Suppose you favor a 4% NGDP target. And suppose NGDP growth is running at 3%. What advice should you give to the Fed? I will argue that you should not advise the Fed to push NGDP growth up to 4%. Before explaining why, let’s revisit a prediction I made 28 months ago, at a time when NGDP growth was averaging roughly to 4%:

The Fed has a big NGDP problem. It’s becoming increasingly clear that when the labor market recovers, RGDP growth will be very slow, maybe 1.2%. Add in about 1.8% on the GDP deflator, and 3% NGDP growth looks like the new normal, assuming the Fed intends to stick with 2% PCE inflation targeting.

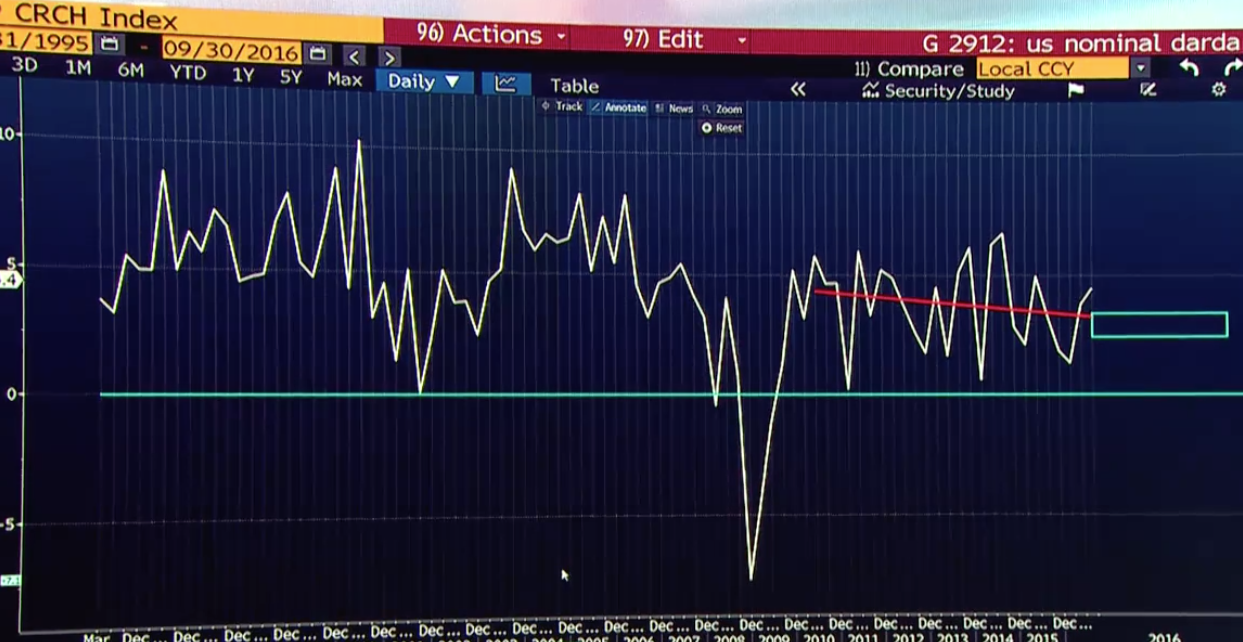

I believe that this will eventually become the conventional wisdom. Today on BloombergTV, Michael Darda made a similar claim. He suggested that 3% NGDP growth is the new normal for the Fed, as productivity growth has fallen to 0.6% and working age population growth has also slowed to about 0.6%.

Many people are confused on this point—they speak of “slack” in the economy, and an ability to grow faster to soak up that slack. Even if they are correct (which is unclear), that has no bearing on the trend rate of growth. The trend rate averages growth during both recessions and expansions. Yes, NGDP growth has averaged closer to 4% since 2009, but that’s a period when the unemployment rate fell from 10% to 5%. It’s not going to fall to 0% over the next 7 years. In the long run, unemployment (and labor force participation) is stable, then neither rise nor fall. That’s why America’s trend rate of growth is actually well below the actual growth over the past 7 years.

So that explains 1.2% RGDP growth, but why do I assume a 1.8% inflation rate? My view is that at current levels of interest rates, we will hit the zero bound in every future recession. At that point, inflation will run below 2%—not because the Fed wants it to, but rather because their policy tools (fed funds targeting) are defective. With NGDP futures targeting, inflation would run above 2% during recessions.

Under the current policy regime the Fed will boost inflation up to 2% during expansions. It’s not that the Fed has a 2% ceiling; it’s symmetrical as long as the economy grows as they expect. Rather that their technique leads to on target inflation during booms and below target inflation during recessions.

Oddly, the Fed always assumes that there will never again be another recession. Look at their longer term forecasts—they never show an expected recession. So they aim for 2% inflation going forward, during an anticipated expansion, even though they know that if we do fall into another recession then inflation will undershoot 2%.

So the Fed’s current policy regime will deliver 3% NGDP growth in the long run. In that case, how do we best stabilize the economy? The answer is simple; aim for 3% NGDP growth each and every year. If you aim for 4% growth one year, that will be offset by 2% growth in another year. That sort of NGDP roller coaster makes recessions more likely. I think Janet Yellen understands this, which is why her policy seems more hawkish than many of her supporters anticipated.

So far it sounds like I am trying to let the Fed off the hook. Not so. While their tactics are defensible given their current long run strategy, the strategy itself is horrible: Targeting inflation instead of NGDP. Doing growth rate targeting instead of level targeting. Using interest rates as a monetary instrument. Doing policy with no NGDP futures market guardrails to warn of policy being off course. Procyclical inflation. The list could go on and on. It’s a horrible strategy. So I’m just as much a Fed critic as I’ve always been—it’s just that I see strategy as the big issue.

But given the Fed’s strategy, the tactics are actually roughly appropriate, at least at the moment. In contrast, even the tactics were far off course in 2008-12.

To summarize, your tactical advice should not reflect your preferred strategy, it should reflect the Fed’s preferred strategy.

PS. My prediction implies that 2.4% is the new normal for wage growth. That’s inflation plus productivity.

PPS. This is also why many of my commenters are wrong about monetary offset. They speak as if the Fed has a choice to offset fiscal stimulus, or not. But given the Fed’s (de facto) current policy regime of 3% long run NGDP growth, they really don’t have a choice. Inflation targeting forces them to do monetary offset.

PPPS. The next recession might be triggered by government attempts to raise labor costs, not a sharp NGDP slowdown. If so, it will be mild.

PPPPS. I forget to mention that Iceland’s Pirate Party, discussed in a previous post, did not do as well as expected in Sunday’s election, getting 10 seats out of 63. No group has a majority at the moment, so it still could end up in the government.

READER COMMENTS

bill

Nov 1 2016 at 9:10pm

Should the Fed ever predict a recession? If they see one coming wouldn’t they also assume that they’d react appropriately? I guess inflation well above target could tie their hands but they wouldn’t be expecting that either under current conditions.

Scott Sumner

Nov 2 2016 at 9:03am

Bill, Yup. I wrote a paper back in 2008 with that theme, in a sense it’s why I got into blogging.

Comments are closed.