I recently did a post arguing that it’s almost impossible to forecast recessions. Many commenters were surprised by my view, wondering why market monetarism doesn’t provide insights into where the economy is going. The simplest answer is that if the market rationally expected a recession, we’d already be in one, and hence it would be too late to predict the recession. In fact, it’s even worse. During the past three recessions, a consensus of economists didn’t even predict the recession until it was well underway, approximately six months into the recession. So not only do we have trouble predicting the future, we even have trouble predicting the present.

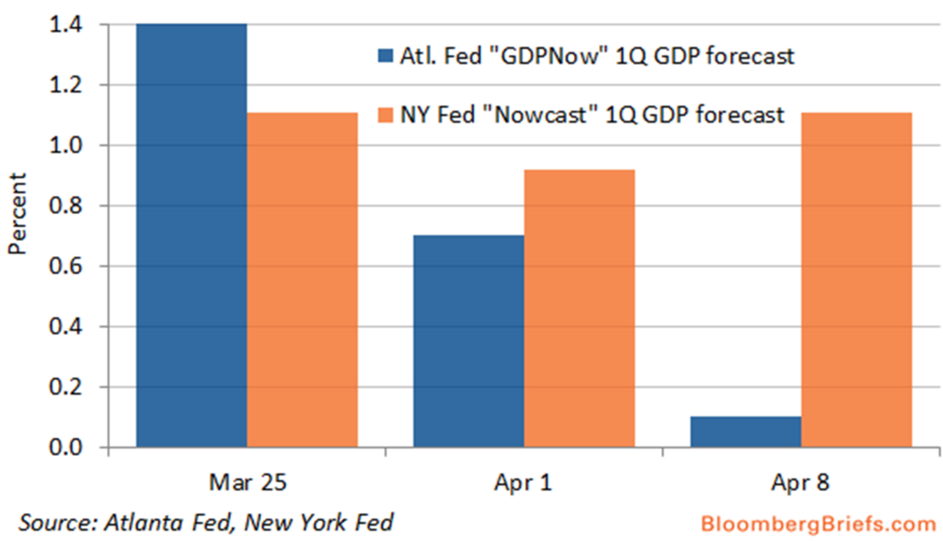

John Hall directed me to a very good Barry Ritholtz article on “nowcasting”, which is predicting the current position of the economy. The reason we need to predict that position, of course, is that there are data lags. Here’s a graph showing recent changes in two nowcasters, both at Federal Reserve banks:

Notice how dramatically the Atlanta 1st quarter prediction has declined in the past few weeks, even though we are already into the second quarter. Also notice the gap between the two nowcasters. Here’s Ritholtz:

The good news is, we now have two Fed bank nowcasting models. The competition between them might lead to more accurate forecasts.

The bad news is, given what appears to be a bullish and bearish modeling bias in the two, selective perception is likely to rule the day. Don’t like one nowcast? You can check the other one. In a free market, having more choices never hurt anyone. And if you’re a long-term investor, it almost doesn’t matter. If you’re a regular reader, you know where I’m coming from: Pay little or no attention to forecasts and stick to probabilities instead.

I see the development of nowcasting as good news. Not because they are useful (I don’t think they are) but rather because I see this as part of a process that will eventually lead to a highly useful entity—macroeconomic prediction markets—subsidized by the various Feds. Atlanta could run a RGDP prediction market, New York could run a NGDP prediction market, whereas St. Louis could run a PCE inflation prediction market. Competition between the various Federal Reserve banks to come up with the best forecast is a very healthy development. Eventually one of them will realize that prediction markets will allow them to beat their rivals.

I sometimes wonder if Keynes wished he could go to sleep and wake up in the early 1960s, when his ideas had been accepted. Personally, I wish I could just fast forward to the 2030s. It’s tiresome having to continually point out the obvious; we need highly liquid macro prediction markets. In early 2016, when the Fed got very nervous due to falling equity prices, we had no NGDP futures market showing whether those declining equity prices reflected falling NGDP growth expectations. The Fed was flying blind.

READER COMMENTS

Philo

Apr 16 2016 at 1:57pm

“It’s tiresome having to continually point out the obvious . . . .” But there are so few besides you who are willing to do it, and even they seem to lack your energy. Hang tough!

Dikran Karagueuzian

Apr 16 2016 at 3:28pm

“It’s tiresome having to continually point out the obvious . . . .”

I don’t know how you can do this without going crazy, but please keep up the good work!

Federico

Apr 16 2016 at 6:44pm

Scott, why do you not find the nowcasters useful? They’re a pretty good way of aggregating disparate information, no?

Benjamin Cole

Apr 17 2016 at 11:47am

Sure seems to me that nowcasting could be done. Retailers know when they sell a pack of gum. Hotel chains and airlines know to the room and seat how many are sold. Amazon?

Utilities know power consumption. Trains are well monitored. UPS deliveries. All this in real time now.

Seems like some aggregation and data-work could be done.

Scott Sumner

Apr 17 2016 at 10:53pm

Philo and Dikran, Thanks.

Federico, I suppose they have some value. But a true NGDP market, with prices changing minute by minute, would be far more valuable.

Ben, Good point.

Stats

Apr 18 2016 at 1:43am

[Comment removed for supplying false email address. Email the webmaster@econlib.org to request restoring this comment and your comment privileges. A valid email address is required to post comments on EconLog and EconTalk.–Econlib Ed.]

Louis Woodhill

Apr 18 2016 at 9:38am

An NGDP prediction market would work, but only if the Fed was not targeting it. If the only reason that a player had to do a transaction in an NGDP futures market was to profit from his “bet,” no one would bet against the Fed by buying or selling at a price significantly different from the Fed’s target.

OTOH, the Fed could target (say) the CRB Index without impeding trading, because there are reasons to buy and sell commodities other than to place bets on monetary policy.

Comments are closed.