I don’t follow fiscal policy closely, because I don’t think it impacts the business cycle. But most economists disagree with me, and many are recommending fiscal stimulus. I argue that fiscal stimulus has no demand-side effects when the Fed is targeting inflation (as it is right now) and most fiscal packages actually worsen the economy’s supply side.

Since the debacle of 2013, Keynesians are reluctant to trumpet “experiments” in fiscal stimulus. But if they’ve become bashful, that’s no reason for us to avoid holding them to account. Between 2012 and 2013, the deficit declined rapidly, and then more slowly in 2014 and 2015 (as it typical of a recovery period.)

But this year something very strange has happened. The budget deficit has begun rising rapidly. Here is Politico:

The White House said Friday the federal budget deficit is expected to be $600 billion in 2016, an increase of $162 billion from last year.

This is quite bizarre. There is no cyclical explanation for this change, nor has there been any discussion in the news media of a major fiscal stimulus. Rather the media keeps talking about what’s wrong with our current “austerity”, and the need for more stimulus. The GOP Congress doesn’t want its voters to know that it is caving in to Obama. The Democrats don’t want voters to know what’s happening or else they might get nervous about calls for still bigger deficits. Keynesian economists don’t want this publicized, as their failed predictions in 2013 made them gun shy about actually putting their theories to a highly public test. So let’s call it the “secret stimulus”.

The Politico piece referred to the current fiscal year, which began in October 2015. (This Treasury report suggests the deficit was already increasing in the final three months of last year.) If someone has any more information on when the deficit began ballooning, please let me know.

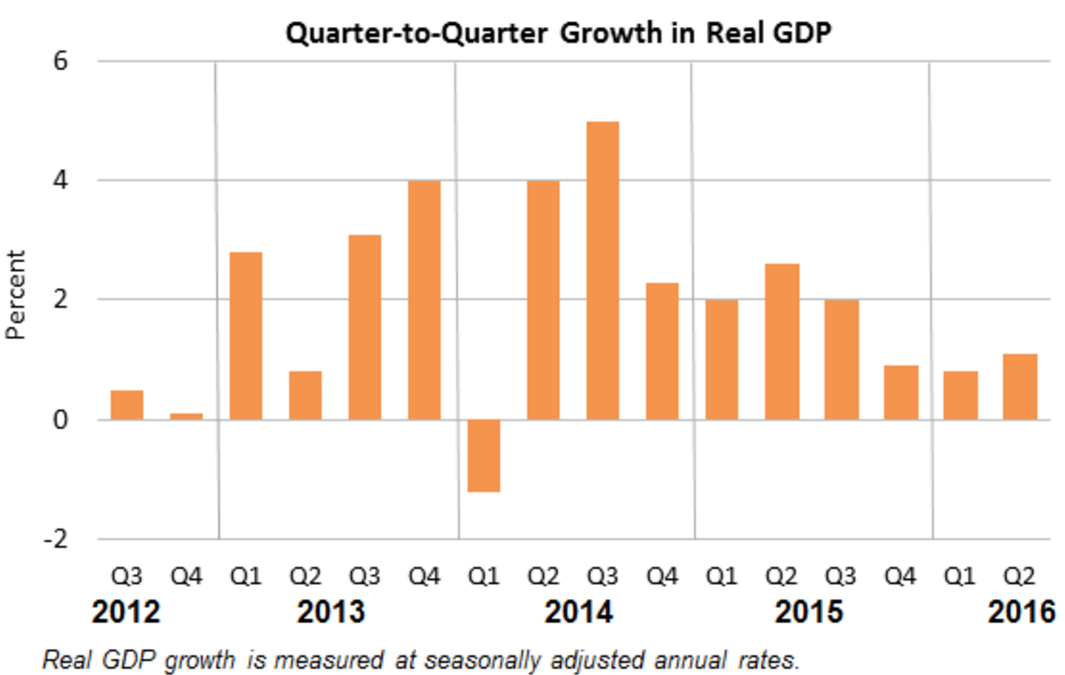

Now let’s look at how all this fiscal stimulus has impacted growth:

Notice that growth in the first three quarters of fiscal 2016 has slowed sharply, averaging about 1% at an annual rate.

Back in 2013, growth actually sped up after an austerity package was introduced on January 1st. This time, growth has slowed down as fiscal stimulus has picked up steam. In both cases the explanation is the same. In 2013, growth sped up because monetary stimulus more than offset fiscal austerity. Over the past 9 months, growth has slowed because monetary tightening has more than offset fiscal stimulus. Note that growth has not slowed in the eurozone, because the ECB is not currently trying to tighten policy.

PS. Of course NGDP is a better test of demand-side policies, but NGDP growth has also slowed in recent quarters.

PPS. Tyler Cowen has a post on a related topic. Tyler also has a post on Brexit, which indirectly addresses a point I keep making, the cyclical economic effect of “Brexit uncertainty” is very different from (and probably less than) the impact of Brexit itself.

PPPS. You might wonder why these failed experiments have no impact on economists’ confidence in the effectiveness of fiscal stimulus. So do I.

READER COMMENTS

Kevin Erdmann

Sep 13 2016 at 6:31pm

This is the beginning of anti-stimulus where corporate profits fall and corporate taxes fall, but since losses can’t be fully deducted, effective corporate tax rates rise. This is an early recession indicator, especially when the Fed is looking to tighten.

Normally, at this point, interest income would be rising, because interest rates would be rising, and investment and leverage would be rising. But, in this cycle, the natural rate has never risen above the policy rate, so the yield curve is levelling through the decline in long term rates instead of through the rise in short term rates. That means, we have the unusual situation where both interest income and corporate profits are declining at the same time, and there hasn’t been much of an investment recovery, especially in real estate. This is why we are starting to see a decline in federal revenues.

So, in this case, the fiscal deficit is an effect, not a cause.

Jeff Clemens

Sep 13 2016 at 8:59pm

On the federal spending side, this is the period over which ACA spending through Medicaid and exchange subsidies was scheduled to phase in. CBO’s projections from April 2014 have such expenditures rising from $38B in FY 2014 to $80B in FY 2015 to $141B in FY 2016.

(See Table 1: https://www.cbo.gov/sites/default/files/113th-congress-2013-2014/reports/45231-ACA_Estimates_OneColumn.pdf)

Scott Sumner

Sep 13 2016 at 9:00pm

Kevin, Yes, but the Keynesians look at the cyclically adjusted deficit. That’s their model, I am just an outside observer. And the cyclically adjust budget deficit increased sharply this year, so that’s “fiscal stimulus” according to Keynesians.

E. Harding

Sep 13 2016 at 11:50pm

Scott Sumner is right. The cyclically adjusted deficit really is soaring, and is currently at Vietnam War levels:

https://fred.stlouisfed.org/graph/?g=14Kr

Note: the majority of American voters, according to numerous polls, expect Trump to be better at reducing the deficit than Clinton. I can’t vouch for their correctness, though; their impression may well be mistaken.

James Alexander

Sep 14 2016 at 6:10am

How do you know it’s the cyclically adjusted budget deficit rising? Where are we in the cycle? Industrial Production is signalling a recession, or near one.

A lot of financial types have been onto the fall in tax revenues for a while.

https://mishtalk.com/2016/06/09/us-tax-receipts-signaling-recession/

Matthew Moore

Sep 14 2016 at 8:00am

Re PPS

Both Tyler and Scott continue to overweight the risk of an overall closing of the British economy.

They also both make the same error – saying explicitly that Leave voters are generally hostile to free trade. That is not the case, and represents an assumption of a Trump-like link between aversion to high immigration and to trade, which doesn’t exist in England. Polls indicate that the key issues were low-skilled immigration and sovereignty. Protectionism doesn’t feature.

Every single Leave newspaper or organisation, outside the fringe Hard Left, as well as the government, is calling for new free trade deals, including the Sun, the Daily Mail and the Telegraph.

I’m trying to think of how to phrase this as a bet…

steve

Sep 14 2016 at 9:36am

As you pointed out in your 9/13 post, the Fed has actually been tightening despite falling short of their inflation target. Given this, is it true to say the Fed has an inflation target? If they do, it seems like it must be lower than the current inflation rate.

Since the Fed is confused, and tightening – does fiscal stimulus make sense in order to ‘offset’ the Feds crazy tightening (which does not appear related to inflation rates, but some other unknown factor)?

Brian Donohue

Sep 14 2016 at 9:51am

Excellent post, Scott.

Scott Sumner

Sep 14 2016 at 10:03am

Thanks Jeff.

Harding, I don’t understand what that graph is supposed to show. It doesn’t seem to show the cyclically adjusted deficit. What was fiscal policy in 1982?

James, There has been no significant change in the output gap over the past 3 quarters, so I’m quite confident that the cyclically adjusted deficit has been rising fast. Any change in the actual deficit is almost identical to the change in the fiscally adjusted deficit.

Don’t focus on particular sectors like industrial production.

Matthew, You said:

“They also both make the same error – saying explicitly that Leave voters are generally hostile to free trade.”

No, I do NOT say that. UK voters tend to favor free trade. I have made a completely different argument, check out my earlier posts.

The UK is already becoming more closed to foreign investment, and the new government is committed to be more closed to labor migration. Services provided by the City may lose passport privileges, even though the British do not favor that.

E. Harding

Sep 14 2016 at 11:05am

“What was fiscal policy in 1982?”

-Very tight.

“It doesn’t seem to show the cyclically adjusted deficit.”

-It does, so far as I understand the concept.

James Alexander

Sep 14 2016 at 11:09am

I admire your confident knowledge of the output gap.

I only mentioned industrial production because it has almost always coincided with recessions. Maybe next time (this time?) it won’t.

Why do you think tax revenues are coming in below expectations? Expenses are rising in line with expectations – the big month for revenues was in April (as I expect you personally know only too well – I’ve always enjoyed your blogs on tax form filling weekends).

https://www.cbo.gov/publication/51534

Gene Frenkle

Sep 14 2016 at 11:51am

Not all spending is equal. So in 2007 the US had a very generous welfare system directed at children, mothers, elderly, and disabled. So the next welfare dollar spent would be less productive than the previous dollar because it would be directed at able bodied adults. So 2013 shows that the stimulus expanded welfare programs to able bodied adults and that the stimulus undermined the job market and once the stimulus ran out Americans began looking for jobs again.

bill

Sep 14 2016 at 12:10pm

There is an odd pattern here. It seems the Fed and BOE do their best at stimulating the economy when they are fighting against fiscal policy or a shock like Brexit. Over-offset if you will.

liberalarts

Sep 14 2016 at 6:57pm

I just googled: federal budget deficit 2016, and this was the 2nd hit, published in March of 2016:

https://www.cbo.gov/publication/51384

So 6 months ago a budget deficit of close to what they are now projecting. It makes it seem less secret. Here is an excerpt:

“CBO now estimates that if no further legislation is enacted this year that affects the federal budget, the total federal deficit for fiscal year 2016 will be $534 billion.”

Boonton

Sep 15 2016 at 6:50am

Isn’t spending going to actually have to happen before you see a change in total growth?

Scott Sumner

Sep 15 2016 at 11:26am

Harding, No, fiscal policy was expansionary in 1982–with big tax cuts and military spending increases.

James. The unemployment rate has not increased at all—it’s probably the best measure of an output gap.

Not sure what’s going on with tax revenues, or spending increases. Perhaps income is becoming more equal–which would reduce tax revenue. Did you see that real median income rose far faster than RGDP last year?

Boonton, Spending equals output—they move together.

E. Harding

Sep 15 2016 at 5:35pm

“No, fiscal policy was expansionary in 1982–with big tax cuts and military spending increases.”

-Completely unsubstantiated by the data. As you say, “Yes, but the Keynesians look at the cyclically adjusted deficit.”

Cyclically adjusted, the budget was in surplus in 1982. The deficit in 1982 is more than explicable by the extraordinary output gap at the time. Unemployment in 1982 averaged over 9% of the labor force. The deficit was less than 6% of GDP that year. By comparison, unemployment in 2009 averaged slightly lower than in 1982, but the deficit was 9.8% of GDP -much larger. Cyclically adjusted, was the deficit in 2009 all that large? I don’t think so.

There is nothing about the 1982 budget deficit which cannot be explained by cyclical factors. Only later in the Reagan administration did deficits not justified by the size of the output gap occur.

Matthew Moore

Sep 15 2016 at 7:21pm

My mistake, apologies. Those are reasonable positions.

Comments are closed.