Even prior to the financial crisis, the median duration of unemployment was in severe recession territory. Now, it is through the roof.

In manufacturing, it almost appears that employment and output are decoupled. Output can increase while employment declines or just edges up.

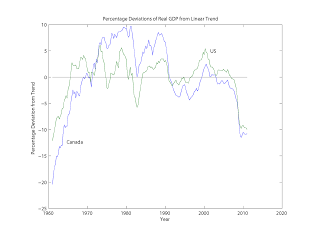

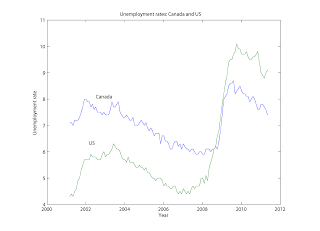

Finally, Stephen Williamson compares Canada and the U.S. in terms of output relative to trend and the unemployment rate.

The output drops are similar, but the unemployment rate behavior is not. Note, however, that I prefer the employment/population ratio to the unemployment rate.

Only half of the drop from 2000 to present took place during the 2008-2009 recession. And I think even that represents an acceleration of structural unemployment. What fraction of those jobs do we think are coming back?

Or, to put it another way, where do you think that ratio would be today if nominal GDP had remained on its trend? I think it would still be under 60. The extra nominal GDP would show up in part as a higher price level and in part as more jobless output, as in the graph of manufacturing above.

READER COMMENTS

eric

Jul 1 2011 at 5:07pm

If you get out of the military and would like to go to school instead of fighting pointless wars they let you have unemployment for 99 weeks.

Those on unemployment that really don’t have a desire to work skew the results.

shawneriksmith

Jul 1 2011 at 6:16pm

Looking at the chart of median duration of unemployment and unemployment rate, it appears they were highly correlated during the 1980’s. Around 1992, it appears they became decoupled with median duration of unemployment remaining high while unemployment rate decreases. It would be interesting to see the data pre-1980, but any thoughts on why this began happening in the mid-90’s?

My thoughts are that is when computers and automation became a larger and larger force in corporate America…resulting in many of the unemployed not properly trained in this new regime of programming, powerpoints, etc.

Nathan Smith

Jul 1 2011 at 9:43pm

“Only half of the drop from 2000 to present took place during the 2008-2009 recession.”

Huh? It was about 64 1/2% in its 2000 peak, 63 1/2% at its 2007 peak. Now it’s 58 1/2%.

“Or, to put it another way, where do you think that ratio would be today if nominal GDP had remained on its trend?”

Looks to me like if the 2001-2007 expansion had continued, the ratio would have regained its 2000 peak.

Chris Koresko

Jul 2 2011 at 2:13am

shawneriksmith: “Looking at the chart of median duration of unemployment and unemployment rate, it appears they were highly correlated during the 1980’s. Around 1992, it appears they became decoupled…”

I’d take that with a big grain of salt. Note that the two curves on that graph are in different units (time and dimensionless ratio). So the authors are free to scale the curves arbitrarily for plotting purposes. They appear to have chosen a scale factor close to 1 week per percent. That makes the curves line up nicely in the 1980s. A scale factor of something like 1.7 would have made them line up in the 1990s, and a scale factor of around 2.0 in the 2000s. The correlation between the curves looks like it’s not too different over those periods once the scale factor is chosen appropriately.

My hypothesis is that we’re mostly seeing the effect of policy changes, e.g., the availability of unemployment insurance.

Nathan Smith

Jul 2 2011 at 9:24am

Well, for what it’s worth, I do think there’s a real trend here, not one that makes structural employment inevitable, but one that makes it more likely. Job skills are becoming less substitutable for each other. More of the simple jobs that you could learn how to do in a few days are automated, taken over by computers. The new jobs that arise from these are at a higher level, they require more specifically human qualities, like judgment and intuition. Since those are harder to cross-apply to different jobs, and to appraise, the process of matching people with jobs is slower. That’s just a guess, I don’t have data to back it up.

CBBB

Jul 2 2011 at 1:21pm

The structural unemployment, if it exists, has NOTHING to do with training or educational levels. This is a key point. I hear a lot of this stuff like shawneriksmith says where it’s assumed there’s structural unemployment because all these high-school drop out construction workers don’t know how to use computers or powerpoint or whatever. This is a complete crock.

There’s tonnes of university graduates from the last few years – people who should be considered to have been properly trained and educated, and I’m talking about people with science and engineering backgrounds who simply can’t find jobs in their field. Why? Is it because they don’t know how to use computers or something? No, it’s because a general lack of demand in the economy means employers can now insist all new hires have 5-10 years professional experience in the field.

I don’t buy the argument that there’s structural unemployment because not enough workers know how to use computers, etc. No amount of training or education is going to solve this problem as long as employers demand years and years of specific experience and they’ll be able to do this as long as there is no incentive to expand production.

It’s as simple as that.

Cliff

Jul 2 2011 at 4:24pm

CBBB, what you have described is not structural unemployment, but cyclical unemployment. However, I doubt your anecdote-based conclusions. In many industries there is a huge number of open positions that employers cannot fill- due to unavailability of sufficiently skilled prospects.

JonF311

Jul 2 2011 at 5:59pm

Re: My hypothesis is that we’re mostly seeing the effect of policy changes, e.g., the availability of unemployment insurance.

Unemployment insurance has been around for a rather long time– it did not just pop up in the 90s. And in fact the value (in real dollars) of unemployment payments has dropped steadily over time, due to inflation, since the payments are not adjusted with any sort of COLA formula. As originally designed, UI was supposed to replace 2/3 of a worker’s income from his former job; nowadays the median number for that is about 1/3 of former wage income.

Whenever this topic coimes up I am astounded by the ignorance of people who make sweeping claims about unemployment insurance. I am forced to conclude that neither they nor anyone of their close acquaintance has ever been on unemployment.

Chris Koresko

Jul 2 2011 at 6:19pm

JonF311 :“Unemployment insurance has been around for a rather long time– it did not just pop up in the 90s. And in fact the value (in real dollars) of unemployment payments has dropped steadily over time, due to inflation, since the payments are not adjusted with any sort of COLA formula…. I am astounded by the ignorance of people who make sweeping claims about unemployment insurance.”

I freely admit being ignorant of the changes to unemployment insurance over the last several decades. Please enlighten me.

It seems to me that there are several characteristics that could affect its impact on the mean duration of unemployment: availability (how many workers are covered), attractiveness (how does the insurance payment compare to normal pay), and duration (how long can one stay on unemployment before the payments are substantially reduced or otherwise made less attractive).

My impression is that the latter is currently at an all-time high. Is this not true?

CBBB

Jul 2 2011 at 7:21pm

@Cliff

If that’s true – which I HIGHLY doubt, then employers in those industries should raise wages – that’s the market solution. Instead they whine and whine and demand the government spend more taxpayer dollars pumping out more grads so they can hire engineers with 10 years experience for $10/hour.

quadrupole

Jul 2 2011 at 10:23pm

CBBB

I work in tech… do you have data about folks with engineering and science degrees not finding jobs?

I ask, because from the inside, the job market for folks with strong technical skills looks red hot.

Troy Camplin

Jul 3 2011 at 7:53am

Regarding the first graph, might the duration have something to do with the length of time one is allowed to remain on unemployment? After each increase in the length of time since 1990, have we reduced that length? Or do we just keep adding on?

CBBB

Jul 3 2011 at 12:59pm

@quadrupole

This is sort of my point. What does “strong technical skills” mean? Well from what I see it means, not just a degree in CS/Engineering/Math but absolutely no less then 5-10 years of professional experience in half a dozen technologies. I’ll believe the demand for software developers is red-hot when I see employers willing to take on graduates who maybe only have an internship or two under their belt.

My point was that so-called “structural unemployment” gets seen by people as a matter of proper training or education. However in reality many employers don’t consider people qualified unless they also have years of relevant work experience. Once you have any substantial period of high unemployment you’re going to get these structural issues not because of some general lack of education or knowledge but simply because in periods of high unemployment getting on the experience ladder becomes more difficult.

So cyclical unemployment can become structural but structural unemployment can largely be solved using cyclical policies.

I really don’t believe that it’s all a bunch of “stupid jock” construction workers who “should have studied harder” like a lot of people around here seem to think.

Troy Camplin

Jul 3 2011 at 3:56pm

CBBB raises a valid point. I’m looking hard for a job, and running into exactly this problem. More, there does not seem to be an understanding that, if you have a Ph.D. that would allow you to teach something like technical writing (especially with my background), that that means you are in fact more qualified than the undergrad in technical writing who would have necessarily learned what he learned from you. “No, I don’t have an undergrad degree in technical writing, I have a Ph.D. in the humanities and a M.A. in English.” […] “Oh, that means I’m unqualified? You’re an idiot.” Of course, such issues raise the real problem that people cannot think for themselves or understand what they are doing when they can’t understand how someone can be qualified for a job even if they don’t have the specific degree for it.

CBBB

Jul 3 2011 at 6:44pm

@Troy Camplin – most hiring decisions are made by HR people who have little actual knowledge of the industry or position. This is an important point totally ignored by economists.

If your qualifications are not an exact match this is consider structural unemployment even though in REALITY it isn’t. If demand were high then employers would have no choice to take partially or near matches rather then having the option, as they do now, of waiting months maybe a year to fill a position until an exact match comes along.

I absolutely refuse to believe that structural issues are the problem here until it’s proven that companies really can’t find people to fill these positions (can’t find exact OR close matches) rather then just insisting on getting exact matches. Remember the big issue is usually years of experience something that you really can’t acquire on your own without a job.

A little anecdote of my own – after successfully completing 4 technical interviews for a software development jobs I was turned down after a 5th interview because apparently “I didn’t seem enthusiastic and passionate enough about the product/company”. If these are the reasons for not hiring someone I really question how “red hot” the tech sector is.

Shayne Cook

Jul 4 2011 at 11:17am

@ CBBB …

You are partially correct in your observations. But the current U.S. economic situation is not exclusively cyclical or structural in nature. All recessions/economic downturns have cyclical components/characteristics – this one, as you’ve noted, has several cyclical characteristics. What Arnold (here) and others note – and I concur – is that this recession/recovery has far more structural artifacts than many economists and policy-makers originally recognized.

The proscribed remedy for purely (or largely) cyclical downturns is for both fiscal and monetary policy to be adjusted to (artificially) stimulate demand – through both borrowing/tax-relief (government) and money-printing/interest rate easing by the Fed. That is the ‘Keynesian’ remedy and has been effective in shortening/attenuating past cyclical recessions. But you’ll agree there has been an extraordinarily high degree of both government borrowing/tax-relief and Fed money-printing going on for the past 4 years. And it has resulted in an extraordinarily non-robust recovery. There is then a more substantial structural component to this current U.S. economic situation than many realized. And additional ‘proscribed remedy’ will be increasingly ineffective (counter-productive) in addressing the structural artifacts. More money being showered on the economy, either from the Fed or the Federal Government, will not improve the situation. Nor will ‘more regulation’ of business (read force from the Government as to how/when business should spend their money) improve the situation.

late to the thread

Jul 4 2011 at 1:32pm

Two comments from the hiring manager side (technical).

@Troy: I’ve turned down PhDs and hired BA. for the same job (on a team with some PhD’s, some Master’s and some BA/S’s). The PhD isn’t a trump card, especially if it is being balanced against 5 years of industry experience and it is a non-research job. The very attitude that the undergraduate automatically could have nothing to offer that you couldn’t teach could be a turn off.

@CBBB Sounds like you got 4 “meh” results and the 5th guy (the boss?) finally pulled the plug. It is a wishy-washy excuse he gave, but sometimes that’s all you get. Not all dates work out.

CBBB

Jul 4 2011 at 1:51pm

I don’t agree that there has been all that extraordinary an amount of government spending. Sure there’s been tax-relief and loose monetary policy. But, as far as I remember, the Keynesian economists were saying even before the stimulus was implemented that it was going to be inadequacy and that tax breaks weren’t going to help much, no matter how big. They were always demanding the government spend more on direct job creation and financial support to the States and worry less about tax rates – but this never really happened.

So I agree that there might be some actual structural component but, in my experience (anecdotal as it is I have yet to see any data that really debunks this) there’s a large cyclical component that was REALLY never properly addressed.

I maintain that a non-trivial part of the unemployed at people who would partial or near matches for available positions but can’t find work because employers have the luxury to wait until an exact-match comes along. More money, as long as it’s targeted at actual job creation this time, would absolutely help the situation – I have yet to see a reason why it wouldn’t.

CBBB

Jul 4 2011 at 1:55pm

@late to the thread

Maybe it was 4 “meh” – I don’t see how though since I found the interview questions pretty straightforward, but the company did pay to have me fly to their offices and pay for my stay – seems like a bit of an investment for a 4 “meh” interviews. My personal feeling is that I killed the technical interview – and the reality is a lot of companies are looking for the perfect candidate: technical skills AND the “right” personality.

RZ0

Jul 4 2011 at 7:59pm

Still waiting for someone – anyone – to point out to me the high areas of growth that workers should be flocking to.

I’ve heard health care, but my next-door neighbor is an administrator at a hospital that is downsizing, my brother in law is PR at a different hospital that is laying off, and my sister in law, who sells raw materials to pharmaceuticals, is quaking in her boots over her job.

RZ0

Jul 4 2011 at 8:02pm

Just to add, per earlier comments, that I know programmers who have been laid off, too, and have struggled to find work.

To say there’s a shortage of people with substantial experience who will work for peanuts is not to supply evidence of structural unemployment.

Comments are closed.