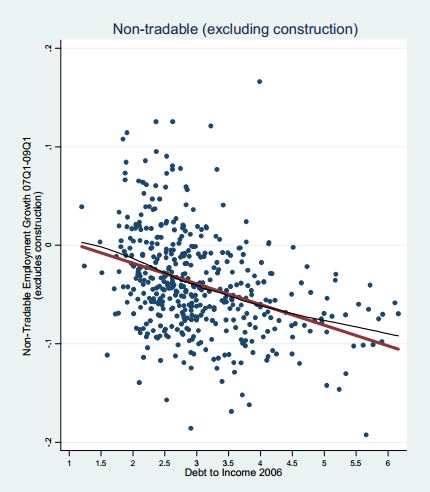

Mian and Sufi (who showed that cash for clunkers failed) have written a batch of papers on leverage and the financial crisis. This one may be my favorite: They check to see whether counties with the highest leverage before the crisis (measured by the ratio of household debt to income) lost the most retail and restaurant jobs. Key quote:

[A] one standard deviation increase in the 2006 debt to income ratio of a county is associated with a 3 percentage point drop in [retail and restaurant] employment during this [2007-2009] time period…

So high-borrowing counties were high-layoff counties.

But there’s more to it than that: High-leverage counties lost a lot of retail and restaurant jobs (which they label “non-tradable”), but they didn’t lose an especially high number of jobs making tradable goods. So the worsening balance sheets hurt the demand for local goods, but didn’t noticeably hurt the supply of exported goods. Each dot is a county:

[W]e show that the leverage ratio of a county is a far more powerful predictor of total employment losses than either the growth in construction employment during the housing boom or the construction share of the labor force as of 2007.

READER COMMENTS

Nickolaus

Sep 17 2012 at 12:51pm

That’s quite a trend line. The error bars on that thing are gonna be huge!

Garett Jones

Sep 17 2012 at 3:07pm

The t-stat is about -7, so the error bands are tiny.

That’s what 450 observations–every U.S. county with > 50,000 people–will get you…

Charlie

Sep 17 2012 at 10:02pm

You accidentally posted Bernanke and Gertler (1989) instead of Mian and Sufi, but it gives me a chance to try one more time to get people talking about it.

In the conclusion:

“We have not discussed policy implications…Issues of efficiency and policy are taken up in our 1987 paper. In particular the paper discusses whether a policy of “debtor bailouts” may be desirable when borrower net worth is low.”

If you chase that rabbit hole to the 1987 paper <http://www.jstor.org.ezproxy.lib.uconn.edu/stable/10.2307/2937820?origin=api>

“Thus far, we have focused on the benefits of transfer policies; our model suggests that they can be used to improve borrower creditworthiness and thus reduce the adverse effects of financial

fragility. However, our model, not being dynamic, does not incorporate every economist’s first and most strongly held objection to bailouts: the moral hazard issue. The problem is, of course, that expectations of being bailed out in the future will lead to excessive risk-taking and other inefficient behavior by borrowers. One response to this is to recommend that bailouts be used only in response to large aggregate or systemic shocks, over which individual borrowers could have no control; individual institutions

that have made bad decisions should not be bailed out. In principle, this approach should avoid the moral hazard problem.”

I feel like there’s some interesting points in these papers about Bernanke’s bailout thought process that were never blogged about.

Various

Sep 18 2012 at 1:16am

Garett,

Thanks for another great post. You are covering some good ground. Wanted to let you know that I have been a long-time reader of Econlog and you are posting some fabulous stuff. I haven’t commented on the substance of your posts because they are well thought out, and thus I have nothing to ad. Justed wanted to pass along my 2 cents and welcome you.

Charlie

Sep 19 2012 at 2:16am

I fail again. Still the click through link on batch is the wrong paper. See above.

Karl

Sep 20 2012 at 5:07am

So the bottom line is that counties that need to deleverage and pay down debt have a aggregate demand problem. That makes a lot of sense and certainly passes the common sense test.

It also points to the obvious conclusion that policy should be geared toward keeping individuals from leveraging up beyond their means (weakened lending standards and fraud obviously had a big role in exacerbating these problems) and any recovery plan should be geared around helping deleveraging happen more quickly. I don’t think the government has done enough to push those two things, but deleveraging has slowly been taking place.

Comments are closed.