Marcus Nunes directed me to a post by Jerry O’Driscoll, which asked the following questions:

The specific question I pose for advocates of NGDP targeting is how today will anything the Federal Reserve does to its balance sheet alter the growth rate of NGDP in a predictable fashion? The answer to such a question could be that the central bank should do more. How much more? And what, then, becomes of the rule? It sounds like a recipe for discretion. In any case, central banks have been unable to get either component of NGDP to grow in a normal or predictable manner.

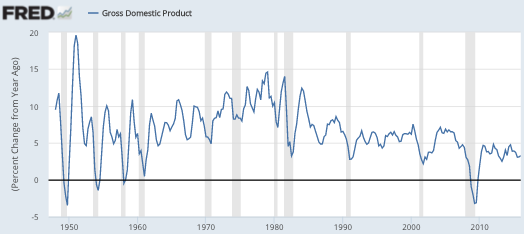

Before answering this question, let’s take a look at NGDP growth in the US:

Notice that NGDP growth became more stable after the mid-1980s. There are many possible explanations, but I believe one factor was the Fed’s adoption of something close to the Taylor Rule. Then NGDP plunged sharply in 2008-09, and the recovery was rather disappointing. So how can we do better?

1. Make policy more effective when the economy is not at the zero bound.

2. Address the zero bound problem. Most economists believe that at least part of the problem since 2008 is that the Fed becomes less effective at the zero bound.

Let’s consider the zero bound problem first. There are two basic approaches to dealing with the zero bound:

1. Dramatically increase the supply of base money.

2. Reduce the demand for base money.

A reduction in base money demand can be done in one of two ways:

1. Raise the trend rate of growth in NGDP/inflation and/or adopt level targeting.

2. Adopt the sort of negative interest rate policy recommended by Miles Kimball.

So there are clearly lots of ways of addressing the zero bound problem, but not surprisingly they are all a bit controversial. Ideally, Congress should instruct the Fed on which approaches are better, but at this point Congress does not understand the problem. Thus Janet Yellen needs to go to Congress and say that the Fed will have to adopt one of those three policies during the next recession, or else monetary policy will fail. I suppose we can consider failure an option, and hence the Fed has 4 options. Yellen should tell Congress that in a perfect world Congress would instruct the Fed as to which option or options it prefers, but if they do not do so then the Fed will be forced to choose on its own. In that case, the Fed should do what it thinks best.

In my view, the best option is something like a 4% NGDP target path, level targeting, maintained by a “whatever it takes” adjustment in the Fed’s balance sheet. But the other options (an even faster NGDP growth rate and/or negative interest rates), are also clearly preferable to failure.

So once we solve the zero bound problem, how do we address the discretion issue that Jerry worries about?

1. I prefer using NGDP futures to guide monetary policy. This removes discretion. There are intermediate (hybrid) policies that could also be considered, as when NGDP futures provide guardrails, and the Fed has discretion within those guardrails. Perhaps discretion within 3% and 5% expected NGDP growth.

2. A switch to level targeting would automatically tend to reduce discretion somewhat, as under level targeting there could no longer be hawks and doves at the Fed. The concept would be meaningless.

3. If the Fed insists on continuing to do what it did in the period 1984-2007, then policy will not be optimal, but I do think that this policy regime was reasonably effective at producing fairly stable NGDP growth. And even under discretion, it’s possible to improve policy through level targeting, the ending of interest rate smoothing, and the adoption of Lars Svensson’s proposal to “targeting the forecast”, which means always maintaining equality between the goal of policy and the Fed’s own forecast of future NGDP. In late 2008, that criterion would have required buying enough assets to insure that expected mid-2010 NGDP exceeded mid-2008 NGDP by the policy target (say 8% or 10%, if the NGDP target growth rate had been 4% or 5% per year.)

READER COMMENTS

James

Jun 12 2016 at 4:31pm

Scott,

Targeting the forecast can only work to the extent that the forecast is accurate, but we know that macro models do not produce accurate NGDP forecasts. You can conjecture that NGDP futures would be an accurate forecast but you don’t know that because no such market exists. I mention this because you failed to address the first question: “How today will anything the Federal Reserve does to its balance sheet alter the growth rate of NGDP in a predictable fashion?”

Do you believe it is possible, even in theory, to create a rule which prevents the use of discretion if the central bank officials want to use discretion? An activist Fed could sneak discretion into the mix by adjusting the target NGDP growth rate.

Scott Sumner

Jun 12 2016 at 5:02pm

James, You said:

“Do you believe it is possible, even in theory, to create a rule which prevents the use of discretion if the central bank officials want to use discretion? An activist Fed could sneak discretion into the mix by adjusting the target NGDP growth rate.”

No. In fact even abolishing the Fed would not prevent the government from doing discretion if it wanted to. Indeed nothing could prevent that, not even a gold standard. I’d rather not worry about problems that have no solution, and try to make current policy less bad, under the assumption that the Fed would like to see more effective policy. I think that’s a reasonable conjecture, indeed why else would the Fed have begun targeting inflation at 2% a few decades ago?

I prefer rules to discretion, but I think it’s wrong to get too obsessed with trying to come up with a rule that makes discretion impossible. It just can’t be done. Instead we should look for policies that would make it easier to stabilize the path of NGDP. The Fed made some changes in the 1980s that helped smooth NGDP growth, and there are some additional changes that would improve it even further.

Now let’s take a look at this question:

“How today will anything the Federal Reserve does to its balance sheet alter the growth rate of NGDP in a predictable fashion?”

I gave three methods of overcoming the zero bound problem, only one of which involved altering the Fed’s balance sheet. I would say the same about affecting NGDP expectations.

As far as market NGDP forecasts, you are right that they are not perfect. But the main problem with monetary policy has not been an inability of the market to forecast NGDP (it clearly saw NGDP expectations plunging in late 2008) the main problem is that the Fed put too little weight on those market forecasts.

In my own view, monetary policy can be reasonably effective at the zero bound. But if you don’t think that’s possible, then you’d favor either negative interest rates or a higher inflation/NGDP target path. It’s hard for me to fully answer your question without knowing which approaches are in bounds and which are out of bounds.

michael pettengill

Jun 12 2016 at 7:52pm

James writes:

Sounds like you read Milton Friedman’s paper on the near impossibility of prediction based on uncertain contemporary data, sometime before 1973. He proved that unless the data was at least 75% correct, any actions taken based on cycle theory will make the cycles more extreme. I think the paper was published in the 50s, but 60s at latest.

He argued against all fiscal and monetary policy to prevent recessions or bubbles.

Bill Woolsey

Jun 12 2016 at 8:57pm

O’Driscoll has in mind an instrument rule–adjust the federal funds rate by so many basis points according to the percent deviation of nominal GDP from the target growth path, or adjust the growth rate (or path?) of base money so many percent according to the percent deviation of nominal GDP from its target growth path.

Then, if nominal GDP isn’t on target, it must “do more.” That would mean changing base money or the federal funds rate by more than what the rule states. The Fed then has discretion.

O’Driscoll sees that as unacceptable and favors commodity money.

I believe that any rule like O’Driscoll is describing should be nothing more than a rule of thumb that should be adjusted, That is, I think discretion should be allowed regarding interest rates or the quantity of base money.

What should be constraining to the Fed is the nominal anchor–like the growth path for nominal GDP. They shouldn’t have discretion to adjust that on the fly.

During the Great Inflation, the Fed had no nominal anchor. It claimed inflation was out of its control. And they just tried to promote full employment. The had discretion regarding the nominal anchor, including throwing up their hands and not even trying.

The gold standard requires that money be redeemable in gold or, at the very least, the price of gold be pegged.

Does that mean there should be a formula relating gold reserves to changes in interest rates or the quantity of paper money? Or some formula relating the market price of gold to interest rates or some measure of the quantity of base money?

To me, the central bank should adjust the interest rates in charges or pays or the quantity of reserves or paper currency it issues as it thinks best, subject to constraint that it maintain redeemability or keep the price pegged.

If one favors free banking so that central bank discretion is not an issue, the notion that any or all banks should set the interest rates they charge or pay or their issue of currency or deposits according to a formula would be absurd (or I would think so.) Maximize profit subject to the constraint that redeemability is maintained.

The same is sure for nominal GDP level targeting. Adjust interest rats or the quantity of currency or reserves according to best judgement subject to the constraint than nominal GPD remain on the target growth path.

michael pettengill

Jun 13 2016 at 4:45am

NGDP or GDP are driven primarily by labor costs. To have rising (N)GDP, labor costs must rise.

Whether labor costs go to funding consumption or capital has long run effects, but higher labor costs will always mean higher GDP.

I’ve argued for some years that the Fed should implement “quantitative easing” by buying zero interest 30 year tax revenue bonds building new capital assets, ie 100% labor cost. (Capital costs are, in a competitive market, almost 100% labor cost. In a global recession, buying a CAT road grader will be labor cost.)

The reasons for contractions is that people/institutions with money refusing to pay labor to work, often to increase monopoly power to allow rent seeking to inflate asset prices with zero labor costs.

Speculators buying real estate do so to create scarcity to drive up the price in the expectation they will be able to stop their pump and dump asset churning before the buyers go on strike. After 1980 to 1986, 2000 to 2006 was clearly a rerun – I just had no idea it was possible to bet against the asset inflation I saw and win big.

ThaomasH

Jun 13 2016 at 1:14pm

Boring as it may be, this is the kind of post you need to write pretty frequently to get people to understand your position. You might strengthen it by more specific comments of exactly what the Fed should have done when in the past.

Scott Sumner

Jun 13 2016 at 5:11pm

Bill, You said:

“The same is sure for nominal GDP level targeting. Adjust interest rats or the quantity of currency or reserves according to best judgement subject to the constraint than nominal GPD remain on the target growth path.”

Nominal GDP, or expected nominal GDP?

Michael, You said:

“Whether labor costs go to funding consumption or capital has long run effects, but higher labor costs will always mean higher GDP.”

It depends what you mean by labor costs. Rising total labor costs are usually associated with rising NGDP. That’s less true for rising hourly labor costs.

Thanks Thaomas.

James

Jun 14 2016 at 8:31am

Scott,

I wasn’t asking about any zero lower bound problem. On that, I don’t think I would have any room to disagree with you. I believe central bankers can create inflation whenever they want to.

I was asking about predictability, hence the bold font. If the central bankers want to cause the next quarter’s NGDP to be some value X, how do they get it there in a predictable way versus overshooting or undershooting?

I’ll give a concrete example. Say the target for next quarter’s NGDP is 100 and the central bank has a model (or a futures market) for forecasting NGDP. The model (or futures market) has an standard error of Z. At some point, I hope you will admit that the forecasts errors are so large that NGDP targeting is not an implementable option. Unless the forecasts are “good enough,” then NGDP targeting can’t possibly work. So far, you have never produced evidence that NGDP forecasts wil be accurate enough or even described what you see as a sufficient degree of accuracy.

Scott Sumner

Jun 14 2016 at 1:35pm

James, I agree that market-based NGDP forecasts will not be perfect, but I do think they would be better than the alternative.

I also think that an NGDPLT regime would make NGDP forecasts more accurate, as it would reduce the volatility of actual NGDP.

You said:

“At some point, I hope you will admit that the forecasts errors are so large that NGDP targeting is not an implementable option.”

It depends on the alternative. Suppose the alternative is relying on Fed forecasts of NGDP, and suppose that those are even worse than market forecasts (a not unreasonable assumption.) In that case, a market-based NGDPLT policy would still be the lesser of evils. You can’t beat something with nothing; you need an alternative to compare to a market-based approach. What is your alternative?

James

Jun 14 2016 at 5:48pm

Scott,

What? NGDP targeting requires forecasts. This is true no matter what the alternatives may be. If the forecasts are poor, NGDP targeting is not possible. No matter what the alternatives may be.

Tangentially, I do not believe the specific choice of what variable to target will have a large impact on anything except in rare and unpredictable cases. Other variables outside the control of the central bank are so much more important.

Maybe one day some country will try NGDP targeting and we will see how much difference it makes. I predict not much.

Elwailly

Jun 15 2016 at 10:30am

James,

“If the forecasts are poor, NGDP targeting is not possible.”

I think this should say “NGDP forecast targeting”.

This should be possible even if the forecasts are poor. With level targeting, NGDP growth should be predictable in the medium term even with forecast errors.

Most important is the impact on consumer and investor behavior. They can make medium term consumption and investment decisions knowing that NGDP forecast errors will be corrected as a matter of course.

Comments are closed.