George Selgin’s new Cato working paper demolishes the now fashionable view that banks are not intermediaries between savers and borrowers. (It’s a sad comment on our profession that the paper needs to be written.) Toward the end of the essay Selgin makes the following observation (on page 41):

Yet there’s a fundamental sense in which banks are strictly intermediaries. It is the sense one gains by thinking in terms of real, long run or general equilibrium magnitudes. That is, by thinking of banking in the same way economists think of other industries.

That changes in the nominal quantity money are at least roughly “neutral” in the long run is perhaps the most fundamental tenet of neoclassical monetary economics. It doesn’t mean that monetary expansion never has important real short-run

consequences: most obviously, it can lower unemployment when the cause of that unemployment is a lack of aggregate demand. But it doesn’t generally alter the relative size of particular industries, or of firms within them. Instead of depending on the

nominal quantity of money, firms and industry’s success or failure depends on the real demand for their products.

My critics often tell me that I don’t understand banking, and that’s why I believe in a supposedly fictitious “money multiplier”. In fact, I don’t need to understand anything about banking to determine the money multiplier. That’s because the long run money multiplier in banking is exactly the same as the long run money multiplier in any other industry.

This claim may sound a bit over the top, so let me clarify that money multipliers defined in the conventional way do differ from one industry to another. The usual definition is the change in the broad money supply divided by the change in the monetary base. But that’s not a very convenient definition. It makes more sense to define the multiplier as the percentage change in a broad money aggregate divided by the percentage change in the monetary base. By that definition, the long run money multiplier is precisely one. And that follows from the long run neutrality of money:

The long run effect of an exogenous increase in the monetary base is a proportionate increase in all nominal aggregates.

Suppose I’m told that there’s a planet circling Alpha Centauri. And this planet contains a civilization. And the civilization contains an industry entitled @#$%&. We have no information as to what product @#$%& produces. We don’t even know whether it produces a good or a service. My claim is that I can predict the money multiplier for industry @#$%&. In the long run, an exogenous 47% increase in the (fiat) monetary base on this faraway planet will produce a 47% increase in the nominal size of industry @#$%&.

So the problem is not that I don’t understand banking, it’s that my critics don’t understand the long run neutrality of money. An exogenous increase in the monetary base has no long run impact on the real demand for base money. My critics confuse nominal and real variables, assuming that a purely nominal effect is somehow “real”. Nominal shocks can have real effects in the short run, but those effects are due to sticky wages and prices. These short run effects reveal nothing at all about the fundamental role of banking in the economy. Banks are intermediaries between savers (lenders) and borrowers.

PS. Does it matter if this faraway planet has the floor system, where it pays interest on bank reserves (IOR)? It matters for some questions, but it doesn’t matter for the long run money multiplier in response to an exogenous increase in the monetary base. Peter Ireland showed that the best way to think about IOR is as a one-time shift in the demand for reserves. Even with IOR, long run money neutrality continues to hold true.

PPS. By “long run”, I mean in the period after all sticky wages and prices have fully adjusted to the monetary shock.

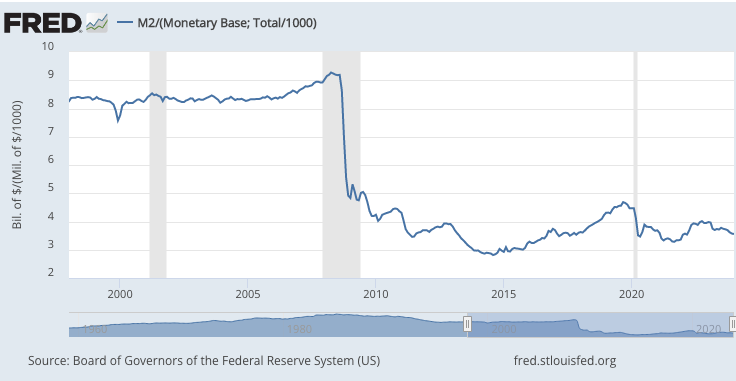

PPPS. Here’s the M2 multiplier, showing the effect of IOR (in late 2008) and other factors such as changes in nominal interest rates and forward guidance:

READER COMMENTS

dlr

Mar 22 2024 at 4:25pm

scott, i’ve seen you link the ireland paper before but i have never been persuaded it shows much but a unhelpfully stylized possibility of determinate equilibria, similar to many woodford cashless nk papers. is it a convincingly pragmatic story of how lowering and raising a stock dividend in a floor system with permanently satiated reserves and nonbinding reserve constraints attains a determinate price level equilibria while also even vaguely matching our actual world? it sure doesn’t look like it does.

normally when talking about ior, you talk more mechanically about the fed manipulating “demand for reserves” (sort of as if determinacy were not a consideration and supply could be held exogenously constant or as if we didn’t have a forever floor system) as opposed to ireland’s version of what seems like clumsy over-reliance on artificially modeled deposit wedges and ultimately just more plausible equilibria selection. what specifically do you like about his model as it applies to the real world?

Scott Sumner

Mar 23 2024 at 1:08pm

The intuition here is that the neutrality of money is an extremely powerful concept. Yes, IOR makes for much larger and more variable demand for reserves. But banks still need to decide on optimal REAL reserve holdings. And in that case exogenous changes in the base do not have any long run impact on real reserve demand. (Unless you believe that monetary policy permanently impacts the real interest rate, which seems very unlikely.)

Ahmed Fares

Mar 22 2024 at 11:09pm

A good paper, but it didn’t demolish anything. The best way to understand a bank is to actually run one. In the following simulation, after selecting “NO, Text Only” in the popup, click the button on the top-right which says “Issue $25 Loan”. Note how the bank’s balance sheet expands with the $25 loan creating a new $25 deposit that was created out of thin air. That new deposit could not have come from anywhere else because the bank’s existing deposits were untouched.

How Loans Create Money

Scott Sumner

Mar 23 2024 at 1:14pm

So in that case a person has loaned money to themself, using a bank. The bank might pay 2% interest and charge 5% on the loan. So answer this question: Why would a person loan $25 to a bank at 2%, and then borrow it right back at 5%? That doesn’t seem very smart, does it?

Now you might say the person depositing the money is different from the person borrowing the money. That’s intermediation, right?

Ahmed Fares

Mar 23 2024 at 8:44pm

“Everyone can create money; the problem is to get it accepted.” —Hyman Minsky

Banking is an IOU swap. The bank swaps its IOU which is accepted in the market for yours, which doesn’t trade as well. It’s a form of financial alchemy, made possible by the bank’s equity. The bank earns a return on its equity by the spread between those two interest rates. That return on equity includes the default risk of your IOU. You bear it, so the public doesn’t have to.

I Googled IOU swap and came up with this, which also mentions maturity transformation:

There’s a picture in the article of that IOU swap.

Game of Transformations: the Liquidity Version

Ahmed Fares

Mar 23 2024 at 12:15am

I consider Richard Werner to be the world’s leading expert on banking. He did the first empirical study of banking in 5,000 years. In the following video, he discusses the three theories of banking: the financial intermediation theory of banking, the fractional reserve theory of banking, and the credit creation theory of banking.

The latter, which is the oldest, is the correct theory. Interestingly, as noted in the video, Keynes started with the credit creation theory, then moved to the fractional reserve theory, then moved to the financial intermediation theory, becoming wronger and wronger over time.

How Banks Create Money Out of NOTHING – Richard Werner

Here is an abstract of the paper referred to in the video:

The link to the pdf file can be found here:

Can banks individually create money out of nothing? — The theories and the empirical evidence

Scott Sumner

Mar 23 2024 at 1:16pm

“I consider Richard Werner to be the world’s leading expert on banking. He did the first empirical study of banking in 5,000 years.”

Is this a joke?

Ahmed Fares

Mar 23 2024 at 9:01pm

Richard Werner is also the guy who invented Quantitative Easing.

The expert who pioneered ‘quantitative easing’ has seen enough: Central banks are too powerful and they’re to blame for inflation

This from Wikipedia:

Quantitative easing

spencer

Mar 23 2024 at 12:50pm

Dr. R. Alton Gilbert in the Fed’s bible: “Requiem for Regulation Q: What It Did and Why It Passed Away” naively asked the wrong question. His implicit and false premise was that savings are a source of loan-funds to the banking system. Gilbert assumed that any potential primary deposit (funds acquired from other DFIs within the same regulated boundaries), were newfound funds to the payment’s system as a whole.Thereby in his analysis, Gilbert also assumes that every dollar placed with a non-bank deprives some commercial bank of a corresponding volume of loanable funds. However, saver-holders never transfer their funds out of the payments system unless they hoard currency or convert their funds to other national currencies. This applies to all investments made directly or indirectly through intermediaries. Gilbert asked: Was the net interest income on loans/investments derived from “attracting” these savings deposits (viz., outbidding other DFIs for the same stock of core deposits), greater than the interest attributable to the direct and indirect operating expenses of endogenous retail and this wholesale “funding” [sic]? The question is not whether net earnings on CD assets are greater than the cost of the CDs to the bank; the question is the effect on the total profitability of the commercial banking system. This is not a zero sum game. One bank’s gain is less than the losses sustained by the other banks in the System. The whole (the forest), is not the sum of its parts (the trees), in the money creating process.

Matthias

Mar 25 2024 at 8:20pm

Why would converting your money into a different currency have an effect any different from ‘converting’ your currency into donuts or into a house?

In all cases, you spend eg dollars to buy eg euros, donuts or houses. And then the seller has to worry about what to do with the dollars.

Philippe Bélanger

Mar 23 2024 at 3:59pm

Since 2013, Japan’s monetary base has increased more than six fold, while M2 has increased by around 20%. And during most of that period, interest rates on reserves were negative. You would think that 10 years would be enough for prices and wages to adjust. But the percentage increases of these monetary aggregates have been nowhere near identical.

Scott Sumner

Mar 23 2024 at 6:51pm

Once again, the multiplier concept does not imply that the money multiplier is constant, even in the long run. It responds to multiple factors including IOR, market interest rates, regulation, and many other factors. The claim is that an exogenous increases in the monetary base causes a proportional increase in the aggregates, in the long run. Many central banks increase the base in response to higher commercial bank demand for reserves. Given the low inflation rate in Japan, that was almost certainly the case with the BOJ.

Philippe Bélanger

Mar 24 2024 at 3:01am

But what caused the real demand for base money to increase? As I said, interest rates on reserves in Japan were negative for most of that period. And inflation has not been noticeably higher. In fact, inflation for consumer prices has been, on average, higher since 2013 than it was in the preceding years. So I don’t see why the demand for reserves would have risen. And we should be able to identify what caused large changes in the money multiplier. Otherwise this theory becomes untestable, since we can always attribute any change in the money multiplier to an unobservable cause.

Philippe Bélanger

Mar 24 2024 at 3:06am

Typo: I meant that inflation has not been noticeably lower.

Scott Sumner

Mar 24 2024 at 12:10pm

I don’t have enough knowledge of Japanese banking to know why their banks have chosen to hold much larger real reserves over time. I would note that Japanese 10-year bond yields fell substantially between 2008 and 2020:

https://fred.stlouisfed.org/series/IRLTLT01JPM156N

That may have made reserves a relatively more attractive asset (compared to bonds.)

There may be other factors as well. But I do agree with the sense of your question in one respect—the money multiplier is not a very useful concept for policy purposes, which is why I reject traditional monetarism, and prefer NGDP targeting over M2 targeting.

Ahmed Fares

Mar 24 2024 at 12:29am

Philippe,

For Scott, this issue is existential.

The monetary base is special

Incidentally, I’m not saying that Scott is right or wrong about this because I’m not smart enough to understand this, and it’s not for lack of trying. As an aside, and as regards the “hot potato effect”, MMTers pushed back.

Sumner’s Cold Potatoes

Ahmed Fares

Mar 24 2024 at 8:34pm

Philippe,

Scott discussed the Japanese case in an article many years ago. Selected quotes and then a link (I included the first sentence because Scott is a funny guy.):

Where MMT went wrong

spencer

Mar 24 2024 at 10:13am

Supposedly, the base ceased to be a base for the expansion of bank credit after Greenspan dropped reserve requirements by 40 percent. Then the base was changed from containing nonearning assets to earning assets. So, the money multiplier was deliberately eroded.

Warren Platts

Mar 30 2024 at 5:55am

I was hoping the article actually was about Mars. Respectfully request an article on what a Martian economy would be like!

Comments are closed.