Imagine living in a country where the top 30% of the population had roughly 25 times as much wealth per person as the bottom 30% of the population. That seems pretty unequal, doesn’t it? Now suppose the same statistics applied, but every person at any given age had exactly the same wealth. All 18 year olds had the same wealth as other members of their cohort, as did all 60 year olds. But 18 year olds had much less wealth than 60 year olds. Now how would you feel about the data? Does that sort of society seem highly unequal? Not to me, indeed in a sense there’d be no inequality at all; each person would experience the exact same wealth trajectory over the course of their life.

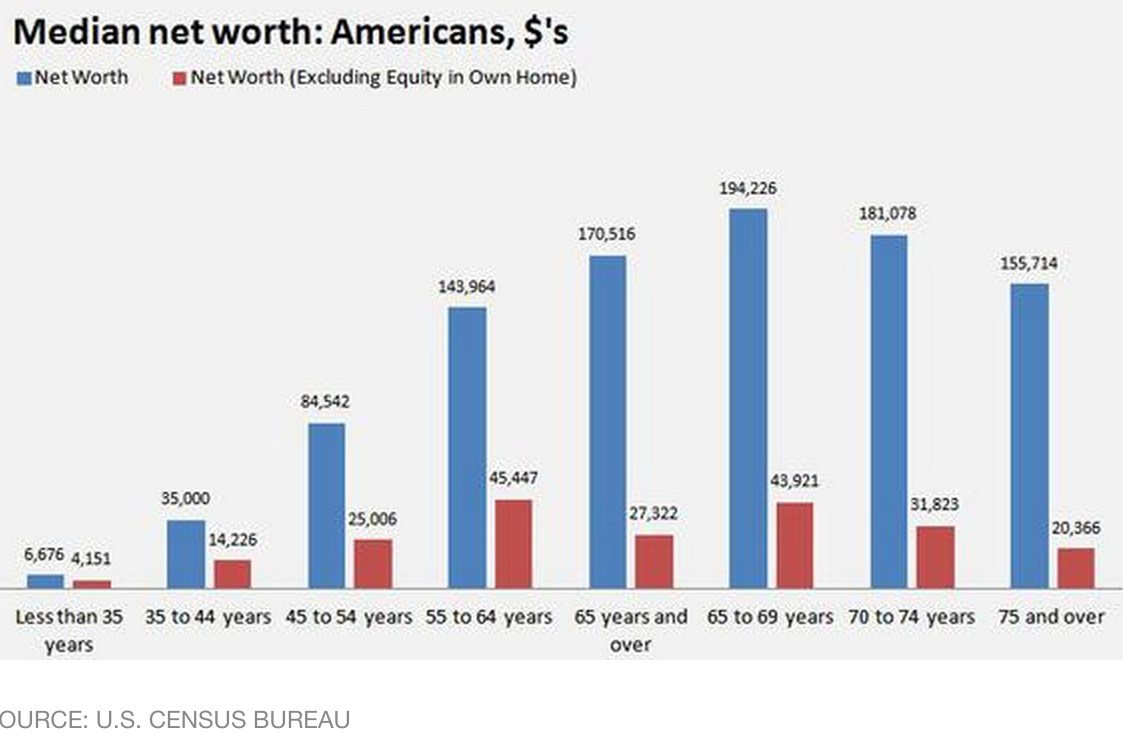

Of course we don’t live in that sort of society, there are large differences in wealth at any given age. But even if we did have that sort of equality, the aggregate wealth data would look shockingly unequal. Here’s some Census data for the US, showing that the median person in the over 55 age group holds about 25 times as much wealth as in the 18 to 35 group:

So could we solve this measurement problem by getting wealth inequality data for each age cohort? Not even close, because wealth is a poor measure of economic well-being. Suppose you had two people who each earned $100,000/year in wage income. Over the course of their life they both eventually spent all of their wealth on consumption goods. Both ended up with an identical level of total consumption, in present value terms. But one person spent all his money as it was earned, and then relied on Social Security, while the other saved 1/2 of his wage income, spending much more in his later years. By age 65 the thrifty guy might have several million dollars in wealth, while the other guy had almost nothing, even though (by assumption) they were equally well off in economic terms, they simply had different preferences as to when to spend their money.

I was recently at a NGDP conference in West Virginia, and noticed this in the local paper’s advice column:

Dear Dave,

My wife and I have just started getting on track with our money. We have $2,000 in savings, and the only debt we have is our house and two cars. I work in the oil and gas industry and make about $180,000 a year, but things are pretty volatile right now. We’re upside down on both vehicles, and we owe $39,000 on one and about $48,000 on the other. Under the circumstances, should we go ahead and build a fully funded emergency fund or work on paying off the cars?

KendallDear Kendall,

Are you kidding me? Sell the cars, dude!You need to go to Kelly Blue Book’s website right now, and find out what your cars are really worth. Then, put them on the market as a private sale. You’ll get thousands more selling them that way than you will at a dealership. You’ll have to talk to a local credit union or bank for a small loan to cover the difference, plus a little bit more so you guys can get a couple of little beaters to drive for a while.

I’m going to go out on a limb and guess there aren’t very many similar letters in China. Like the advice columnist “Dave”, I have a temperament that makes it easy to save. But as a libertarian I favor allowing people like Kendall to spend their money when and how they wish. The only qualification is that I think people should be forced to save enough to cover the things that society would otherwise have to pay (basic retirement, medical, etc.) If we believe that people should be free to choose when to spend their wealth, we will end up with far more wealth inequality than if we try to force everyone to consume the “right amount” of each year’s income. But I don’t see how that sort of wealth inequality could be considered a problem.

Inevitably some will misconstrue what I am saying here. Just to be clear, even accounting for all the factors I mentioned (age, saving preferences, etc) there is still lots more inequality due to big differences in lifetime earnings (or inherited wealth.) So this post is not trying to suggest that inequality is not a problem. Rather I’m suggesting that if inequality is a problem, we would not be able to know that from the wealth inequality data that is presented in the media. And that’s because even if wealth inequality were not a problem at all, the actual inequality of wealth would look shocking large, with 100 to 1 disparities easily accounted for by nothing more than differences in age and saving propensities. The only data that truly gets at the inequality question is consumption inequality, which is very rarely discussed in the media.

READER COMMENTS

Bostonian

May 18 2015 at 9:57am

There is inequality of income and wealth and also inequality of leisure, and leisure comes at the expense of income and wealth. We should not adopt the left’s rhetoric of “inequality”, which ignores such trade-offs.

I earn well, so my wife’s working as a physician contributes to income and wealth inequality. It also leads to our having little free time, since we have three children as well as two full-time jobs.

Scott Sumner

May 18 2015 at 10:29am

Bostonian, Good point.

Sieben

May 18 2015 at 12:31pm

Why is it even valid to measure wealth in terms of net worth/income/whatever? I know several nominally rich people who can’t take care of themselves. They can’t feed themselves properly, groom or maintain pleasant hygiene (despite expensive cosmetic products), manage their relationships like an adult, etc.

I would feel poor if I lacked all of those skills. Money is just one aspect of wealth. Wealth is control and mastery over your life. There’s nothing to envy from most people regardless of how much money they have.

KLO

May 18 2015 at 12:43pm

I always wonder if these questions to advice columnists are real. Whether it is weight loss, finances, or relationships, the problem people have is rarely about knowing the “right answers” to the major questions. The real problem is execution in the face of constant temptations to stray.

Advice columnists present themselves as experts on their subject, but what they really are is expert motivators. If this spendthrift is real, I suppose he needs to be told that continuing to pay off debt slowly on expensive, rapidly depreciating assets will hurt him financially not because he doesn’t know this, but rather because he does know this and is having trouble acting on this knowledge.

For libertarians, the difficulty presented by this scenario is not so much the spendthrift prefers to spend his money now rather than save in spite of the consequences, but that many people feel quite torn between buying things that are relentlessly marketed to them in subtle and overt ways and saving money. If China is different (I am not sure it is), it is not because individual Chinese people are less prone to temptation or have starkly different time preferences. More likely, it is because external factors encourage saving and investment over consumption.

For individuals to successfully pursue what it is they value most, they must have an environment that supports this. Legally imposed constraints on action are but a very small part of the puzzle.

Philo

May 18 2015 at 2:12pm

“So this post is not trying to suggest that inequality is not a problem.” I think this post *is* arguing, quite convincingly, that inequality of *this year’s income* and inequality of *present wealth* are *not* problems, that if there is a “problem of inequality” it must concern inequality *of something else*. And, as you suggest, by far the most plausible candidate is *lifetime consumption*. But on reflection this does not seem to be quite what the inequality-fear-mongers should offer us. Suppose my twin voluntarily consumes all his income, while I save a lot of my similar income so as to give it to my children, or to charity, or to some political cause. He ends up consuming much more than I, but where is the “problem”? Or suppose that, though he and I have similar incomes and propensities to consume, I am killed (accident, disease, whatever) in my youth, while he lives to old age. My early death is regrettable, but I do not see that our *inequality of lifetime consumption* is itself a *problem*.

Those who decry “inequality” owe it to us to specify in *exactly what* respect we ought to be made equal. I doubt that they can find a plausible candidate.

(It would also be nice to learn *exactly who* “we” are. Human beings? But that would be *speciesism*! [By the way, I am serious: I think speciesism is a philosophical error.] And even if we accept that “we” = human beings, why are fetuses to be excluded? And where do past and future human beings figure in?)

I see inequality-phobia as completely unfounded.

Philo

May 18 2015 at 2:26pm

You think that people should be forced to save enough to cover the things that society [by which you seem to mean *the government*] would otherwise have to pay for, including “basic retirement, medical, etc.” But obviously the government/society does not have to pay for these things, since over most of human history (not to mention pre-history) *it has not done so* (and in some of the poorer regions of the world, even today, it *does not do so*).

Suppose I promised to pay your medical expenses, and then I forced you to give up smoking, take exercise, etc., because otherwise your medical expenses would burden me unduly. Would my use of force on you be justified?

True, in the U.S. and a number of other countries at present the government is *determined* to pay for certain such items: that is political reality. But I object to your saying that it *has to* do so.

Floccina

May 18 2015 at 3:50pm

The one might have a wealth of good memories from his high spending. Some old people regret not saving more when they were younger and some, like may fathers mother, regret not having spent more when they were young and could enjoy it.

It is hard to say who lived better. How do you justify taxing one much higher that the other? There are many other examples like that, one child enjoys his youth playing sports and not studying, another keeps his nose to the grindstone. Should the latter subsidize the former? Should we push the former to study more or the latter less? Not easy to answer.

Scott Sumner

May 18 2015 at 3:56pm

Sieben, I completely agree.

Philo, Yes, I should have been more specific. I meant that economic inequality (i.e. consumption) may be a problem, but you are right, I don’t think income or wealth inequality are problems.

Floccina, I agree, it’s hard to justify taxing one higher than the other.

JMK

May 18 2015 at 8:38pm

I don’t know where the idea of “forcing” anyone to do anything comes into play here. The letter writer sought advice from someone whose stance on the issue is well known. It would stand to reason that he voluntarily wanted to know how Dave would do things, thus is not forced into a particular behavior. The letter writer also retains the option to follow this advice or do something else. He is not “forced” in any of his decisions.

Now that we have that out of the way, I’m going to need some help understanding why “inequality” is a problem. We understand that individuals are inherently unequal — different physical attributes, different mental abilities, different desires. We also understand that a society will contain a range of each ability and outcome. There can’t be a “good” outcome if there weren’t a “bad” outcome.

Knowing that individuals at all income levels consume, what are the specific concerns in regards to “inequality”? What is a desirable amount of inequality to have?

Scott Sumner

May 18 2015 at 10:11pm

Philo, When I said “have to pay” I meant “choose to pay,” as in most people feel we have a moral obligation to do so. Whether we actually have the moral obligation is of course an entirely different question.

As far as the question of when force is justified, I’m a libertarian utilitarian. That is, I’m someone that believes society is happiest when the government uses a very small amount of force, much less than in any actual society that I am aware of. I don’t favor banning cigarettes. But there are close calls, such as seatbelt laws.

JMK, You said:

“I don’t know where the idea of “forcing” anyone to do anything comes into play here.”

That was my straw man.

You asked:

“What is a desirable amount of inequality to have?”

That’s a very difficult question, which becomes far more difficult as you move from the national to the international arena.

John T. Kennedy

May 18 2015 at 11:51pm

” The only qualification is that I think people should be forced to save enough to cover the things that society would otherwise have to pay (basic retirement, medical, etc.)”

But of course there is no reason society would otherwise have to pay for such things.

And consider an able bodied adult who lived off his parents without working. Would you favor forcing him to work to earn enough to save enough to cover those costs you claim society would otherwise have to pay?

Larry

May 19 2015 at 12:56am

* Inequality has increased greatly in recent decades. That’s more interesting than absolute inequality. (Why was it less before, if this is normal?)

* The savings example neglects the role of inheritance (not to mention that lots more than “assets” get passed down.)

* I’ve never been able to get a liberal to tell me what a “fair” distribution of income or wealth would be or how you’d come up with such a thing. The best I get is “more equal”, although that was the demand back in those more equal days, too….

* The crash has disrupted the wealth/income trajectory of millenials compared to that of prior generations. Millenials may be condemned to stay (relatively) behind their forebears. If we don’t fix the macro economy, not to mention education (finance, etc.) that may be true of the generation after them as well.

* Love to see an age-adjusted inequality trend and one that excludes millenials, for the above reasons.

maynardGkeynes

May 19 2015 at 1:54am

I fail to see how this post is at germane, let alone instructive, to the actual debate about inequality going on today. That fact that a Bill Gates has enough money to buy up every private residence in Boston, with enough spare change to buy up Bentley Univ and turn it into his private airport, is what’s at issue. That fact that he actually does not choose to “consume” his wealth in that particular way strikes me as largely irrelevant to the present 99.90% debate. Nor does anyone I know view Beyonce having her baby in the private wing of a hospital as a threat to our democracy, wasteful and silly though it may seem. It’s simply not debate about consumption at this fundamental level. Perhaps I misunderstand your point? (very possible).

john hare

May 19 2015 at 4:32am

For those interested in the advice by Dave, look for “Dave Ramsey” on your local radio. He’s on 500+ stations in this country and on the web. Focus is on getting out of debt and never borrowing money again for any reason. “Debt is dumb, cash is king, and the paid off home mortgage has taken the place of the BMW as the status symbol of choice”

Interesting show and often informative, but sometimes I disconnect from the advice. One of them I remember is “Don’t take out a $20,000.00 school loan to get a certification that nets an automatic $9,000.00 a year raise at your current job. Save up the money and pay cash or work your way through it, but don’t borrow.” To me, a 2.5 year payoff is an excellent ROI.

Bostonian

May 19 2015 at 8:07am

@maynardGkeynes

‘That fact that he actually does not choose to “consume” his wealth in that particular way strikes me as largely irrelevant to the present 99.90% debate.’

Why? The examples of multibillionaires like Gates and Buffett consuming only a small part of their wealth and donating/investing most of it is an argument against taxing it away. I trust Gates and Buffett to do more good with their money than politicians would.

maynardGkeynes

May 19 2015 at 9:53am

@Bostonian — for every Buffet or Gates, there’s 10 Koch or [your liberal plutocrat here]. However, the fact that the very wealthy actually don’t spend that much may be an AD problem, (although I think the Professor does not see that as an issue.) Also, I’m not so sure how much good Bill Gates has actually done — I have the impression that much of the money has not had great results. FDR did a lot of lasting good. The bridges, parks, and highways of the WPA are marvelous (and under his successors, the interstate highway system, and the Apollo program), are a reminder if what great things government can do.

Mike W

May 19 2015 at 5:13pm

This kind of debate…i.e., the measurement of inequality….seems like the academic version of looking for your lost car keys under a street light. It does not address the real question, does domestic inequality…of consumption in the case of SS…justify government action? In the mass media…and in the academic measurement debates…the inequality issue is merely political rhetoric, but in academia there must surely be some who argue that it is a problem…what are the pros and cons?

myb6

May 19 2015 at 6:49pm

Still ignoring that “only data that truly gets at the inequality question is consumption inequality” is just a statement of Scott’s personal values. Other people might also value things like security, power, status, self-actualization, influence, etc etc which need not fall under our “consumption” statistics.

Let’s say Scott and I are living in a micro-state under a benevolent state ruled by Fnargl. Now let’s say that, under Fnargl’s laws, I have property rights to the only water-source. I like Scott, split the water evenly, and on 7/4/1826 (Fnargl Year) we both die having consumed the exact same amount of water. However, Scott lived his entire Fnargl-life under the apprehension that I might arbitrarily decide to let him die of thirst. Equality? Now assume I’m a jerk and used my property rights to influence Scott’s behavior. Still equality?

The metrics people are using in the inequality conversation aren’t great, let alone perfect, but consumption inequality is even less useful. The lack of engagement with this criticism, despite repeated opportunities, reflects poorly on Scott’s thought-process.

Scott Sumner

May 19 2015 at 9:16pm

John, You asked:

“And consider an able bodied adult who lived off his parents without working. Would you favor forcing him to work to earn enough to save enough to cover those costs you claim society would otherwise have to pay?”

No, that’s between him and his parents. It’s up to them to decide if they want to support their son.

Maynard, My point is that what you call the “actual debate” is in fact the wrong debate. We should be debating consumption inequality, not wealth inequality. My second point is that the wealth inequality data doesn’t really tell us what many people assume it tells us.

Regarding Gates, I’m very sympathetic to the claim that our intellectual property laws are far too restrictive, and that this provides excessive monopoly power and economic rents. But that’s not the issue I was discussing here.

Regarding who spends money more wisely, my impression is that Gates donates quite a bit to foreign causes, especially programs helping the poor in developing countries. In contrast the US foreign aid tends to go to corrupt dictators, and/or military weapons for Pakistan, Egypt, Israel, etc. Is that impression correct?

You’ll have to explain to me how the Apollo program was a wise use of money. Couldn’t the same science have been done with an unmanned probe for less than 1/10th the cost?

The reason we don’t build infrastructure like FDR used to is that government regulations have made it far too costly today.

Jim Glass

May 19 2015 at 11:15pm

Back in the olden days when usenet’s sci.econ was a vibrant (that’s one word for it) discussion forum, I posted a numerical example illustrating how a termite colony, in which every termite was exactly the same as all the others, would display ever-rising inequality between rich and poor termites as time passed, by the metrics used in popular discussion.

Start with a colony in which all termites are identical, produce the same amount, and receive income in the amount they produce. So the colony’s income is equally divided among all. (Forget the Queen, she’s been toppled in a revolution.)

Now an evolutionary advance lets termites learn to become more productive as they age, say by 3% a year (or whatever time period). All termites live the same lifetime, say 38 years — long- lived but conveniently giving the oldest termite exactly 3x the income of the youngest.

This is unambiguously good, an improvement to all termites, as it gives the colony double the income it formally had, and income is still split exactly equally among each generational cohort — so over a lifetime each termite still has exactly the same income as every other.

But, ooops, “inequality” has set in among the termites, as the “richest 2.6%” have double the average income of the bottom 60%.

Now, another evolutionary advance happily occurs, letting termites gradually accumulate knowledge and learn to continually become even more productive. Say the original 3% increment between termite cohorts itself grows by another 2% per year (from 3% to 3.06% to 3.12%, etc.) while newly arrived first-generation minimally productive minimum-wage termites, having not learned anything yet, retain a root income of 1 unit, from which all other growth grows.

Again, this is unambiguously good. Now the termite colony grows ever richer forever, each generation of termites is richer than the one that preceded it, each generation splits its income evenly with perfectly equality, and each termite receives with perfect equality income exactly equal to what it produces. Who would not endorse *that* societal structure?

Yet, yikes, a horror of inequality results. The richest-level termites get richer forever and ever faster, pulling ever further up and away from the rest while the bottom remains forever rooted. As the richest termite income level gets richer at an accelerating rate, and the higher income-level layers get richer faster than the lower-levels, the bottom income-level layer of termites never experiences any gain at all. None, falling further and further behind.

When I posted this several people got very angry at me. Though it is just arithmetic, why get mad at arithmetic? Well, they were really angry that it implied that the method they were using to measure a problem that they were worried about exaggerated it to make it look worse than it was. But if you learned that the measure you were using of a problem you were worried about was biased to exaggerate it, so the problem wasn’t really as bad as you feared, shouldn’t that make you happy? Instead of angry? Well, that was usenet…

Jim Glass

May 19 2015 at 11:27pm

You’ll have to explain to me how the Apollo program was a wise use of money. Couldn’t the same science have been done with an unmanned probe for less than 1/10th the cost?

Sure, probably at 1/100th. Tang wasn’t that difficult to come up with.

But nobody ever pretended the Apollo program was about cost-efficient science.

The money spent to contain and defeat Communism was well worth it in my book, for all the mind-boggling “waste” one can point to in the process at so many junctures along the way.

J Mann

May 20 2015 at 9:54am

Jim, I always look forward to your posts, and occasionally stop by your old blog and sigh, but doesn’t your termite parable beg the question?*

You’re right that the high-growth high-“inequality” mound is preferable to the static growth completely equal mound, but that doesn’t answer the question of whether the termites should agree to transfer some wealth from the more productive bugs to the less productive bugs.

IMHO, to answer that question, you need to know:

1) How much would the transfer reduce overall productivity or growth?

2) How upsetting to the termites find the “inequality”, including varying utility functions, envy, social unrest, etc.?

3) What moral standard do you want to apply to the question? Utilitarianism? Hard property rights? Something else?

* Yes, none of this is relevant to your point that people got upset when you challenged their worldview, and you probably addressed it in the full post back in the day. 😉

Jim Glass

May 20 2015 at 6:56pm

J Mann wrote…

that doesn’t answer the question of whether the termites should agree to transfer some wealth from the more productive bugs to the less productive bugs.

If one thinks they should that’s a judgment that’s OK by me — but note that it is the younger generations of termites that are richer on a lifetime basis while it is the older that are richest at the moment, though poorest on a lifetime basis. So transferring from the richest to the poorest of the moment is in one real and meaningful sense actually transferring from the poorest to the richest – giving proponents of progressive termite taxation some technical issues to work out.

Steven Landsburg, IIRC, once proposed that we should drop a huge national debt on our young and hit them with youth-targeted taxes too, because on a lifetime basis today’s young will be the richest and most well-off of us all. And if one believes in progressive taxation currently one should believe in it inter-temporally too, across generations. It seemed an odd idea at the time, but as I get older it is beginning to grow on me.

And thank you for the kind words. I’ve been thinking recently of restarting the old blog. Reality has kinda beat up on me over the last few years but now seems to be easing up a bit, and I may get a chance to flee it. What better place to escape to?

Comments are closed.