UPDATE:

See baconbacon’s comment below and my response. I may well have blown this big time.

I had been meaning to write a post about oil prices and the economy. Now this article in the New Yorker by James Surowiecki has beat me to it–and done it well.

It’s not that long and so I recommend reading it. I’ll hit one highlight and then add a couple of my own thoughts.

Investors aren’t just worried that oil is the canary in the global coal mine, though. They’re also worried that low oil prices are, in themselves, hurting the U.S. economy. For instance, as oil prices have plummeted, shale-oil drillers have sharply reduced their investments, and that has hit places like North Dakota and Oklahoma hard. These setbacks are real, but they should be seen in proportion. Even after the shale revolution, the U.S. is still very much a net consumer of oil, importing five million more barrels of oil a day than it exports. That means that the drop in oil prices has amounted to a windfall for consumers–one that Harris estimates saved them a hundred and ninety billion dollars over the past six quarters. In other words, cheap oil means Americans have an extra ten billion dollars in their pockets every month.

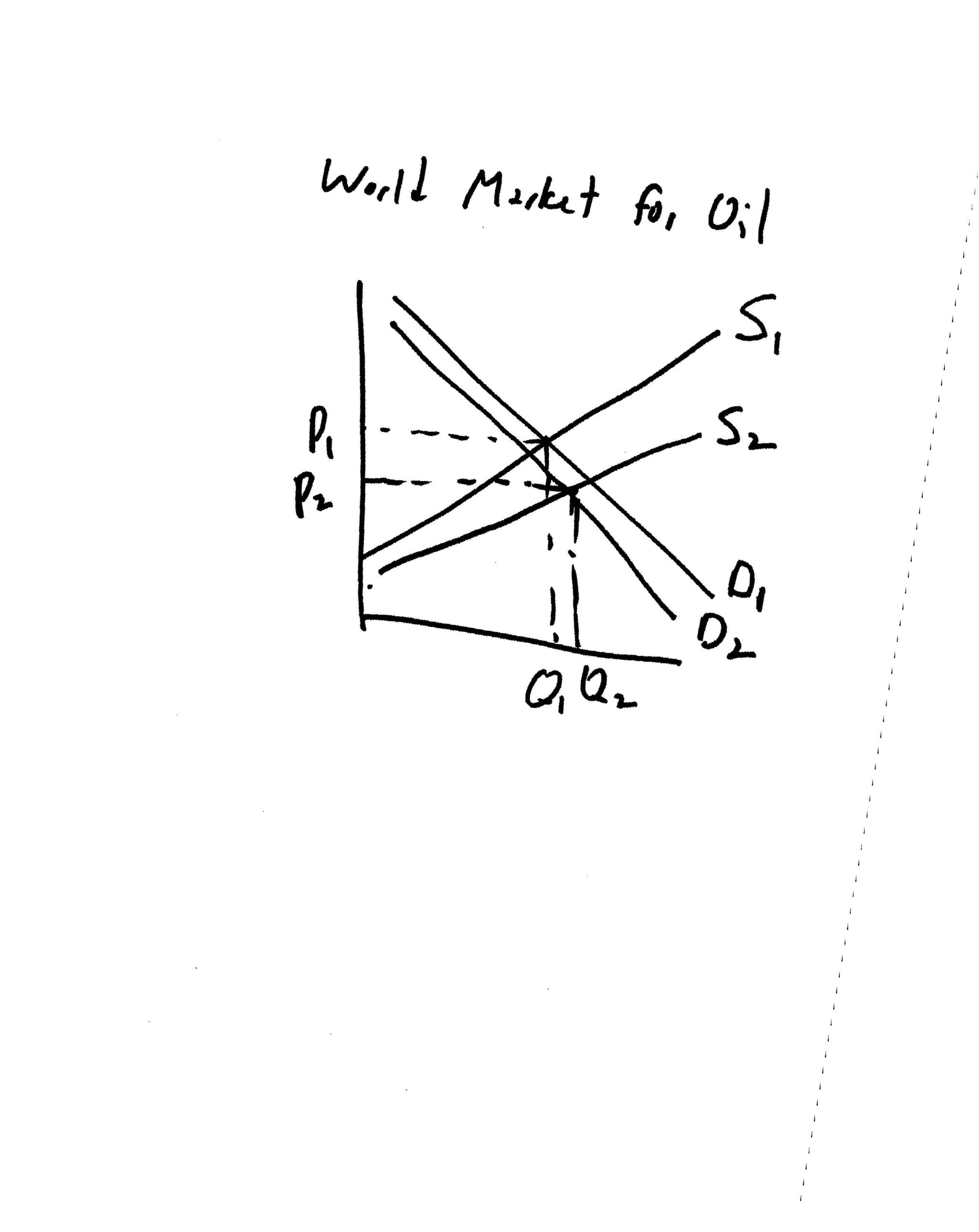

I have been saying something similar to students and colleagues who have asked. Given that the United States is a net importer of oil, a decrease in the price of oil helps consumers more than it hurts producers. Of course, we should never simply reason from a price decrease. We should always ask what caused the price change. It has to be due either to a drop in demand or an increase in supply (or some combination–see Figure above) or an increase in supply that exceeds an increase in demand. How do we tell? By checking the equilibrium quantity and not just the price. Up until recently, the equilibrium quantity has increased as the price has dropped. Specifically, from 2014 to 2015, total world production rose from an average of 93.3 million barrels per day (mbd) to an average of 95.6 mbd. From 2014 to 2015, total world consumption rose from an average of 92.4 mbd to an average of 93.8 mbd. (Why the difference between production and consumption? A build up of inventories.) Those data, combined with the approximately $45 drop in price from 2014 to 2105, suggest that the outward shift in supply exceeds any leftward shift in demand.

Had I been Surowiecki, I would not have written the last sentence that I quoted from him above. Why? Because he focuses on consumers and ignores producers. If his method of estimating is correct, then yes, consumers have an extra ten billion dollars per month. And producers have approximately ten billion dollars less a month. It’s not a wash because American producers produce less than the amount consumers consume: that’s what it means to say that the United States is a net importer. U.S. producers now produce about 75% of the amount consumed by Americans. So that means $7.5 billion a month less in the hands of producers. So the relevant net gain (I’m ignoring little bits of triangle producer loss and consumer gain) to the U.S. economy is more like $2.5 billion a month.

Also, like Surowiecki, I don’t think the drop in oil prices should have tanked the stock market. But I’m not as certain as he is that participants are making an error. Perhaps they are responding to other information. My gut feel is that he’s right in assuming an overreaction in the stock market. But that’s my gut feel, not more.

HT2 Jeff Hummel

READER COMMENTS

Effem

Feb 16 2016 at 2:06pm

The more interesting question is why the USD and oil are so highly correlated? Things are more interconnected than this type of analysis would suggest.

IVV

Feb 16 2016 at 3:35pm

Petrodollar liquidation, perhaps? As oil-producing nations need to raid their coffers to pay for things, they have to liquidate their positions in all international financial instruments, meaning increasing downward pressure on stocks, etc.?

I keep looking at how commodity prices exploded in the immediate aftershock of the financial crisis. It was clear then that it was mainly driven by a desperate grasp for returns than it was on any fundamental value of the commodities for themselves. In essence, it was tulips for everyone.

Are we perhaps seeing a similar hunt for tulips?

LD Bottorff

Feb 16 2016 at 5:13pm

It is still good news that domestic oil producers will now be able to sell their products on the world market instead of selling only on the domestic market.

Jhanley

Feb 16 2016 at 5:18pm

Thanks for this. My students were asking this the other day and it’s nice to have my answer corroborated since I’m not a real economist. But I did miss the import gap part.

I did point out to them, though, that our college has a number of alums, Canadians who came down to play hockey, learn geology, and go back home to work in the Canadian oilfields, who might not be doing so well.

baconbacon

Feb 16 2016 at 5:32pm

I don’t believe you are correct. The appropriate way to determine if it is a supply or demand shock is to look at expected demand vs actual. If oil compaies thought demand would grow by 5% and it grows by 2% that is functionally a demand shock. The best way to estimate this is to take the marginal cost of producing the extra supply. If the new price is lower than the marginal extraction cost it is most likely a failure of growth expectations, not simply a supply shift.

Anyway you slice it though one should not simply take supply from yesterday to today and determine that it is a supply shock. An increase in the supply of oil (unlike say corn which can have a surprising year due to weather) is heavily based on investment growth, and so expectations are the way to go.

Handle

Feb 16 2016 at 5:52pm

Nick Szabo has a fascinating new post that argues that a significant component of the recent decline in oil prices can be attributed to the loss of its ‘monetary premium’ (as if it deserves a place in the Divisia aggregate measures.)

Since the end of the Bretton Woods regime, oil, like gold, has had a ‘partial money’ character as an insurance hedge against fiat currency risks due to its special broad usefulness and what seemed to be a fundamental scarcity with low price elasticity of supply.

Fracking and other unconventional production has changed all that, and so we observe the popping of the ‘oil as partial money’ bubble. We don’t observe any similar change in the fundamentals of gold production, which is why the gold/oil price ratio just hit an all time high.

I haven’t done justice to the argument in this brief synopsis, so please go read the whole thing.

bill

Feb 16 2016 at 7:01pm

Nice post.

My belief is that the oil price drop has coincided with the stock drop, so some uninformed reporters connect the two. It’s as if the world economy would disintegrate if oil were free. OMG, Not that! I believe that the Fed’s tightening is the source of the stock market issues and that it would have been worse if oil prices weren’t falling at the same time.

Mark Barbieri

Feb 16 2016 at 7:47pm

As someone working for an oil producer currently going through a round of layoffs, this is a very timely post. I’m definitely not an economist, but in my layman’s view, three things are needed to determine the price of oil – the amount of supply, the amount of demand, and the value of the dollar. It seems like increasing the supply of oil should help the stock market. Decreasing demand absent a major shift to oil alternatives seems related to a slowing economy. Increasing the value of the dollar could mean a lot of things, but in this environment it smells like an overly tight monetary policy.

If the price of oil and the value of stocks changes, new information must be getting priced in. During most of 2015, oil prices went down while stock prices didn’t. I think that is because people were surprised by the inelasticity of oil supply. Later in the year, the price of oil and stocks started moving together. I’m guessing that it is because both prices were moving in response to new, negative information about global growth prospects.

Regardless of how it works, I’d be much happier if oil went back to $100/bbl.

David R. Henderson

Feb 16 2016 at 7:56pm

@baconbacon,

You may well be right. I’m stunned that I blew this by not thinking thought the inter temporal aspects given that I teach futures markets and allocation of oil over time in my class. Egg on my face. I’ll think it through and likely do another post.

Roger McKinney

Feb 16 2016 at 9:17pm

It didn’t, though it helped. We are probably in a recession now. Manufacturing, mining and transportation have been in a recession for a while. The market is down because profits have fallen for three consecutive quarters.

The collapse in oil prices is hurting banks because oil companies racked up $trillions in debt, not to mention many times that amount in derivatives.

The world-wide recession is tanking demand even as oil production continues to grow.

Yes, consumers are saving on gas, but oil producers have shut down capital expenditures and laid off thousands. Almost all of the employment gains in the US since 2008 came in the oil patch.

JK

Feb 17 2016 at 3:30pm

You cannot just look at imports and exports of oil to determine US consumption. You must look at the production and consumption of refined products. America has a lot of capacity to refine heavy oil which needs to be imported. For example, America imports heavy oil (Texas sweet won’t do) but then exports quite a bit of diesel.

Lower oil (really gasoline) prices is very good for American consumers. If America only imported oil, it is an unambiguous positive. As we produce so much oil, there is a direct hit to GDP with lower oil prices because the price is now lower. Soon, production levels will contract and we will feel the second effect. We can already see the negative effects in the sharp reductions in revenue for entities that supply and support US oil production.

Now that the US is one of the top oil producers in the world and with energy consumption as a percentage of disposable income declining due to the improved energy efficiency of everything, the price decline is not as unambiguously positive as it once was.

Michael Giberson

Feb 17 2016 at 4:33pm

Surowiecki concludes:

As baconbacon says above, expectations are key. In some sense it is obviously the case since all actions are forward looking. But the interesting question becomes why do expectations — which are always there — seem more relevant sometimes and less relevant other times.

One approach is put forward in Roger Koppl’s book Big Players and the Economic Theory of Expectations. I’ve just started reading it, but it offers the promise of a theory that explains why the action in a market may seem more driven by fundamentals of supply and demand at some times and driven by rapidly changing expectations at other times.

sk

Feb 20 2016 at 2:29pm

Most seem to attribute the fall in the price of oil to an oversupply situation and less so with actual demand being less than they anticipated. Creditors of these companies did not see it either; otherwise they would not have made loans. So, how did all these sophisticated players get it so wrong?

Comments are closed.