corporation income tax is shifted to consumers, in the form of higher prices, while A assumes that all of it is borne by shareholders, who are generally high-income taxpayers. Chart 1 illustrates both the importance of the shifting assumptions and the fact that, even though the federal income tax by itself is progressive, its progressivity is overwhelmed by less progressive levies such as sales taxes and, to a lesser extent, the payroll tax.

Chart 1. Effective Tax Rate by Income Decile, 1985

SOURCE: Graph from Stiglitz, p. 348, based on Pechman, 1985.

Enlarge in new window

Traditionally, economists have taken three different approaches to this question. Under the benefit principle, taxes are thought of as a payment for services rendered by the government to individuals. Under this principle, revenue ought to be raised where possible by user fees. While this is a sensible policy for admission to national parks, it is not a feasible approach to financing other government activities such as national defense. It begs the question of how to measure the benefits any given taxpayer gains from such publicly provided goods as defense or the criminal justice system. Although the more affluent benefit more from the protection of that affluence, the precise relationship between their benefit and their income or wealth is undeterminable. Interestingly, reliance on the benefit principle would prohibit the government from transferring wealth from one group to another. It therefore undermines the case for the welfare system and the vast number of other government programs whose explicit objective is to redistribute resources.

Under the ability-to-pay principle, tax burdens should be related not to what taxpayers receive from government, but rather to their ability to bear the tax burden—that is, to tolerate a sacrifice. Reasoning from the plausible, but unprovable, idea that paying a dollar is a lesser sacrifice for a well-to-do person than for a poor person, an equal sacrifice requires higher tax payments from the well-to-do person. But as with the benefit principle, this reasoning does not point to a particular relationship between income and tax burden. A proportionate tax, whereby everyone pays the same percent of income, would take more from the rich person than from the poor person. Even a regressive tax, with everyone paying 25 percent on the first $20,000 of income, and 10 percent on all additional income, would take more from the rich than from the poor. Yet under other assumptions about sacrifice, a steeply progressive tax system is appropriate.

Under the utilitarian principle, tax burdens should be assigned to maximize social welfare. The nineteenth-century economist Francis Edgeworth showed that if from society’s perspective a dollar is valued less as the income of the recipient rises, then social welfare would be maximized by a tax system that leveled all incomes, taxing away all income above a certain level and distributing the proceeds to those whose incomes would otherwise fall below the cutoff income. The problem, of course, is that a leveling tax system would destroy the incentive to work, save, invest, and innovate, so that the size of the economic pie to be divided equally would rapidly shrink.

The modern theory of optimal income tax progressivity begins with the utilitarian principle, but views the issue as a trade-off between the social benefits of a more equal distribution of after-tax income and the economic damage imposed by highly progressive taxes. The social benefits of equality are not a matter that economists can resolve—they are better left to the theologians and philosophers to debate. But the economic costs of progressive tax rates are, in principle, knowable, and economists have invested much effort in knowing. As of 1980 many prominent economists (such as Michael Boskin, later President Bush’s chief economic adviser, and Harvard’s Martin Feldstein) were arguing that these costs were quite high, and concluded that the tax system at the time was probably too progressive.

After a decade featuring two major tax changes, many economists now doubt that tax policy has much effect on investment or saving. Alan Auerbach of the University of Pennsylvania has concluded that the 1986 tax changes played a relatively unimportant role in explaining the level and especially the pattern of investment in equipment and structures since then. Also, the personal saving rate declined steadily from 1980 to 1987, despite lowered tax rates on the return to saving and liberalized IRAs, and began to recover in 1987, soon after new restrictions were put on IRA eligibility.

But according to Brookings economists Barry Bosworth and Gary Burtless, the reductions in marginal tax rates did cause a modest increase in labor supply of a magnitude that had been predicted in 1980 by mainstream economists. Bosworth and Burtless found that men between the ages of 25 and 64 worked 5.2 percent more hours than would have been predicted on the basis of past trends, that women age 25 and 64 work 5.8 percent more, and that married women worked 8.8 percent more. They conclude that tax policy was probably not the dominant factor influencing labor supply over the decade. One reason for their cautious conclusion about the role of tax cuts is that lower-income men increased their labor supply by a large amount even though their marginal tax rates were constant or even rising until 1987.

Also, upper-income taxpayers responded to sharply lower tax rates by changing the timing of their asset sales and by abandoning financial stratagems such as tax shelters that were attractive only because of the special tax treatment they were given. So marginal tax rates do matter, but perhaps not as much or not in the same way as many economists thought in 1980.

Joel B. Slemrod is the Paul W. McCracken Collegiate Professor of Business Economics and Public Policy at the University of Michigan, and director of the Office of Tax Policy Research at the Michigan Business School. He was senior economist for tax policy in President Reagan’s Council of Economic Advisers.

Pechman, Joseph A. Who Paid the Taxes, 1966-1985? 1985.

Slemrod, Joel B., ed. Do Taxes Matter? The Impact of the Tax Reform Act of 1986. 1990.

Slemrod, Joel B., ed. “Do We Know How Progressive the Income Tax System Should Be?” National Tax Journal 36, no. 3 (September 1983): 361-69.

Stiglitz, Joseph E. Economics of the Public Sector, 2d ed. 1988.