A few weeks ago I criticized a Robert Shiller claim that economic theory tells us that low interest rates should lead to more investment. That’s an EC101 level error, reasoning from a price change. Unfortunately, I see this all the time.

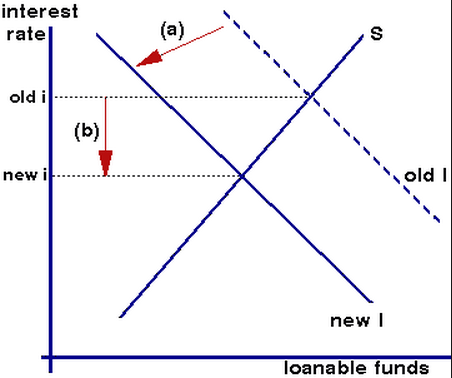

Many commenters defend fiscal stimulus by claiming that when interest rates are very low more projects are feasible using NPV criteria. But as the following graph illustrates, that’s just not so:

In this case, the investment schedule shifted to the left, and the equilibrium quantity of investment fell as the interest rate fell. The mistake is assuming that the factor that caused a fall in the market interest rate did not also cause a fall in the NPV of many projects.

A recent Quartz article provides a good example of this fallacy:

Summers has proposed “secular stagnation” (pdf) as the explanation for economic weakness since the 2008 recession: Private investment is falling because firms see slow population growth and innovation as a sign that future returns aren’t likely, creating a self-fulfilling prophecy of slow growth. His answer is more government investment–to jump-start demand, and the economy.

Now of course there might be a case for more public investment. But if so, it would not be because the economy is depressed and interest rates are low. If a depressed economy is caused by slow NGDP growth the answer is clearly a more expansionary monetary policy. For instance, the Fed could cut its interest rate target for 2016. If NGDP is right on target and interest rates are still unusually low, there might be a justification for more public investment, but only if the low rates were caused by a rightward shift in the supply of saving. But the factors in the Quartz article suggest exactly the opposite!

Most public investment is designed to accommodate population growth. This includes roads, sewers, public transport, schools, airports, etc. Much of this should be turned over to the private sector. But if the government insists on doing all this public investment then it needs to make sure that projects meet strict cost/benefit tests. When there’s a population growth slowdown then far fewer projects will meet that criterion.

I’m not saying that the slowdown in population growth is the only factor causing low interest rates. They partly reflect the hangover effects from the recent recession. But circumstantial evidence suggests that slower population growth plays some role. Japan has the slowest rate of population growth, and was the first country hit by the ultra-low real interest rates. Australia has the fastest population growth of the major developed economies, and in recent decades has had real interest rates that were somewhat higher than other developed countries.

When interest rates are low due to slow population growth the correct response may well be more consumption. Does your intuition tell you that this answer is wrong? If so, it may be because almost all governments currently have policies that are massively anti-saving/investment, and pro-consumption. The proper solution is to address the root cause of this investment deficiency—the high taxes on deferred consumption, restrictive urban land use rules, immigration restrictions, etc.

READER COMMENTS

Jacob H.

Apr 8 2015 at 1:53pm

Isn’t the argument that the low interest rates are due to an increase in (foreign) loanable funds that is unrelated to the NPV of US investments? Undoubtedly the investment schedule shifted left in 2008-2009, but it’s not clear that that is what is causing low interest rates today.

foosion

Apr 8 2015 at 2:36pm

Low interest rates and excess capacity lower the cost of projects.

For example, many believe we need better physical infrastructure and a better educated population. Is it better to make the investment when the cost of building, repair, etc. is low or the cost is higher?

Even with a declining population, it’s helpful to have infrastructure in good repair. It may even increase growth.

Nick

Apr 8 2015 at 2:44pm

If the appropriate infrastructure discount rate is lower due to low interest rates derivative of slow population growth, wouldn’t the expected returns in the numerator be lower for the same reason? Slow population growth, etc should yield lower expected returns over the lifetime of the asset and offset any decrease in the denominator. When interests rates are lower due to a shift in savings, the NPV calculus would capture the difference.

Doubtful that expected returns analysis by state governments would be that exact though.

MikeP

Apr 8 2015 at 2:46pm

Low interest rates and excess capacity lower the cost of projects.

Indeed they do …which is why it is bad policy to take resources away from private investment in private projects, which have more capable and interested decision makers, to invest them in public works just because interest rates are low.

The point being made in this post is that public investment must be justified based on the value of that investment, not merely because interest rates are low.

foosion

Apr 8 2015 at 3:58pm

bad policy to take resources away from private investment

A feature of low rates and excess capacity is that you’re not taking resources away from private investments.

public investment must be justified based on the value of that investment

There are things I’d hope it would be obvious we should be doing, like maintaining heavily used roads, bridges, etc.

Scott Sumner

Apr 8 2015 at 5:37pm

Jacob, I’m not sure what you mean by “the argument.” I was responding to the specific argument in the post I quoted, which mentioned falling population growth. Undoubtedly there are many factors.

foosion, It’s not an either or situation. There is always going to be some infrastructure investment. But when population growth slows then the optimal amount of infrastructure investment usually falls. Another problem is that building things like subways lines costs 5 to 7 times more in the US than Europe. So it’s really hard to find subway projects that work on a cost /benefit basis.

Everyone, Look and the graph, and recall that this graph shows less equilibrium investment, even taking into account the fact that lower interest rates make any given project look better.

ThomasH

Apr 8 2015 at 7:39pm

“Many commenters defend fiscal stimulus by claiming that when interest rates are very low”

“The mistake is assuming that the factor that caused a fall in the market interest rate did not also cause a fall in the NPV of many projects.”

It IS a mistake in general. But 2008 – 2015 have not been “in general.”

If one believes that ngdp gdp growth was knocked off course by – chose one or more: 1) too tight money, 2) a financial crisis that gummed up financial intermediation, 3) rise in risk premia then these factors did not suddenly and pari paus reduce the returns from fixing potholes, repairing roads and bridges, building new transit systems, surveying for Earth orbit crossing asteroids, investing in CO2 emission reducing technologies, public and publicly-subsidized R&D, etc.

Therefore the fall in interest rates as the Fed moved ST rates to the ZLB and pushed LT rates down with QE SHOULD lead to greater public investments and certainly does not lead to a presumption that we needed to close libraries and lay off teachers. So, yes, the kind of recession we’ve had [sorry, but the graph of real gdp in 2008 just does not look like a decline in the LFPR or a technological shift in the MP of capital] DOES mean that an optimizing government (one that invests in positive NPV projects) would increase its deficit-financed investments. If you want to call this “fiscal stimulus” and NK models get to this (unfortunately uncommon) common-sense result, bully for them.

ThomasH

Apr 8 2015 at 8:10pm

While Scot make a valid theoretical point about public investment (there are circumstances in which a fall in the government’s borrowing rate would not imply an increase in investment) this is where the real world discussion is:

http://www.slate.com/blogs/the_slatest/2015/04/08/the_u_s_government_has_cut_funding_to_a_key_hurricane_research_program_and.html

Duncan Earley

Apr 9 2015 at 12:34am

I think this is one of my fav Scott posts 😉

I still have a question of course…

I understand why “restrictive urban land use rules” and “immigration restrictions” would hurt growth. Indeed I think these, aside from population growth, are the main things that could increase growth.

However how does “the high taxes on deferred consumption” hurt growth? If you reduce those taxes it isn’t going to help investments if there are no feasible (NPV) investments?

Scott Sumner

Apr 9 2015 at 9:42am

Thomas, The article claimed that slowing population growth was a factor, and I agree. You still want to fill potholes, but you don’t want to build new roads.

Duncan, Lower taxes on investment income (i.e. future consumption) would raise the after-tax NPV of potential investment projects.

Shayne Cook

Apr 9 2015 at 11:45am

Good post, Scott.

I think even more myths abound, and some fact checks might help…

On Larry Summers (evidently relying on his “intuition” and biases, rather than data):

He is dead wrong. In fact, BEA data indicates private non-residential Investment has been steadily increasing as a percent of NGDP since its low in 2010 – 9.23% of GDP in 2010, 12.25% of GDP in 2013, and 12.69% of GDP in 2014. As opposed to an average of 11.56% of GDP for the period of 1980 to 2000.

[Source: bea.gov, Table 1.1.5]

Sanity check of BEA data: The vast majority of new jobs created since 2009 – reducing the unemployment rate – have been private sector jobs.

One other item that becomes clear from the NGDP data is that elevated Government “Investment” didn’t occur during the 2009-2014 period, nor was it directly “stimulus”.

Note GDP/NGDP reflects only purchases of newly produced goods/services. If you check the [G]overnment share of NGDP in the same BEA data set, you’ll note that Government spending didn’t rise significantly in any of those years. The average [G] purchase component was 19.85% of GDP from 2009 through 2014 – versus a 1980 to 2000 average of 19.61%

The majority of elevated Government spending for “stimulus” during the 2009 through 2014 period was for re-distribution, NOT purchases of new goods/services (as would be indicated in NGDP data), and NOT for “Investment”.

It’s reasonable to assume the elevated Government re-distribution spending did help support and actually elevate [C]onsumption spending at about 70% of NGDP during the 2009 through 2014 period. (I, personally believe that it is intensely un-clever to fund current consumption with massive debt, but that’s just me I suppose.) But it is also likely (and provable) that much of that elevated Government re-distribution spending was diverted to retirement/reduction of private debt levels. See Fed data on private debt level trends for the period. Kevin Erdmann has also presented some interesting/supporting private debt level/trend data on his site.

A “Keynesian” note here …

The conventional wisdom “Keynesian” recession remedy is to elevate [G]overnment spending (via debt, if required) during a recession, ostensibly to offset reductions in private [C]onsumption and/or [I]nvestment spending that caused the recession in the first place – thereby keeping overall GDP “pretty”. The highly elevated, debt financed, [G]overnment spending during the 2009 through 2014 was NOT “Keynesian” in that respect. There were no elevated levels of [G]overnment spending on the purchase of new goods/services.

Instead, the net effect of the highly elevated, debt financed [G]overnment (allegedly “Keyensian” stimulus) spending was to temporarily prop up [C]onsumption, AND convert a massive amount of formerly private debt into public debt.

So, it seems Larry Summers (and others) has it wrong now, and has had it basically wrong all along.

On the general effects of interest rates on Investment …

[I]nvestment-Non-Residential (business investment):

Conventional wisdom would indicate that low interest rates (borrowing costs) would tend to stimulate new increased business investment spending. Two things tend to confound that conventional wisdom (in addition to the “mistake” Scott identifies here.)

1.) Business will prefer to finance start-up and/or expansion via equity rather than debt – at any interest rate – due to debt service costs being accounted for as “fixed cost” in ongoing operations. And “fixed cost” reduction is always a major concern/goal/mantra in business. Even if a firm does finance an expansion/start-up via debt, its management will attempt, at the earliest possibility, to retire that debt with equity financing – again, completely irrespective of interest rate – in order to reduce “fixed costs” of operations.

(The benefit of business tax-deductibility of debt interest does NOT offset the negative effects of elevated “fixed costs” of operations, as conventional wisdom might indicate. Especially in a low interest rate environment.)

2.) Everyone knows current interest rates are low. Additionally, everyone knows they aren’t going to stay low. An increasingly prominent trend in business related lending/borrowing is variable rate debt – similar to that already applied in residential housing related debt.

And again, the business (non-residential fixed) [I]nvestment component of GDP returned to “normalcy” (long term trend) as a percent of GDP over two years ago. And in fact was above trend in 2013 and 2014.

[I]nvestment – Residential (housing investment):

Again, conventional wisdom (Shiller) would dictate low interest rates to inspire elevated housing investment. Scott pretty much “nailed it” why Shiller and conventional wisdom might not be reliable in this case …

Referring again to the BEA NGDP data, current [I]nvestment-Residential remains low (3.21% of GDP in 2014 versus an average of 4.25% during 1980-2000, and 5.51% of GDP during the 200-2006 “housing boom” period.)

Keep in mind that the GDP data reflects new home construction/sales during those periods, NOT pre-existing home sales.

But there are other artifacts of “housing investment” that also tend to confound conventional wisdom in this regard.

1.) The first-order effect of low interest rates on housing is to elevate home prices. If you have ever purchased a home, you’ll know that the first question that is asked of you is, “What is your income?” It is the answer to that question that determines “how much house you can buy”, by virtue of how much debt service you can “afford” – debt service being interest PLUS principle. If the interest rate component drops, the principle component elevates.

High and/or elevating housing prices might inspire elevated new home construction (reflected in GDP), but only as a secondary effect of low interest rates. But simultaneously, high and/or elevating home prices also reduce the number of private buyers able to enter the market.

2.) The “housing bubble” period from 2000-2006 was an interesting period. For private owners, homes have an “Investment” value certainly. But they also have an “Intrinsic” value. Let’s assume that, early in the “housing bubble” period, the elevating prices and new home construction trend was generally “good” debt-financed investment for private owners, generally speaking. It certainly also helped make the NGDP numbers look “pretty” during that period.

But at some point between 2000-2006 (probably around 2004), that debt-financed “good” investment turned into debt-financed mal-investment. Bad joo-joo, as they say. But all during that period, and well into 2008 frankly, NGDP still looked “pretty”, primarily because the [I]nvestment-Residential component of GDP still looked robust and “pretty”. Furthermore, if one considers the also elevated levels of [C]onsumption component of GDP, well into 2008 and beyond, and that at least some of that elevated (and “pretty”, in NGDP terms) [C]onsumption spending was probably fueled by debt, based on the mal-investment fueled (apparent) home equity.

It seems obvious that debt-financed Mal-Investment has just as much capacity to make NGDP (and all the relevant sub-components of NGDP) look “pretty” as real honest-to-gosh Investment does. But it really isn’t Investment at all. It’s just debt. Contrary to the assumptions of folks like Larry Summers, and their ilk, real honest-to-gosh Investments provide a pay-back. You know, in order to provide the means to actually retire the debt.

Conversely, taking on massive public debt for re-distribution, in order to make or keep current [C]onsumption or even total current NGDP looking “pretty”, is the functional equivalent of using your Home Equity Line of Credit to finance a month-long cowboy drunk. Once that party is over, all your left with is the debt – and no new way of paying it off.

My “story” differs from that of Larry Summers, and others. But at least I have data to back my “story”. And someone should probably explain to Summers and others what an “Investment” actually is.

(Apologies for the length of this comment.)

perfectlyGoodInk

Apr 11 2015 at 7:31am

I think the issue is not that he’s reasoning from a price change, but that he’s reasoning from a price level. He’s talking about low interest rates, not lower interests rates. So it sounds looking purely at the Investment curve and reasoning that a low interest rate means you must be on the lower right side of the curve.

The whole loanable funds model is suspect anyway. I recall that it’s been empirically shown that consumers consumption/saving choice is not significantly affected by the interest rate. Most people spend what they want, and save if there happens to be money left over. They will even use very high-interest rate credit cards to achieve the desired spending level. If consumers really cared about interest rates, they would never use credit cards.

Scott Sumner

Apr 11 2015 at 2:01pm

Shayne, Yes, Summers overestimates the ability of governments to invest wisely.

PerfectlyGoodInk, You said:

“The whole loanable funds model is suspect anyway. I recall that it’s been empirically shown that consumers consumption/saving choice is not significantly affected by the interest rate.”

Keep in mind that the loanable funds model does not predict that consumer will save more at higher interest rates. It depends why rates change.

perfectlyGoodInk

Apr 13 2015 at 5:44pm

Why does the Savings curve slope upwards then?

Comments are closed.