I saw this in the Financial Times:

Many economists think the government can help a weak economy by convincing people the rate of price increases is poised to accelerate. In theory, households will spend more whilst businesses will boost their hiring and investment.

New research presented at the Brookings Panel on Economic Activity, which we attended, suggests this is mostly nonsense. A detailed survey of business executives in New Zealand suggests inflation expectations have basically no direct impact on the way companies make decisions. (Inflation expectations could affect how banks and capital markets charge firms for funding, but that’s an indirect effect.)

When asked what they would do if they learned prices would increase more over the next year than they were currently expecting, 65 per cent of managers wouldn’t raise prices, 75 per cent wouldn’t raise wages, 73 per cent wouldn’t increase employment, and 71 per cent wouldn’t increase investment.

Moreover, almost no manager would do any combination of those four things. Just 13 per cent of businesses would respond by raising both wages and prices — and that’s the most popular combination!

I’m not a fan of using inflation expectations to steer the economy, but this isn’t really a fair criticism. They haven’t even asked the right question. It makes no sense to ask the average businessman if they’d raise prices if they expected more inflation—of course the average businessman would raise prices—how else would you get the inflation! Here’s what they should have asked:

1. Suppose economic conditions evolve in such a way that you yourself will decide it’s appropriate to raise prices next year. In that case would you be more likely to boost employment and investment today?

But even that doesn’t really get at the question of interest to economists. A businessman might think to himself, “Hmmm, it sounds like there will be a big rent increase, or oil price increase, forcing me to raise prices next year. No, I don’t think I want to hire more workers or increase investment if there is a negative supply shock.”

The problem here is that the (New Keynesian) economists who talk about higher inflation expectations boosting the economy don’t really mean what they say. They talk about inflation, but in context it’s clear that what they really mean is “inflation caused by a positive AD shock.” That is, a rise in NGDP. So here’s an even better question to ask:

2. Suppose the economy goes into a boom next year, and aggregate demand is so strong that you feel it is appropriate to raise prices in response. In that case would you be more likely to boost employment and investment today?

And I think the answer would be yes. Not from everyone, but from enough to be of macroeconomic significance.

HT: Tyler Cowen

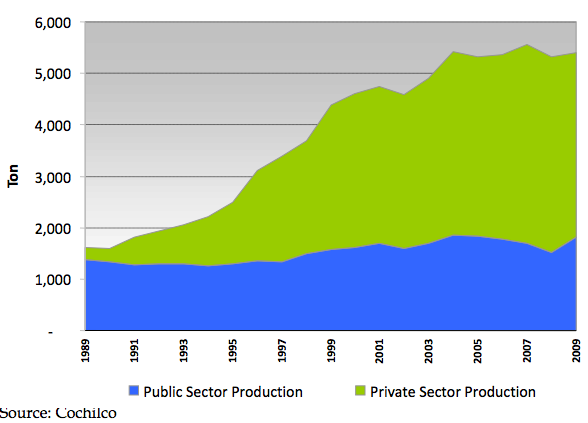

PS. Tyler responded to my recent post on Chilean copper:

I think it would be hard to privatize Chilean copper and then tax the mines at the proper rate, given the resulting power of the owners.

I think that’s a good argument, but not quite good enough to fully convince me. And that’s because there’s another good argument that cuts the other way, which is that privatized industries are far more productive. Consider this graph of public and private copper production:

If the industry were completely nationalized, I believe the tax revenue per ton of ore produced would be higher, as Tyler claims. But I also think it likely that total production would have been much lower without privatization. The net effect is unclear. And even if there’s slightly more tax revenue with total nationalization, it may not offset the other drawbacks of nationalization. It’s even possible that the current 1/3 public and 2/3 private industry mix maximizes tax revenue, especially if the private sector produced output that the public SOE would have overlooked.

READER COMMENTS

foosion

Sep 15 2015 at 4:07pm

3. Suppose you know today that next year demand for your products or services will be so strong that you feel it is appropriate to raise prices in response. In that case would you be more likely to boost employment and investment today?

Isn’t this just an individualized version of 2 and isn’t the obvious answer “yes”?

Scott Sumner

Sep 15 2015 at 4:28pm

Foosion, It’s possible I still don’t have the optimal question. What we are trying to get at here is how firms would respond to expectations of higher NGDP growth. But that concept is hard to explain at the firm level. Tell Ford Motor Co. that next year people will spend 5% more dollars on their cars. I’d guess that’s good news, as Ford may think it has costs under control with long term labor contracts, but strictly speaking it does not mean Ford would sell any more units. Still, they would probably react to that news with more investment and more hiring. Thinking that costs (and car prices) will only rise about 2%.

Ak Mike

Sep 15 2015 at 4:33pm

Following up on my comment from an earlier thread, Tyler is likely wrong in implying that the power of the owners would be greater than that of the government regarding taxation of mining revenue; an opinion that is informed by the Alaskan experience, where taxes have been frequently raised here, resulting in huge revenues for the state.

The trick is to let the owners make their big investments and begin producing, then start raising the tax rates when the costs of start up are already sunk and the choice is between paying the tax or abandoning the investment and the still-substantial profits. Because I also think Scott is correct regarding the higher productivity of private owners, it seems to me a politically-driven decision to have a SOE, almost certainly resulting in lower revenues. E.g., contrast Pemex with Exxon.

David Cushman

Sep 15 2015 at 5:40pm

Scott, you write, “. . . but this isn’t really a fair criticism” and give reasons why the questions posed by the research presented at Brookings were poor. Here’s another reason. The FT writes parenthetically in the 2nd paragraph, “Inflation expectations could affect how banks and capital markets charge firms for funding, but that’s an indirect effect.” But this “indirect effect” is (I think) the primary mover in a standard ISLM expectations-augmented model. A rise in inflation expectations reduces the demand for real money, which is expansionary (the real interest rate falls). The questions in the research (at least in the quotes above) do not address this key channel.

EB

Sep 15 2015 at 7:03pm

Scott,

Unfortunately I have not been able to find a good reference of how Chile’s copper industry has been changing since the nationalisation of the old mines was completed in 1971 (in Spanish, you can read “La Viga Maestra y el Sueldo de Chile” by Patricio Meller, 2013, but it refers only to 1990-2010 and it does not discuss in detail the issues referred in your posts). You are right that private production has increased sharply starting in the late 1980s (in my view, largely the result of Pinochet’s 1980 Constitution and 1981 Mining Code that reformed the legal regime, but private companies were able to take advantage of it only after the big crisis of 1982-85).

More important, government revenue from copper has been significant for a long time (look for Wikipedia – Ley Reservada del Cobre in English and if you read Spanish search in Google for a couple of documents about the history of this law). Indeed, since the end of WWII that revenue has been quite significant when the world price was well above the average of the past 70 years (as a matter of fact, the high price just after the Military government took power was one reason why they were not interested in privatisation). In the past two years the situation has changed sharply (lower price, increases in production cost, increases in rents to workers and politicians) so government revenue from copper is expected to be much lower in 2015 and 2016.

Tyler was wrong about Chile’s copper industry and wrong about China. Look for my paper “China’s Financial Reform – The Relation between State Banks and State Enterprises” (written in 1997, based on many meetings with SOE and bank managers in China between 1994 and 1997), available in internet as WP of Hong Kong City University. I have not been able to find a detailed analysis updating my study (in particular Table 1), but I’m not surprised because I know how costly it’d be to do it.

Regarding your point about local government’s revenue from land- transferring fees, I did not do any study during my time in China, but except for large cities I have always assumed it has not been as important as local government’s access to local branches of the large state banks. Remember that one reason China has not had a fiscal crisis a la Argentina is the huge amount of private savings deposited in the state banks. It has always been my view that a sharp, unexpected decline in the flow of private savings deposited in the state banks is a sufficient condition for a banking crisis, but we still know little about the flow of private savings, in particular of that part deposited in the state banks.

Scott Sumner

Sep 15 2015 at 7:30pm

All very good comments, thanks for that information. And I basically agree with the points made.

EB, Weren’t the banks bailed out in the late 1990s, when the Chinese government took bad loans off their books?

EB

Sep 15 2015 at 8:33pm

Scott,

In 1994-97, I shared my experience about banking crises in Argentina and Chile with some PBC managers and I explained them that state banks do not need to be bailed out (in China state banks didn’t need deposit insurance and capital as it had been the practice in some Western countries to pretend that the banks are independent). More important, and contrary to what happened with private banks in Argentina and Chile, the large net inflow of private savings into the state banks was enough to play what it looked like a Ponzi game (at that time it was not possible to assess the quality of any state bank’s loan portfolio). Even if loan portfolios had not been generating enough income to pay interest on deposits, state banks would not have had a liquidity problem because they were able to get inflows of new deposits at the official interest rates large enough to finance all outflows. To my knowledge, none of the large state banks was bailed out by government or PBC transfers financed by taxation or borrowing (I never heard that there was a need to adjust PBC or state banks’ books to account for losses related to these transfers as it happened with Chile’s Central Bank in December 1983).

There is a simple way to prove that PBC and the state banks didn’t have a liquidity problem at all. To improve their consolidated asset portfolio, at that time it was decided that an increasing part of the inflow of private savings deposited into the state banks was going to be allocated to purchase U.S. Treasury bonds and other liquid foreign assets.

ThomasH

Sep 16 2015 at 7:09am

I’d think the more useful investigation would be to track the actions of those who answer one way rather than another about inflation.

On the other hand I agree that the question might try to tease out why respondents people expect prices to rise.

Rich

Sep 16 2015 at 11:55am

Scott,

Its probably a bad idea to ask this in a survey in any case because it ends up a lot of cheap talk. In reality, most businessmen don’t really know all of the pressures and changes that make them react. They move as if guided by an invisible hand. I think I might try to coin this “invisible hand” thing.

Floccina

Sep 16 2015 at 12:00pm

Wouldn’t the better question be: If people start spending more would you hire more people?

Comments are closed.