You would think that the best way to criticize a field of science would be from the outside. After all, those within the field may be blinded by the prevailing orthodoxy, and thus be unable to see the weaknesses in the mainstream models.

Actually, the opposite is true. There are lots of excellent heterodox critiques of economics, but almost all are provided by economists. I presume this is true of other fields as well. If a problem were obvious enough to be spotted by outsiders, chances are it would already be the subject of dispute within the field. An anthropologist named David Graeber provides an excellent example of what goes wrong when you don’t understand the field you are criticizing. Here is the intro to his piece in the New York Review of Books:

There is a growing feeling, among those who have the responsibility of managing large economies, that the discipline of economics is no longer fit for purpose. It is beginning to look like a science designed to solve problems that no longer exist.

A good example is the obsession with inflation. Economists still teach their students that the primary economic role of government—many would insist, its only really proper economic role—is to guarantee price stability. We must be constantly vigilant over the dangers of inflation. For governments to simply print money is therefore inherently sinful. If, however, inflation is kept at bay through the coordinated action of government and central bankers, the market should find its “natural rate of unemployment,” and investors, taking advantage of clear price signals, should be able to ensure healthy growth.

All the economics textbooks that I’m aware of, including those written by free market “ideologues” like me, are full of examples of the various ways that government might play a productive role in the economy, including regulation of monopolies, environmental regulation, intellectual property rights, support for basic research, income redistribution, etc. Most economists are well to the left of me, and probably spend as much or more time on those issues than I do—and when teaching EC101 I spent a lot of time on the case for government involvement in the economy.

Hardly any economists believe that it is sinful for the government to print money. Most agree that the money supply should be adjusted to reflect changes in the demand for money.

It’s not a good sign when you write a very long article telling readers that economics is bunk, which starts off with a series of assertions about economic that are wildly inaccurate. Unfortunately, it gets even worse. For instance, Graeber talks about the reality of “magic money trees” a myth I exposed in my previous post. Then he suggests that little is left of the British welfare state:

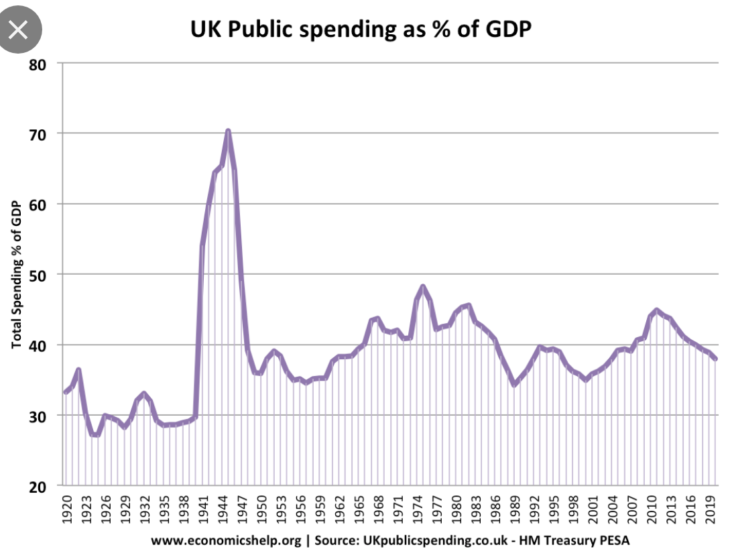

It was center-left New Labour that presided over the pre-crash bubble, and voters’ throw-the-bastards-out reaction brought a series of Conservative governments that soon discovered that a rhetoric of austerity—the Churchillian evocation of common sacrifice for the public good—played well with the British public, allowing them to win broad popular acceptance for policies designed to pare down what little remained of the British welfare state and redistribute resources upward, toward the rich.

Actually, government spending in the UK (mostly entitlements) is just under 40% of GDP. As in most countries it is countercyclical, but there is no long-term trend downwards:

Economists, for obvious reasons, can’t be completely oblivious to the role of banks, but they have spent much of the twentieth century arguing about what actually happens when someone applies for a loan.

I’ve spent most of my life studying monetary economics, and I was completely unaware that economists had spent most of the 20th century arguing about what happens when someone applies for a loan:

One school insists that banks transfer existing funds from their reserves, another that they produce new money, but only on the basis of a multiplier effect (so that your car loan can still be seen as ultimately rooted in some retired grandmother’s pension fund).

Here he is conflating two unrelated issues, whether the money multiplier is a useful concept and whether the funds for borrowers come out of saving. The money multiplier is the ratio of the change in the broad money supply (including bank deposits) to the change in the monetary base (cash plus bank reserves.) That’s all. No one thinks it is constant. When people start talking about how economists are “wrong” about the money multiplier, I suggest you stop reading.

Only a minority—mostly heterodox economists, post-Keynesians, and modern money theorists—uphold what is called the “credit creation theory of banking”: that bankers simply wave a magic wand and make the money appear, secure in the confidence that even if they hand a client a credit for $1 million, ultimately the recipient will put it back in the bank again, so that, across the system as a whole, credits and debts will cancel out. Rather than loans being based in deposits, in this view, deposits themselves were the result of loans.

The one thing it never seemed to occur to anyone to do was to get a job at a bank, and find out what actually happens when someone asks to borrow money. In 2014 a German economist named Richard Werner did exactly that, and discovered that, in fact, loan officers do not check their existing funds, reserves, or anything else. They simply create money out of thin air, or, as he preferred to put it, “fairy dust.”

So now we’ve gone from magic money trees to fairy dust. I feel like I’m in a Philip Pullman novel. This is a nice example of what’s called the “fallacy of composition”, the distinction between the individual case and the aggregate. An individual can unilaterally change all sorts of economic variables. If I decide to retire tomorrow, then employment falls, GDP falls, saving declines, etc. But that does not mean that a theory of the determination of aggregate employment, GDP, etc., should try to explain those variables by analyzing changes in the public preference for working. Instead, both left and right wing economists focus on the underlying drivers of employment. Keynesians might emphasize aggregate demand whereas conservative economists might emphasize how government programs and taxes impact incentives. Hardly anyone thinks that employment fell in 2009 because lots of people suddenly wanted more leisure time.

Similarly, an individual banker can make a decision that causes aggregate loans and deposits to be a bit higher than before she made that decision, but this does not mean that bankers determine the aggregate money supply, at least in any meaningful sense. Bankers respond to macroeconomic conditions such as changes in the monetary base, interest rates, capital requirements, reserve requirements, loan regulations, etc.

An auto executive will not consult the data on global oil production when deciding how many cars to build. But if the oil industry were not producing petroleum, then very few cars would be built.

Historically, the feeling that bullion actually is money tends to mark periods of generalized violence, mass slavery, and predatory standing armies

Hmmm . . . does “tends to mark” suggest “causation” or just “correlation”? I ask because I also believe that “bullion actually is money”.

There’s lots more criticism of behavioral assumptions such as self-interest and rationality. Most good economists understand that these are merely approximations of reality, useful for some purposes but not others.

READER COMMENTS

Mark Z

Nov 23 2019 at 4:20pm

“…bankers simply wave a magic wand and make the money appear, secure in the confidence that even if they hand a client a credit for $1 million, ultimately the recipient will put it back in the bank again, so that, across the system as a whole, credits and debts will cancel out.”

If I’m a bank and have a $100 deposit from a depositor, and I’m considering whether to loan that $100 to a borrower, even if I know to a certainty that borrower will pay me back, if I know the depositor will likely want the $100 back before the borrower returns it, this limits by ability to make the loan. People don’t put their money in banks for eternity. Time is a factor. Withdrawals and deposits netting out ‘as t approaches infinity’ doesn’t change the fact that current deposits constrain how much I can loan out today. And I’m pretty certain banks do indeed use mathematical models of expected withdrawals and deposits to determine how much they can afford to lend, regardless of whether the loan officer knows what the model is. Maybe I’m missing something?

Scott Sumner

Nov 23 2019 at 6:50pm

Mark, Yes, there certainly are constraints on banks balance sheets,

lat

Nov 24 2019 at 3:40am

You’re not missing anything, but I guess Werner and Graeber are. As a banker that’s worked in credit all my banking life, I can guarantee that your statement here is more accurate than their interpretation.

Alex

Nov 25 2019 at 2:40am

I’ve been working in risk management for quite a while and I’ve never heard anyone telling me that there is a constraint on (otherwise profitable) lending because the bank has not enough matching deposits, so my personal experience matches Graeber’s description.

Ricardo

Nov 25 2019 at 1:26pm

Isn’t that what the interest rate would tell you? Just pay depositors a bit more… they’ll increase their deposits, and then you can fund those loans. Repeat until equilibrium.

Alex

Nov 25 2019 at 3:38pm

Yes, this is correct. Also in addition to individual depositors there are other banks who are more than happy to lend you money, again, assuming that there are profitable lending opportunities. Finally banks by definition can borrow from the central bank.

Mark Z

Nov 26 2019 at 2:21am

There was a post awhile ago at Alt-M.org by someone who worked in finance who said (he was writing in general that banks don’t function in practice as MMT theorists say they do) banks tend to avoid borrowing from the central bank unless they have to, as it signals to other banks that they’re in bad shape, so they can’t just borrow at will with impunity. (I looked up the post, it was by Julien Noizet. https://www.alt-m.org/2019/03/15/friday-flashback-the-problems-with-mmt-derived-banking-theory/)

lat

Nov 25 2019 at 5:19pm

Dunno if you’ve been at a commercial/retail bank, but asset-liability management and the associated risks has been central at each institution I’ve worked for. Maybe it’s just a characteristic of smaller community institutions?

It’s not about having 100% matching deposits, but rather that deposits are generally your cheapest source of funds (often by a large margin) so any changes there requires changes in your lending strategy. Changing the composition of your funding sources or deciding to do things like increase deposit rates can very easily make previously profitable lending opportunities no longer profitable. Loan officers will usually be required to run a cursory profitability analysis prior to even accepting a completed application, so I’d still say Mark Z’s comment is more accurate than Graeber’s.

Garrett

Nov 23 2019 at 11:25pm

Scott Alexander has a post about external versus internal criticisms of a science that hits similar points.

BC

Nov 24 2019 at 7:23am

I think Tyler Cowen once said that one of the most useful applications of economics was pointing out how non-economists’ common conceptions were wrong. An example might be the minimum wage: most non-economists view the minimum wage as a way to boost wages, without considering that the minimum wage actually acts as a barrier to employment. Many people don’t like being told that their intuition is flawed. In fact, a common cliche is that one should defer to “common sense” and one’s “gut instincts”. Perhaps, that’s why economics seems to attract more outside criticism than other fields.

ChrisA

Nov 24 2019 at 9:11am

If David Graeber is the best critique that is available of modern economics, I would suggest it is in a pretty good place. He is obviously starting from a conclusion – he has often stated his dislike of modern capitalism – and trying to find reasons why. Instead of starting with an insight and then showing a contradiction. Not surprisingly his thinking is incoherent. The real question is why a prestigious journal like NYRB would print his article, but of course the publishers of such things nowadays are not concerned about truth anymore but getting people to click.

Thaomas

Nov 24 2019 at 9:38am

Most of the problem is that what the public thinks of as what “economists” think is that journalist seldom use academic economists as there sources. In the midst of the “hyperinflation” “debasement of the currency” scare after the 2008 crisis, who knew that economists actually thought that fiscal and monetary policy ought to be doing more, not less, to combat the recession? When an article about dealing with climate change comes out do they interview Nordhaus? Where is the journalist covering the trade wars talk with an economist who could explain that exporters are harmed by import restrictions or that trade restrictions do not affect the trade balance?

Fred

Nov 24 2019 at 2:16pm

Kibitzers are prevalent in lots of fields. Right now, there are tens of millions of people who complain about the third down play calling by the pros. Economics has very important impacts on all; thus we feel strongly.

As a somewhat ignorant observer, the idea that economic pros know what they are doing doesn’t seem quite right. In the 1970s, we were offered Whip Inflation Now buttons that didn’t do much. Fifteen years ago, we headed into a Great Recession that played out despite economic advice. Right now, we have a large deficit and a tariff war which I have been told were bad things, but the economy seems good. Maybe I’m missing something. How does economic theory explain Bitcoin which doesn’t even have a government behind it?

Christophe Biocca

Nov 24 2019 at 6:05pm

Why would a currency require government backing? Gold isn’t backed by any government, and has a long history of being used as currency. Many US banks issued their own notes during the free-banking era.

The belief that a currency requires a government in order to function is not something held by economists, but by the public, and is largely due to the current absence of large-scale private currencies. But there are plenty of historical examples to the contrary.

Lorenzo from Oz

Nov 24 2019 at 4:51pm

Graeber is frustrating. He can come up with some intriguing ideas and then fluffs the execution by getting key aspects (the economics, the history, etc) wrong. And generally wrong for the same reason: grounding everything in some “the ruling class of capitalism is to blame” story.

Consider his concept of “bullshit jobs“. He entirely almost entirely fails to notice that they are jobs mostly about dealing with the state, or are in the state, etc. In other words, the coercive end of social/institutional structure.

His book on debt has some striking ideas, mixed up in some amazingly sloppy history. (E.g. it was true that, up to WWII, public debt tracked military expenditure, but, contra what he claims in the book, that is no longer true.) Not to mention a sort of money-denialism (it is all just credit/debt really).

He also led the charge to have Noah Carl sacked from his academic position, so is one of the multiplying enemies of freedom of thought.

Mark Z

Nov 26 2019 at 2:26am

I’m not sure the general point of this post is right: some fields are better at critiquing different fields than others; and some may be better at critiquing different fields than those fields are at critiquing themselves. I’d take economics’s critique of anthropology more seriously than anthropology’s critique of economics. I take statisticians’ critique of social psychology more seriously than vice versa; and I think I’d take what statisticians’ have to say about the state of social psychology more seriously than what social social psychologists have to say about the current state of social psychology.

Todd Kreider

Nov 26 2019 at 10:02am

Then again, both Call of Duty: Modern Warfare 2 and Grand Theft Auto IV: The Ballad of Gay Tony were released in 2009.

Comments are closed.